|

|

|

|

|||||

|

|

|

Apogee Enterprises, Inc. APOG reported adjusted earnings per share (EPS) of 98 cents for the second-quarter fiscal 2026 (ended Aug. 30, 2025), surpassing the Zacks Consensus Estimate of 86 cents per share. The bottom line decreased 31.9% from the prior-year quarter.

Including one-time items, earnings in the quarter under review were $1.10 per share compared with $1.40 in the prior-year quarter.

Apogee generated revenues of $358 million in the quarter under review, up 4.6% from the year-ago quarter. The top line surpassed the Zacks Consensus Estimate of $334 million. This was mainly due to gains from the acquisition of UW Solutions and higher Architectural Services volumes, which were partially offset by lower Architectural Glass volumes and unfavorable product mix in Architectural Metals.

Apogee Enterprises, Inc. price-consensus-eps-surprise-chart | Apogee Enterprises, Inc. Quote

Cost of sales in the fiscal second quarter moved up 12.4% from the prior-year quarter to $275.6 million. The gross profit fell 15.1% from the prior-year quarter to $83 million. The gross margin expanded to 23.1% in the quarter under review from the prior-year quarter's 28.4%.

Selling, general and administrative expenses moved up 0.7% from the prior-year quarter to $56 million. The operating income fell 35.9% from the year-earlier quarter to $27 million. The operating margin in the reported quarter was 7.5% compared with the prior-year quarter's 12.3%.

In the fiscal second quarter, revenues in the Architectural Metals segment moved down 0.3% year over year to $141 million due to a less favorable mix. This was partially negated by higher volume and price. The segment's adjusted EBITDA was $20.8 million compared with the year-ago quarter's $22.2 million.

Revenues in the Architectural Glass segment fell 19.9% year over year to $72 million due to lower volume. The segment's adjusted EBITDA was around $12 million compared with $24 million in 2025.

Revenues in the Architectural Services segment improved 2.5% year over year to $100.5 million on improved volumes. The segment reported an adjusted EBITDA of $5 million, down 31.7% year over year.

Revenues in the Performance Surfaces segment surged 144% year over year to $48 million, reflecting the contributions from the UW Solutions acquisition. The segment reported an adjusted EBITDA of $11.2 million in the fiscal second quarter compared with the prior-year quarter's $4.6 million.

The Architectural Services segment's backlog came in at $792 million at the end of the fiscal second quarter compared with $682 million at the end of the prior quarter.

Apogee had cash and cash equivalents of $39.5 million at the end of the second-quarter fiscal 2026 compared with $41 million at the end of fiscal 2025. Cash provided by operating activities was $57.1 million in the quarter compared with the prior-year quarter’s $58.7 million.

Long-term debt was $270 million at the end of the second quarter of fiscal 2026, lower than $285 million at the end of fiscal 2025.

Apogee is revising its guidance for net revenues to $1.39-$1.42 billion for fiscal 2026, down from the prior stated $1.40-$1.44 billion. Its updated adjusted EPS guidance is $3.60-$3.90 compared with the prior stated $3.80-$4.20. The updated guidance includes unfavorable headwinds of 35-45 cents from tariffs.

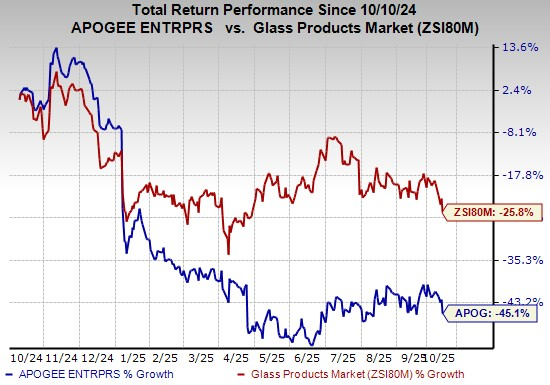

Shares of the company have lost 45.1% in the past year compared with the industry's decline of 25.8%.

O-I Glass, Inc. OI is expected to release its third-quarter 2025 results on Nov. 4, 2025. The Zacks Consensus Estimate for the company’s EPS is pegged at 44 cents for the third quarter, suggesting growth from a loss of 4 cents incurred in the prior-year quarter. The Zacks Consensus Estimate for total revenues is pinned at $1.65 billion, indicating a year-over-year decrease of 2.1%.

Apogee currently carries a Zacks Rank #3 (Hold).

Some better-ranked stocks from the Industrial Products sector are Life360, Inc. LIF and Crane Company CR. LIF sports a Zacks Rank #1 (Strong Buy) and CR carries a Zacks Rank #2 (Buy) at present. You can see the complete list of today's Zacks #1 Rank stocks here.

Life360 delivered an average trailing four-quarter earnings surprise of 487%. The Zacks Consensus Estimate for LIF’s 2025 earnings is pinned at 29 cents per share, which indicates a year-over-year upsurge of 583%. Life360’s shares have skyrocketed 155.6% in a year.

Crane Company delivered an average trailing four-quarter earnings surprise of 7.5%. The Zacks Consensus Estimate for CR’s 2025 earnings is pinned at $5.77 per share, which indicates year-over-year growth of 18.2%. The company’s shares have gained 16.1% in a year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-10 |

Life360 Stock Plunges On Mixed Second-Quarter Report, Soft Full-Year Outlook

LIF LIF -24.76%

Investor's Business Daily

|

| Aug-10 | |

| Aug-05 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-14 | |

| Jul-09 | |

| Jul-06 | |

| Jul-01 | |

| Jun-29 | |

| Jun-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite