|

|

|

|

|||||

|

|

|

The end of the earnings season is always a good time to take a step back and see who shined (and who not so much). Let’s take a look at how custody bank stocks fared in Q1, starting with Hamilton Lane (NASDAQ:HLNE).

Custody banks safeguard financial assets and provide services like settlement, accounting, and regulatory compliance for institutional investors. Growth opportunities stem from increasing global assets under custody, demand for data analytics, and blockchain technology adoption for settlement efficiency. Challenges include fee pressure from large clients, substantial technology investment requirements, and competition from both traditional players and fintech firms entering the space.

The 12 custody bank stocks we track reported a mixed Q1. As a group, revenues beat analysts’ consensus estimates by 1.3%.

In light of this news, share prices of the companies have held steady as they are up 2.4% on average since the latest earnings results.

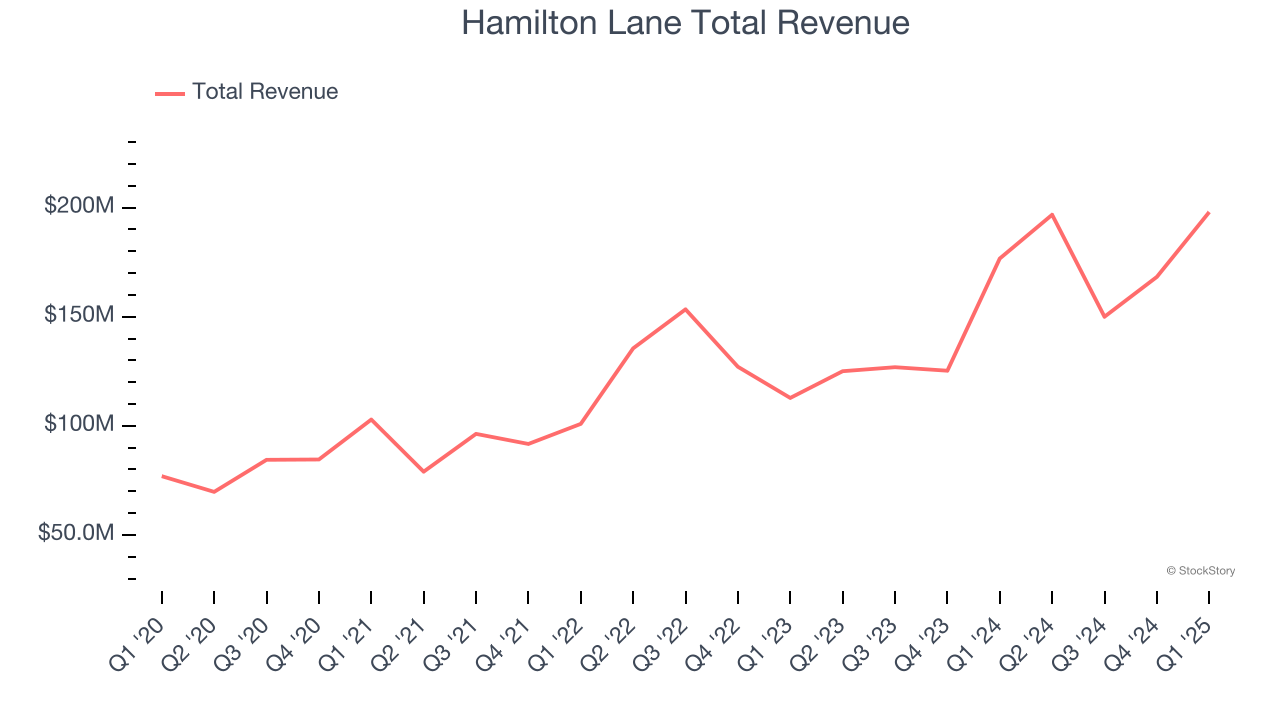

With over $100 billion in assets under management and supervision, Hamilton Lane (NASDAQ:HLNE) is an investment management firm that specializes in private markets, offering advisory services and fund solutions to institutional and private wealth investors.

Hamilton Lane reported revenues of $198 million, up 12.1% year on year. This print exceeded analysts’ expectations by 20.9%. Overall, it was a very strong quarter for the company with a solid beat of analysts’ EBITDA estimates and a beat of analysts’ EPS estimates.

Hamilton Lane achieved the biggest analyst estimates beat of the whole group. Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 18.7% since reporting and currently trades at $142.39.

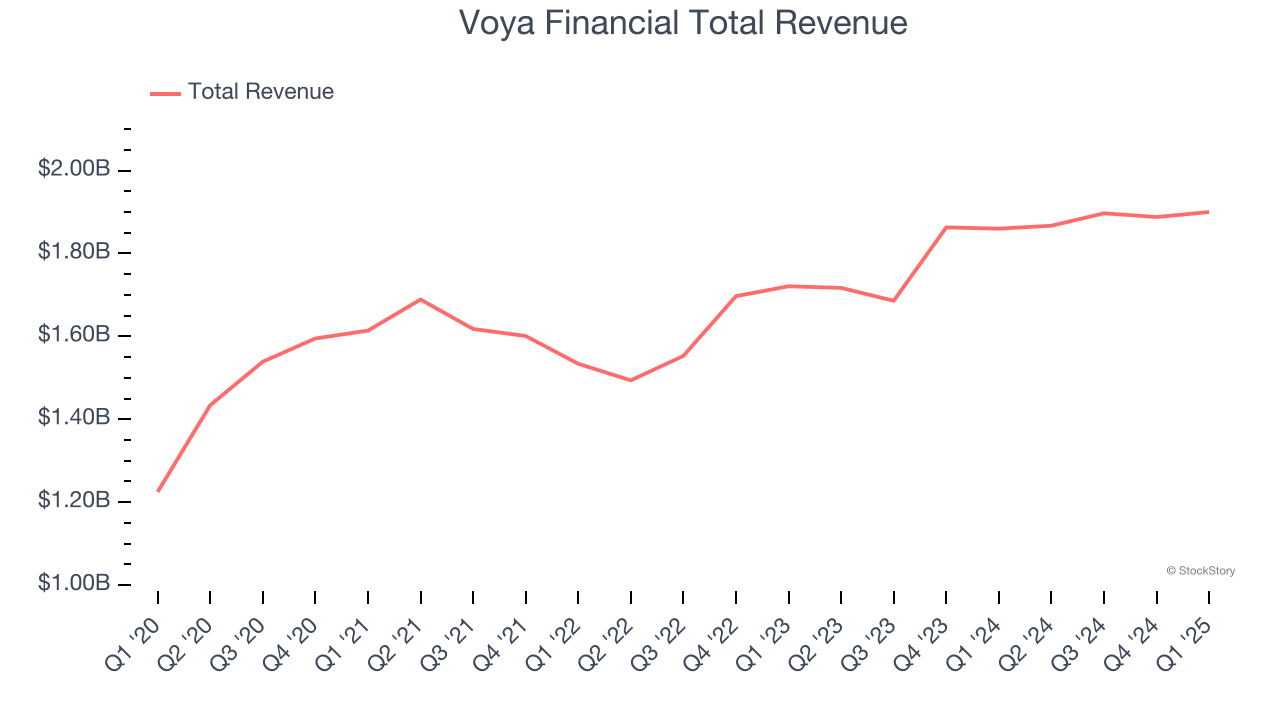

Originally spun off from Dutch financial giant ING in 2013 and rebranded with a name suggesting "voyage," Voya Financial (NYSE:VOYA) provides workplace benefits and savings solutions to U.S. employers, helping their employees achieve better financial outcomes through retirement plans and insurance products.

Voya Financial reported revenues of $1.9 billion, up 2.2% year on year, outperforming analysts’ expectations by 13.5%. The business had a stunning quarter with a solid beat of analysts’ AUM estimates and a beat of analysts’ EPS estimates.

The market seems happy with the results as the stock is up 11.5% since reporting. It currently trades at $75.63.

Is now the time to buy Voya Financial? Access our full analysis of the earnings results here, it’s free.

Operating under the widely recognized Franklin Templeton brand since 1947, Franklin Resources (NYSE:BEN) is a global investment management organization that offers financial services and solutions to individuals, institutions, and wealth advisors worldwide.

Franklin Resources reported revenues of $1.59 billion, down 3.7% year on year, falling short of analysts’ expectations by 18.8%. It was a softer quarter as it posted a significant miss of analysts’ EPS estimates.

Franklin Resources delivered the weakest performance against analyst estimates in the group. The stock is flat since the results and currently trades at $23.75.

Read our full analysis of Franklin Resources’s results here.

Operating as both an advisor and asset manager with over $100 billion in assets under management, StepStone Group (NASDAQ:STEP) is an investment firm that provides clients with access to private market investments across private equity, real estate, private debt, and infrastructure.

StepStone Group reported revenues of $237.5 million, up 27.4% year on year. This print came in 1.1% below analysts' expectations. It was a slower quarter as it also logged a significant miss of analysts’ AUM estimates and a significant miss of analysts’ EPS estimates.

StepStone Group achieved the fastest revenue growth among its peers. The stock is up 13.3% since reporting and currently trades at $65.23.

Read our full, actionable report on StepStone Group here, it’s free.

With roots dating back to 1955 and a pioneering role in money market funds, Federated Hermes (NYSE:FHI) is an investment management firm that offers a wide range of funds and strategies for institutional and individual investors.

Federated Hermes reported revenues of $424.8 million, up 5.5% year on year. This result met analysts’ expectations. Overall, it was a strong quarter as it also produced a solid beat of analysts’ EBITDA estimates and a beat of analysts’ EPS estimates.

The stock is up 3.4% since reporting and currently trades at $51.47.

Read our full, actionable report on Federated Hermes here, it’s free.

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| May-29 | |

| May-29 | |

| May-28 | |

| May-21 | |

| May-21 | |

| May-21 | |

| May-19 | |

| Apr-29 | |

| Apr-23 | |

| Apr-22 | |

| Apr-21 | |

| Apr-20 | |

| Apr-20 | |

| Apr-16 | |

| Apr-14 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite