|

|

|

|

|||||

|

|

|

Amphenol APH is set to report its third-quarter 2025 results on Oct. 22.

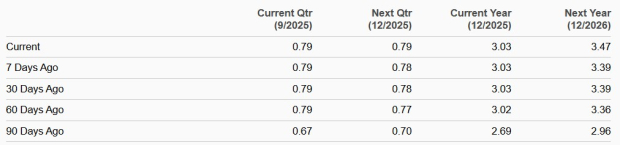

The company expects third-quarter 2025 earnings between 77 cents and 79 cents per share, indicating growth of 54% and 58% year over year. The Zacks Consensus Estimate for third-quarter 2025 earnings has been steady at 79 cents per share over the past 30 days, suggesting 58% growth from the figure reported in the year-ago quarter.

Amphenol expects third-quarter 2025 revenues between $5.4 billion and $5.5 billion, suggesting year-over-year growth in the 34-36% range. The Zacks Consensus Estimate for third-quarter revenues is pegged at $5.48 billion, indicating an increase of 35.6% from the figure reported in the year-ago quarter.

Amphenol’s earnings beat the Zacks Consensus Estimate in all the trailing four quarters, the average surprise being 16.25%.

Amphenol Corporation price-consensus-chart | Amphenol Corporation Quote

Let’s see how things have shaped up for the upcoming announcement.

Amphenol’s to-be-reported quarter's results are expected to have benefited significantly from sustained artificial intelligence (AI) infrastructure investments, continued defense modernization spending and strong contribution from acquisitions including CIT, Lutze, CommScope’s COMM Andrew business, LifeSync, Narda-MITEQ, XMA and Q Microwave.

A strong order backlog heading into the quarter likely acted as an additional tailwind. Orders surged 36% year over year and 4% sequentially to $5.52 billion in the second quarter, resulting in a book-to-bill ratio of 0.98 to 1. This healthy order environment is expected to have translated into sustained revenue momentum for the third quarter.

APH’s results are expected to have benefited from diversified end markets. A plethora of acquisitions are expected to have benefited defense sales on a sequential basis in the third quarter of 2025. Amphenol’s leading position in the defense interconnect market has been a tailwind. Commercial aerospace is expected to have increased in the low single digits range on a sequential basis. Communications networks sales are expected to have remained strong due to positive impact of Andrew acquisition. Mobile devices sales are expected to have benefited from strong demand for antennas, interconnect products and mechanisms designed in across a broad range of next-generation mobile devices

Expansion in alternative energy, instrumentation, medical, industrial EV and factory automation are expected to have driven sales in the industrial end-market despite negative impact from seasonality. The IT datacom segment sales is expected to increased in the mid-to-high single digits on a sequential basis, driven by strong demand for high-speed and power interconnect products despite strong comparisons.

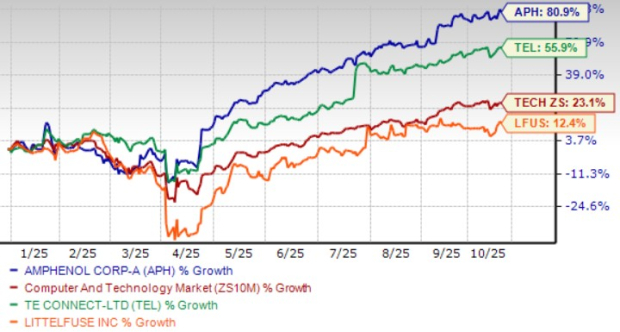

Amphenol shares have appreciated 81% year to date (YTD), outperforming the Zacks Computer and Technology sector’s return of 23.1%.

APH has outperformed broader sector peers, including TE Connectivity TEL and Littelfuse LFUS YTD. TE Connectivity and Littelfuse shares have appreciated 56% and 12.4%, respectively.

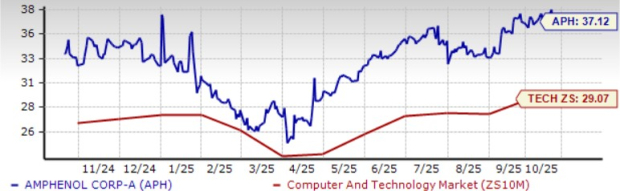

APH stock is trading at a premium, as suggested by the Value Score of F. In terms of the forward 12-month price/earnings, APH is trading at 37.12X, higher than the broader sector’s 29.07X, TE Connectivity’s 23.44X and Littelfuse’s 21.74X.

Amphenol continues to expand its portfolio and market reach through targeted acquisitions across communications, medical and defense verticals. Addition of Narda-MITEQ, XMA and Q Microwave has strengthened APH’s presence in RF interconnect and active RF components. The CIT acquisition has been benefiting the commercial aerospace end-market, while the Andrew acquisition from CommScope has benefited sales in the communications networks end-market.

In early August, Amphenol announced a definitive agreement to acquire CommScope’s Connectivity and Cable Solutions (“CCS”) business for $10.5 billion in cash. The deal expands Amphenol’s interconnect product capabilities in the fast-growing IT datacom market. The CCS acquisition will diversify the company’s broad portfolio of fiber optic and other interconnect product solutions in the communications networks and industrial markets. The CCS business is expected to have sales and EBITDA margins of $3.6 billion and 26% in 2025, respectively.

Amphenol announced a definitive agreement to acquire Trexon for approximately $1 billion in cash. Trexon is expected to have 2025 sales and EBITDA margins of $290 million and 26%, respectively.

Amphenol’s AI-driven growth in the IT datacom end-market, accretive acquisitions and steady demand in defense and commercial aerospace end-markets support growth prospects. These factors justify the premium valuation.

APH currently has a Zacks Rank #1 (Strong Buy) and a Growth Score of B, a favorable combination that offers a strong investment opportunity, per the Zacks Proprietary methodology. You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite