|

|

|

|

|||||

|

|

|

What a fantastic six months it’s been for Palantir Technologies. Shares of the company have skyrocketed 92.1%, hitting $180.59. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is it too late to buy PLTR? Find out in our full research report, it’s free for active Edge members.

Named after the all-seeing stones in "Lord of the Rings," Palantir Technologies (NASDAQ:PLTR) develops software platforms that help government agencies and enterprises integrate, analyze, and operationalize their data for decision-making.

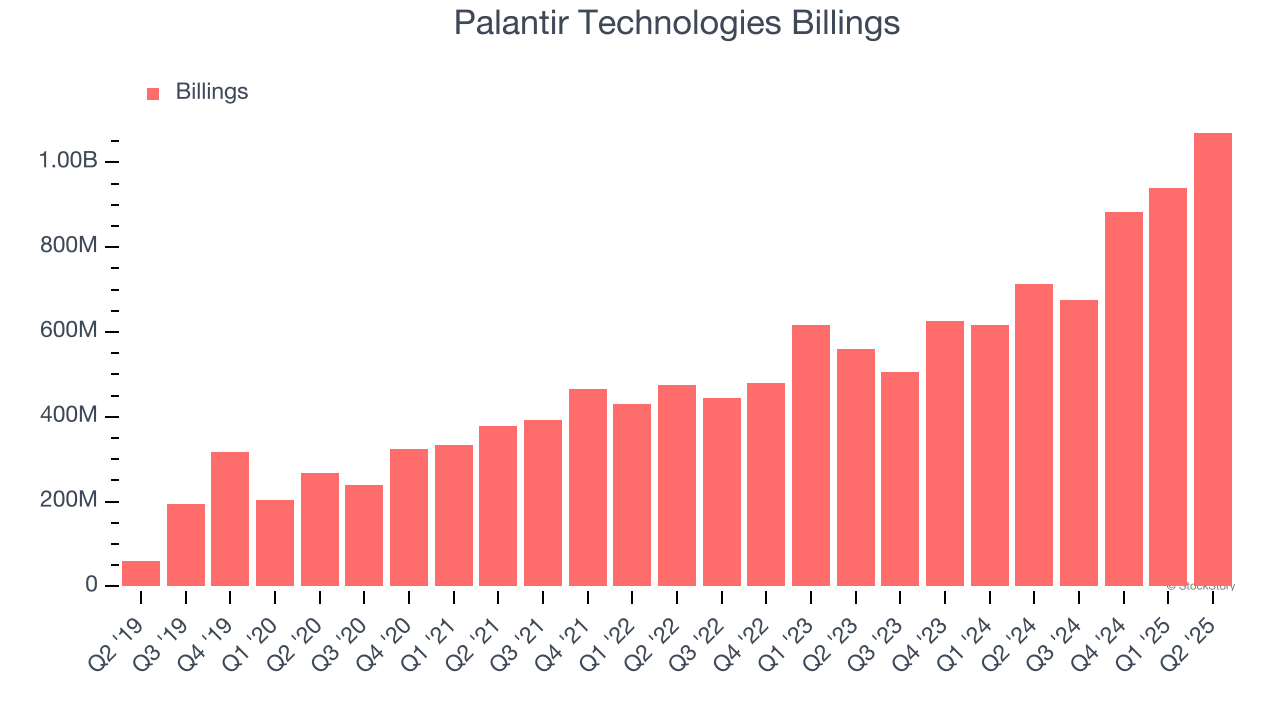

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Palantir Technologies’s billings punched in at $1.07 billion in Q2, and over the last four quarters, its year-on-year growth averaged 44.2%. This performance was fantastic, indicating robust customer demand. The high level of cash collected from customers also enhances liquidity and provides a solid foundation for future investments and growth.

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Palantir Technologies is extremely efficient at acquiring new customers, and its CAC payback period checked in at 12.5 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation. These dynamics give Palantir Technologies more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

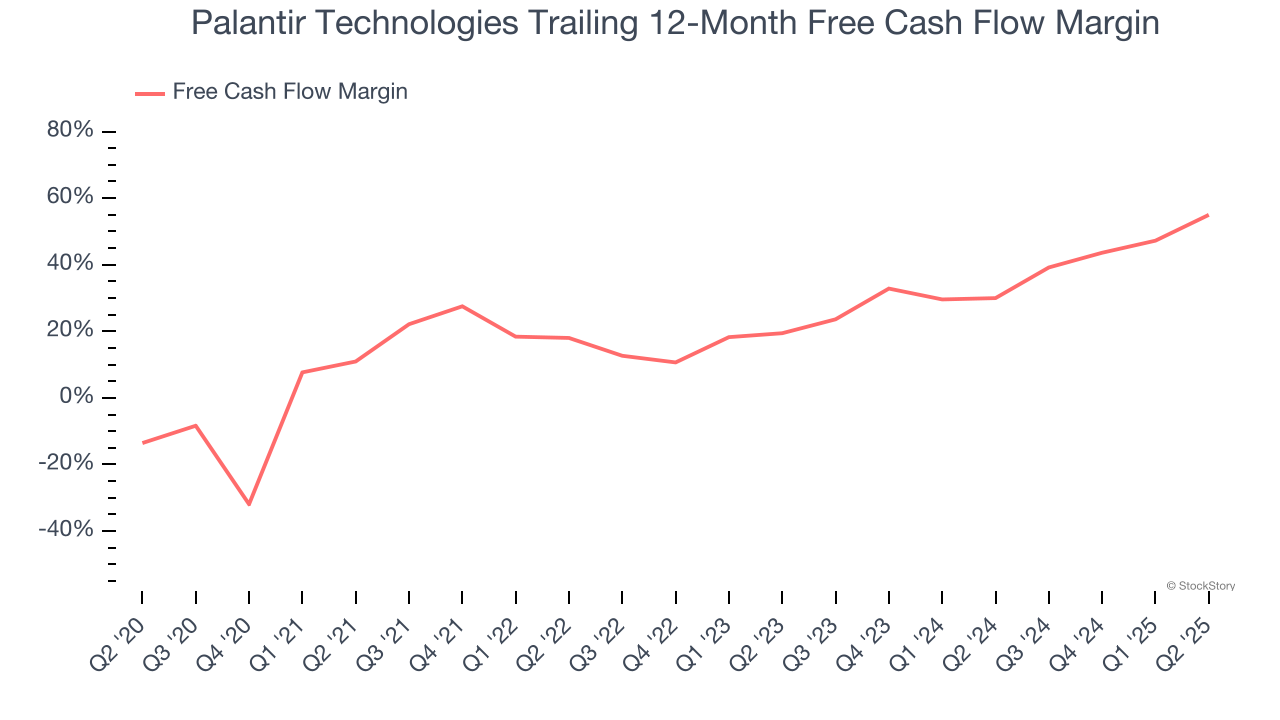

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Palantir Technologies has shown terrific cash profitability, driven by its lucrative business model and cost-effective customer acquisition strategy that enable it to stay ahead of the competition through investments in new products rather than sales and marketing. The company’s free cash flow margin was among the best in the software sector, averaging an eye-popping 55% over the last year.

These are just a few reasons why we're bullish on Palantir Technologies, and after the recent surge, the stock trades at 95.1× forward price-to-sales (or $180.59 per share). Is now a good time to buy despite the apparent froth? See for yourself in our in-depth research report, it’s free for active Edge members.

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| 54 min | |

| 59 min | |

| 1 hour | |

| 2 hours | |

| 3 hours | |

| 4 hours | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 |

Stock Market Today: Dow, Nasdaq Eke Out Gains; Gold, Silver Names Slide (Live Coverage)

PLTR

Investor's Business Daily

|

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 |

Stock Market Today: Nasdaq, Dow Climb; Airline Name Flies Higher (Live Coverage)

PLTR

Investor's Business Daily

|

| Feb-17 | |

| Feb-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite