|

|

|

|

|||||

|

|

|

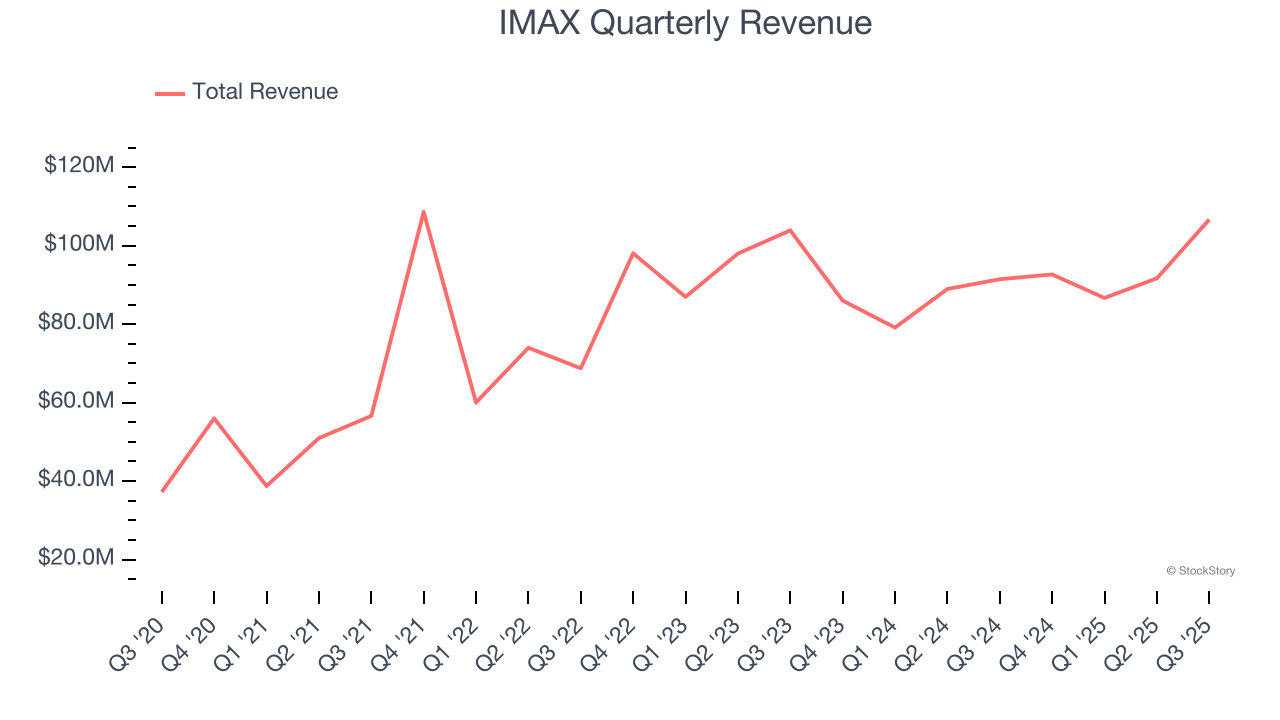

Premium cinema technology company IMAX (NYSE:IMAX) beat Wall Street’s revenue expectations in Q3 CY2025, with sales up 16.6% year on year to $106.7 million. Its non-GAAP profit of $0.47 per share was 20.3% above analysts’ consensus estimates.

Is now the time to buy IMAX? Find out by accessing our full research report, it’s free for active Edge members.

“IMAX is moving into a new position — building to something bigger — and our performance for the quarter and year to date demonstrate we’re breaking out and delivering at a higher level,” said Rich Gelfond, CEO of IMAX.

Originally developed for World Expo '67 in Montreal as an innovative projection system, IMAX (NYSE:IMAX) provides proprietary large-format cinema technology and systems that deliver immersive movie experiences with enhanced image quality and sound.

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $377.7 million in revenue over the past 12 months, IMAX is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

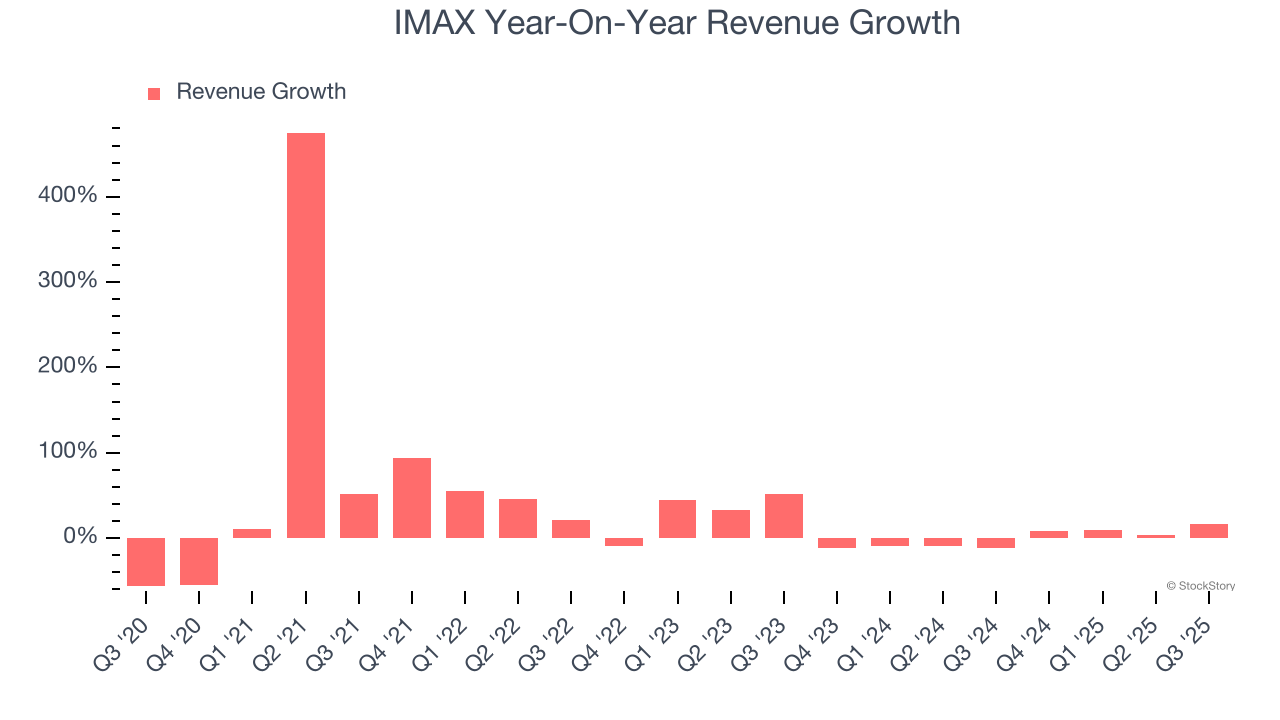

As you can see below, IMAX grew its sales at an excellent 13% compounded annual growth rate over the last five years. This is an encouraging starting point for our analysis because it shows IMAX’s demand was higher than many business services companies.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. IMAX’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 1.2% over the last two years.

This quarter, IMAX reported year-on-year revenue growth of 16.6%, and its $106.7 million of revenue exceeded Wall Street’s estimates by 0.6%.

Looking ahead, sell-side analysts expect revenue to grow 13.3% over the next 12 months, an improvement versus the last two years. This projection is admirable and indicates its newer products and services will fuel better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

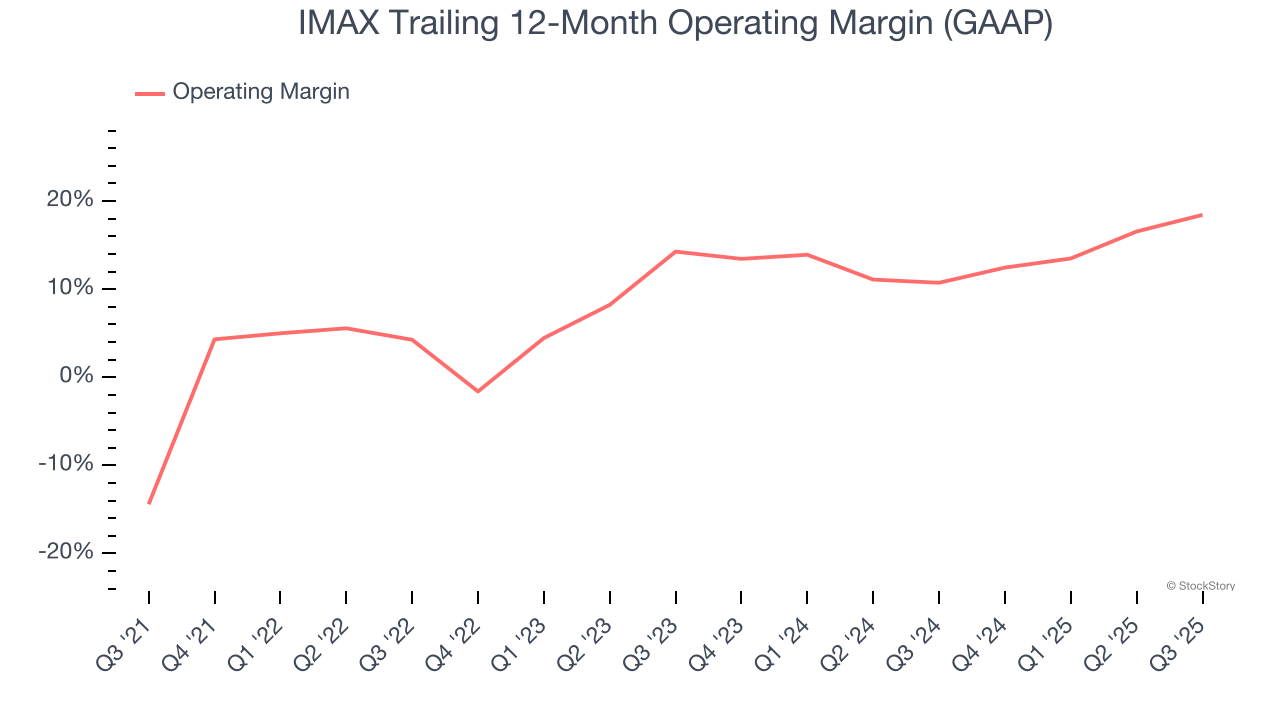

IMAX was profitable over the last five years but held back by its large cost base. Its average operating margin of 9% was weak for a business services business.

On the plus side, IMAX’s operating margin rose by 32.8 percentage points over the last five years, as its sales growth gave it immense operating leverage.

This quarter, IMAX generated an operating margin profit margin of 27.2%, up 6 percentage points year on year. This increase was a welcome development and shows it was more efficient.

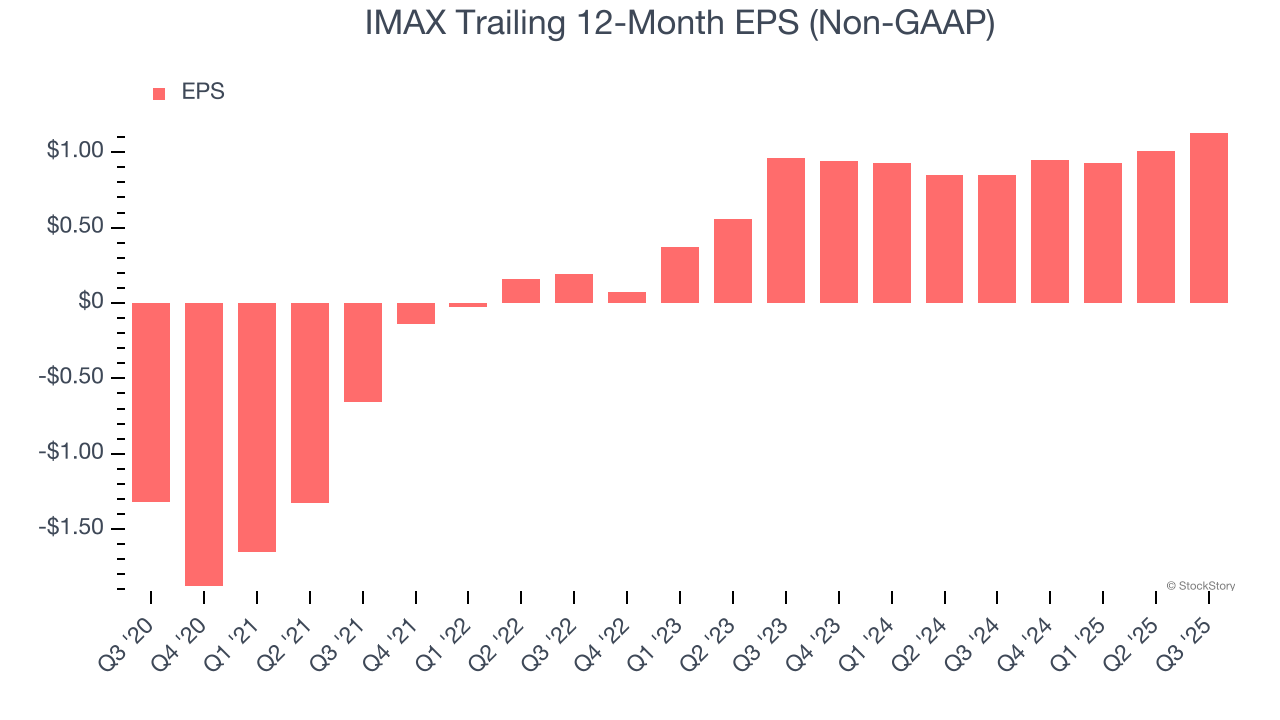

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

IMAX’s full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it’s at an inflection point.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

IMAX’s EPS grew at an unimpressive 8.5% compounded annual growth rate over the last two years. On the bright side, this performance was higher than its 1.2% annualized revenue declines and tells us management adapted its cost structure in response to a challenging demand environment.

We can take a deeper look into IMAX’s earnings to better understand the drivers of its performance. IMAX’s operating margin has expanded over the last two years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q3, IMAX reported adjusted EPS of $0.47, up from $0.35 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects IMAX’s full-year EPS of $1.13 to grow 42.3%.

It was good to see IMAX beat analysts’ EPS expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 3.2% to $33.10 immediately after reporting.

IMAX had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| May-10 | |

| May-05 | |

| May-01 | |

| May-01 | |

| Apr-30 | |

| Apr-29 | |

| Apr-19 | |

| Apr-16 | |

| Mar-30 | |

| Mar-23 | |

| Mar-22 | |

| Mar-15 | |

| Mar-10 | |

| Mar-09 | |

| Mar-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite