|

|

|

|

|||||

|

|

|

Johnson & Johnson JNJ has delivered a strong run over the past three months, with shares up 17.7% and nearly $63 billion in market capitalization added. The stock’s technicals support this momentum. It has been trading consistently above its 50-day and 200-day moving averages since mid-June. This, along with the mid-July “golden cross” — when the 50-day average moved above the 200-day — reinforces the case for continued upside.

Historically, such a setup has signaled the potential for extended bullish trends, reflecting stronger near-term price action relative to the longer-term trend. The 50-day SMA has been above the 200-day SMA since it achieved the golden cross, a positive sign for the stock’s future gains.

Let’s understand J&J’s strengths and weaknesses to better analyze how to play the stock after the recent price gain.

J&J’s Innovative Medicine unit is showing a growth trend. The segment’s sales rose 2.4% in the first half of 2025 on an organic basis despite the loss of exclusivity for a blockbuster drug like Stelara, and the negative impact of the Part D redesign. J&J expects continued growth in the second half of 2025 to be driven by its key products such as Darzalex, Tremfya, Spravato and Erleada, as well as new drugs like Carvykti, Tecvayli and Talvey and new indications for Tremfya and Rybrevant.

J&J expects the Innovative Medicine business to grow 5% to 7% from 2025 to 2030. J&J expects its oncology sales to be more than $50 billion by 2030.

J&J believes 10 of its new products/pipeline candidates in the Innovative Medicine segment have the potential to deliver peak sales of $5 billion, including Talvey, Tecvayli, Imaavy, Caplyta, Inlexzo and icotrokinra.

Three of J&J’s new cancer drugs, Carvykti, Talvey and Tecvayli, have begun to contribute to top-line growth. Combined, they generated $1.3 billion in sales in the first half of 2025.

Imaavy (nipocalimab) was approved in April for treating generalized myasthenia gravis. Inlexzo (TAR-200) was approved by the FDA for treating non-muscle invasive bladder cancer in August and is expected to be launched later this year. Caplyta was added with the April acquisition of Intra-Cellular Therapies. A new drug application seeking approval of icotrokinra, an oral targeted peptide inhibitor of the IL-23 receptor, for moderate-to-severe plaque psoriasis, was filed in July.

J&J’s MedTech segment sales rose 6.1% on an operational basis in the second quarter, improving from the first-quarter levels, driven by the newly acquired cardiovascular businesses, Abiomed and Shockwave, as well as in Surgical Vision and wound closure in Surgery. Moreover, improvements in J&J’s electrophysiology business also drove sequential growth. In the MedTech segment, increased adoption of newly launched products in Cardiovascular, Surgery and Vision is likely to drive growth in the second half. Sales are expected to be higher in the second half than the first half as the business moves past tougher first-half comps and new products gain momentum throughout 2025.

However, the company continues to face headwinds in China. Sales in China are being hurt by the impact of the volume-based procurement (VBP) program, which is a government-driven cost containment effort in China. J&J expects continued impacts from VBP issues in China in the second half as the program continues to expand across provinces and products.

J&J lost U.S. patent exclusivity of Stelara in 2025. Stelara was a key top-line driver for J&J, accounting for around 18% of J&J’s Innovative Medicine unit’s sales in 2024, before it lost patent exclusivity in 2025.

Several biosimilar versions of Stelara have been launched in the United States in 2025. According to patent settlements and license agreements, Amgen AMGN,Teva Pharmaceutical Industries TEVA, Samsung Bioepis/Sandoz and some other companies have already launched Stelara biosimilars this year. The launch of generics by Amgen, Teva and other companies is significantly eroding Stelara’s sales and hurting J&J’s sales and profits in 2025. Stelara sales declined 38.6% in the first half of 2025. Stelara biosimilar competition is expected to accelerate throughout 2025 as the number of biosimilar entrants increases.

In addition, sales in 2025 are being hurt by the impact of the Medicare Part D redesign under the Inflation Reduction Act (IRA). Among other measures, the IRA requires the U.S. Department of Health and Human Services (HHS) to effectively set prices for certain single-source drugs and biologics reimbursed under Medicare Part B and Part D.

In August 2023, the HHS selected J&J’s drugs, Xarelto, Stelara and Imbruvica as one of the first 10 medicines subject to government-set prices. J&J expects a negative impact of approximately $2 billion in sales due to the Medicare Part D redesign in 2025. The Part D redesign is mainly hurting sales of drugs like Stelara, Tremfya, Erleada and pulmonary hypertension drugs.

J&J faces more than 70,000 lawsuits for its talc-based products, primarily baby powders. The lawsuits allege that its talc products contain asbestos, which caused many women to develop ovarian cancer. J&J insists that its talc-based products are safe and do not cause cancer. The company permanently discontinued the sales of its talc-based Johnson’s Baby Powder.

In April, a bankruptcy court in Texas rejected J&J’s proposed bankruptcy plan to settle its talc lawsuits after a two-week trial in Houston. J&J has gone back to the traditional tort system to fight the lawsuits individually with its bankruptcy strategy to settle the lawsuits, failing for the third time.

The uncertainty around tariffs and trade production measures has muted economic growth. President Trump has threatened to impose heavy tariffs, as high as 250%, on pharmaceutical imports. Trump’s repeated threats to impose tariffs on pharmaceutical imports are aimed at pushing American pharma companies to shift pharmaceutical production back to the United States, primarily from European and Asian countries. Trump has said that drugmakers have about one to one and a half years to bring production back to the United States before the new tariffs are imposed.

J&J has already committed to boosting manufacturing in the United States and has a plan to invest $55 billion over the next four years to ensure that all medicines consumed in the United States are manufactured domestically.

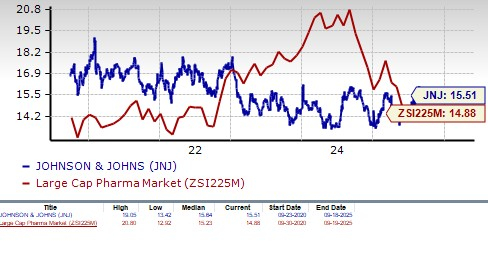

J&J’s shares have outperformed the industry year to date. The stock has risen 23.1% in the year-to-date period compared with a 0.9% increase for the industry. The stock has also outperformed the sector and the S&P 500 Index, as seen in the chart below.

From a valuation standpoint, J&J is expensive. In terms of the price/earnings ratio, the company’s shares currently trade at 15.51 forward earnings, higher than 14.88 for the industry. The stock is also trading above its five-year mean of 15.64.

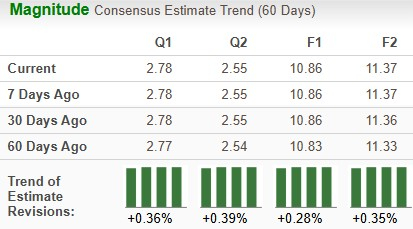

The Zacks Consensus Estimate for 2025 earnings has risen from $10.83 per share to $10.86 over the past 60 days, while that for 2026 has risen from $11.33 to $11.37 over the same timeframe.

J&J considers 2025 to be a “catalyst year,” positioning the company for growth in the second half of the decade. J&J expects operational sales growth in both the Innovative Medicine and MedTech segments to be higher in the second half than in the first. J&J expects growth to accelerate from 2026 onward.

J&J is also rapidly advancing its pipeline, attaining significant clinical and regulatory milestones that will help drive accelerating growth through the back half of the decade. J&J has also been on an acquisition spree, with the latest acquisition of Intra-Cellular Therapies strengthening its presence in the neurological and psychiatric drug market.

The Stelara patent cliff and the impact of Part D redesign will be significant headwinds in 2025. The uncertainty around the unresolved legal issues and pharma tariffs lingers. However, the company looks quite confident that it will be able to navigate these challenges.

The stock’s price appreciation this year and rising estimates should encourage investors to bet on this Zacks Rank #2 (Buy) stock despite the slightly high valuation. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 4 hours | |

| 17 hours | |

| Feb-27 | |

| Feb-27 |

These Stocks Lead Dow Jones In February. Hint: It's Not AI Companies.

AMGN JNJ

Investor's Business Daily

|

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-25 | |

| Feb-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite