|

|

|

|

|||||

|

|

|

Ecolab Inc. ECL has been gaining from its solid product portfolio. The optimism, led by a solid second-quarter 2025 performance and continued focus on research and development, is expected to contribute further. However, concerns regarding macroeconomic factors persist.

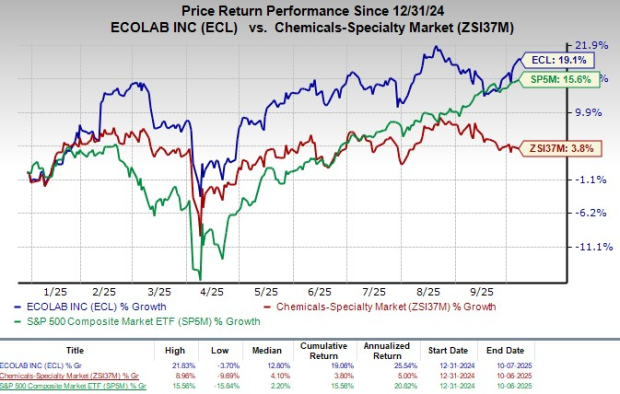

This Zacks Rank #3 (Hold) stock has gained 19.1% in the year-to-date period compared with the industry’s 3.8% growth. The S&P 500 Composite has increased 15.6% during the same time frame.

The renowned water, hygiene and infection prevention solutions and services provider has a market capitalization of $79.34 billion. It projects 12.9% growth for the next five years and expects to maintain a strong performance in the future. Ecolab’s earnings surpassed the Zacks Consensus Estimate in each of the trailing four quarters, delivering an average surprise of 0.29%.

Strong Product Portfolio With a Focus on R&D: Ecolab’s diversified portfolio across water treatment, hygiene, life sciences, digital technologies, and pest control positions it strongly for sustained growth, supported by consistent R&D investments. The global water treatment market, valued at $38.56 billion in 2023, is projected to register an 8.1% CAGR through 2030, providing ample expansion opportunities. In the second quarter, the company reported progress in reshaping its portfolio by exiting non-core, low-margin segments in hospital and retail to concentrate on higher-value areas. Pest Elimination continues to outperform through its digital intelligence model, while Life Sciences sustains robust momentum across biopharma, pharma and personal care, maintaining operating margins near 30%.

Ecolab is also advancing its innovation-led strategy through cutting-edge solutions like the 3D TRASAR AI Dishmachine Program, which applies IoT and machine learning to cut water usage and the 3D Cloud platform, which uses real-time analytics to optimize water treatment. These initiatives, alongside its disciplined portfolio management, highlight Ecolab’s focus on strengthening its competitive edge and driving growth in high-margin, high-tech markets.

Ecolab’s Global High-Tech Business & Digital Platform: Ecolab is accelerating its transformation through two key high-growth, high-margin drivers — its Global High-Tech business and the Ecolab Digital Platform. Per the second-quarter earnings call, the Global High Tech segment delivered sales growth of more than 30%, driven by accelerating demand for data center cooling and water circularity solutions in the fast-expanding microelectronics industry. Management noted that operating margins in this segment now exceed 20%, underscoring both the scalability and profitability of the model, and described it as the beginning of an “incredible growth story” with significant runway as global demand for high-performance and sustainable solutions rises.

Complementing this, Ecolab Digital continued its rapid expansion, with nearly 30% sales growth in the second quarter and an annualized revenue run rate of about $380 million. Growth was fueled by a mix of subscription-based services and digital hardware, demonstrating the company’s ability to monetize its technology platform at scale. These businesses not only enhance Ecolab’s recurring revenue base but also strengthen its positioning in critical industries where efficiency, water management, and sustainability are top priorities, reinforcing the long-term durability of its growth strategy.

Strong Q2 Results: Ecolab ended the second quarter of 2025 with revenue surpassing expectations, posting strong year-over-year growth in both sales and earnings. Most business segments performed well, and margin expansion further strengthened the company’s outlook.

Management noted that the Institutional & Specialty and Global Water divisions delivered notable gains, outperforming market trends driven by the One Ecolab strategy, innovation-led offerings and effective value-based pricing. Meanwhile, key growth engines, such as Life Sciences, Pest Elimination, Global High-Tech and Ecolab Digital, achieved double-digit sales increases, reflecting solid momentum and a positive setup for the stock.

Macroeconomic Factors: Ecolab operates in 170 countries, which is why its operations are subjected to unfavorable social, political and economic challenges that may be ongoing in various countries. Per the second-quarter earnings call, management acknowledged several macroeconomic challenges that are creating near-term headwinds.

Tariffs and tariff-related inflation remain a pressure point, with commodity costs running in the low to mid-single-digit range and expected to persist through the back half of the year. The company also pointed to softer demand in paper and basic industries, which weighed on its performance compared with more resilient sectors. In addition, foreign exchange movements are expected to have an unfavorable impact on expenses relative to last year.

Ecolab is witnessing a stable estimate revision trend for 2025. In the past 30 days, the Zacks Consensus Estimate for its earnings has remained stable at $7.53 per share.

The Zacks Consensus Estimate for the company’s third-quarter 2025 revenues is pegged at $4.12 billion, indicating a 3.1% improvement from the year-ago quarter’s reported number.

Some better-ranked stocks in the broader medical space are Masimo MASI, Merit Medical System MMSI and West Pharmaceutical Services WST, each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Masimo shares have lost 10.4% so far this year compared with the industry’s 7.4% decline. Estimates for the company’s 2025 earnings per share have increased 1.3% to $5.30 in the past 30 days.

MASI’s earnings beat estimates in each of the trailing four quarters, the average surprise being 13.8%. In the last reported quarter, it posted an earnings surprise of 8.1%.

Estimates for Merit Medical’s 2025 earnings per share have increased 0.8% to $3.63 in the past 60 days. Shares of the company have lost 13.8% so far this year against the industry’s 1.1% growth.

MMSI’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 12.92%. In the last reported quarter, it delivered an earnings surprise of 17.44%.

Estimates for West Pharmaceutical’s 2025 earnings per share have increased 1.2% to $6.74 in the past 60 days. Shares of the company have lost 18.2% so far this year against the industry’s 1% growth.

WST’s earnings beat estimates in each of the trailing four quarters, the average surprise being 16.81%. In the last reported quarter, it delivered an earnings surprise of 21.85%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Apr-24 | |

| Apr-23 | |

| Apr-23 | |

| Apr-23 | |

| Apr-23 | |

| Apr-23 | |

| Apr-23 | |

| Apr-22 | |

| Apr-10 | |

| Apr-09 | |

| Apr-02 | |

| Apr-02 | |

| Apr-01 | |

| Apr-01 | |

| Mar-31 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite