|

|

|

|

|||||

|

|

|

Comfort Systems USA, Inc. (FIX) delivered a standout second-quarter 2025 performance, underscoring its strength in mechanical services and positioning as a long-term value creator. The company reported record revenues of $2.17 billion, up 20% year over year, while earnings per share surged 75% to $6.53, reflecting sharp margin expansion and strong project execution.

Mechanical services, the backbone of Comfort Systems’ business, recorded significant profitability gains this quarter. Gross margins in the segment climbed to 22.9%, up from 19.2% a year earlier, highlighting both disciplined project selection and efficiency improvements. Importantly, service revenues, an often-overlooked but stable component, grew 10% and now contributes 15% of total sales, providing recurring cash flows that buffer against cyclicality.

The company’s record $8.1 billion backlog, up 41% year over year, provides visibility well into 2026 and beyond. Much of this demand stems from industrial and technology sectors, particularly data center construction, where Comfort Systems’ expertise in complex mechanical solutions is driving strong bookings. Management also continues to invest in modular capabilities, adding capacity to capture growth through faster and more efficient construction methods.

Alongside operational execution, the company remains disciplined financially. It generated more than $220 million in free cash flow during second-quarter 2025 and repurchased shares while maintaining a net cash position of $250 million.

Overall, Comfort Systems’ rising margins, diversified end-market exposure and strong balance sheet indicate that its mechanical services business is not only thriving in the current cycle but also building durable long-term value for investors.

In assessing Comfort Systems’ long-term value creation in mechanical services, it is helpful to compare with peers such as EMCOR Group, Inc. (EME) and Quanta Services, Inc. (PWR).

EMCOR, like Comfort Systems, has seen robust growth driven by mechanical and electrical construction services. Its diversified portfolio across healthcare, industrial and commercial markets provides resilience, though EMCOR’s growth is somewhat less concentrated in high-demand technology projects such as data centers. This makes Comfort Systems more leveraged to fast-growing end markets, though EMCOR’s scale remains a competitive strength.

Quanta Services, on the other hand, has built a reputation in large-scale infrastructure and utility projects, particularly in renewable energy and power grid modernization. Though it is not a direct competitor in mechanical services, Quanta’s exposure to long-cycle infrastructure spending provides a stability advantage.

Compared with both, Comfort Systems’ focus on mechanical expertise and modular innovation positions it uniquely to capture value in complex, technology-driven construction.

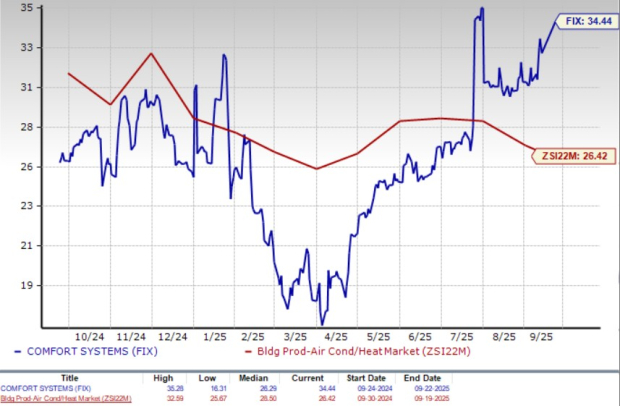

Shares of Comfort Systems have gained 60.1% in the past three months against the Zacks Building Products - Air Conditioner and Heating industry’s decline of 3.4%.

From a valuation standpoint, FIX trades at a forward 12-month price-to-earnings ratio of 34.44X, up from the industry’s 26.42X.

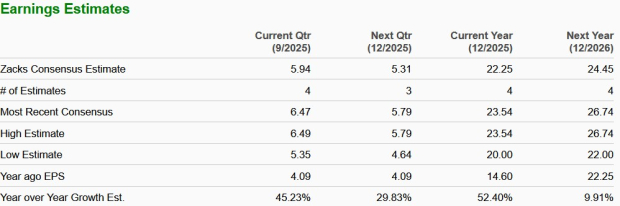

Comfort Systems’ earnings estimates for 2025 and 2026 have trended upward in the past 30 days by 2% to $22.25 per share and 2.4% to $24.45, respectively. The estimated figures for 2025 and 2026 indicate 52.4% and 9.9% year-over-year growth, respectively.

Comfort Systems currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-14 |

Boeing Holds In Buy Zone, Leads 5 Stocks To Watch In Short Trading Week

PWR

Investor's Business Daily

|

| Feb-13 |

IPO Stock Of The Week: Health Care Leader BrightSpring Eyes New Buy Point

PWR

Investor's Business Daily

|

| Feb-13 |

Walmart Stock, Parade Of Gold Leaders Headline Another Busy Earnings Calendar

PWR

Investor's Business Daily

|

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 |

Comfort Systems Is Trading At A Record High As It Constructs An AI Future

FIX

Investor's Business Daily

|

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite