|

|

|

|

|||||

|

|

|

C3.ai, Inc. AI began fiscal 2026 on a weaker footing as profitability concerns resurfaced. In the fiscal first quarter, non-GAAP gross margin slipped to 52%, representing a 1,800-basis-point decline from the 70% reported in the prior-year period. The downside was attributed to a higher proportion of initial production deployments (IPDs) related costs, reduced revenues from demonstration licenses and lower economies of scale. For a company aiming to achieve non-GAAP profitability and free cash flow, the margin contraction underscores the pressure that scaling new deployments places on operating leverage.

The pivot toward IPDs reflects both expansion potential and margin risk. These contracts extend C3.ai’s footprint across industrial and government clients but carry elevated upfront service costs. Management acknowledged that gross margins are likely to remain moderate in the near term as the company builds out support capacity.

Despite these headwinds, subscription revenues remained a stabilizing factor, contributing $60.3 million, or 86% of total fiscal first-quarter revenues. Liquidity also remains a differentiator, with $711.9 million in cash and equivalents providing flexibility to absorb operating losses. However, the free cash flow of negative $34.3 million reflects the intensity of ongoing investment. Until IPDs begin to scale into profitable recurring streams, progress toward profitability will likely be slower than previously anticipated.

Looking ahead, margin stabilization remains critical for investor confidence. With 90% of new business sourced through partners such as Microsoft Azure, AWS and Google Cloud, C3.ai has a channel to scale quickly. Yet, without evidence of an improving gross margin trajectory, the timeline to sustainable profitability could extend further, leaving the company at a relative disadvantage compared to peers that maintain stronger operating efficiency.

Palantir Technologies Inc. PLTR is setting itself apart with industry-leading gross margin fundamentals. In the second quarter of 2025, the company reported an adjusted gross margin of 82%, underscoring the scalability of its software-first model and strong unit economics across both commercial and government contracts. This margin profile enabled Palantir to expand its adjusted operating margin to 46%, while still delivering outsized top-line growth of 48% year over year. The high-margin nature of Palantir’s platform not only supports robust free cash flow ($569 million) but also provides ample cushion to reinvest in AI innovation without sacrificing profitability.

Snowflake Inc. SNOW also demonstrated healthy margin performance, albeit at slightly lower levels relative to Palantir. In the second quarter of fiscal 2026, Snowflake reported a non-GAAP product gross margin of 76.4%, consistent with its long-term target of approximately 75%. The figure reflects ongoing efficiency gains within its AI Data Cloud and stable unit economics under its consumption-based model. While operating margins remain modest at 11%, Snowflake’s gross margin fundamentals provide the flexibility to balance investment in growth initiatives with the pursuit of durable free cash flow, guided at 25% for fiscal 2026.

Compared to these peers, C3.ai’s reliance on upfront-cost-heavy IPDs highlights its different stage of maturity. While Palantir and Snowflake are demonstrating the ability to scale AI platforms profitably with strong margins, C3.ai remains in investment mode, with negative free cash flow and moderated gross margins. Until IPDs convert into high-margin recurring streams, C3.ai risks ceding ground to competitors with proven operating models.

Shares of C3.ai have declined 23.6% in the past three months compared with the industry’s fall of 6.1%.

From a valuation standpoint, AI trades at a forward price-to-sales ratio of 7.86X, significantly below the industry’s average of 17.20X.

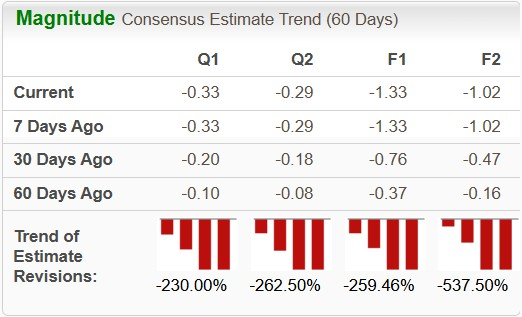

The Zacks Consensus Estimate for AI’s fiscal 2026 earnings per share (EPS) implies a year-over-year downtick of 224.4%, while fiscal 2027 EPS indicates a rise of 23.7% year over year. The EPS estimates for fiscal 2026 and 2027 have declined in the past 30 days.

AI stock currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 18 min | |

| 31 min |

Stock Market Today: Dow Rises Ahead Of Fed Minutes; Nvidia Jumps On Meta Deal (Live Coverage)

PLTR

Investor's Business Daily

|

| 44 min | |

| 59 min | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 5 hours | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite