|

|

|

|

|||||

|

|

|

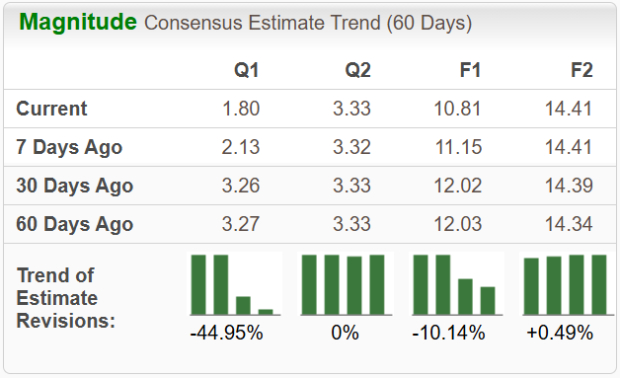

AbbVie ABBV is set to report third-quarter 2025 earnings on Oct. 31, before the opening bell. The Zacks Consensus Estimate for the quarter’s sales and earnings is pegged at $15.59 billion and $1.80 per share, respectively. The company’s earnings estimates for 2025 have declined from $12.02 per share to $10.81 in the past 30 days.

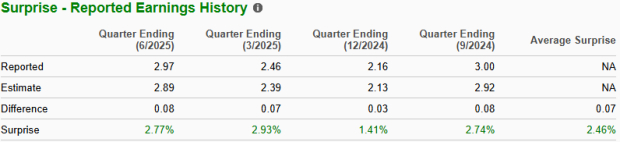

AbbVie’s performance has been impressive, with its earnings exceeding expectations in each of the trailing four quarters. It delivered a trailing four-quarter average earnings surprise of 2.46%. In the last reported quarter, the pharma giant delivered an earnings surprise of 2.77%.

Per our proven model, companies with the combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) have a good chance of delivering an earnings beat. This is not the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

AbbVie currently has an Earnings ESP of 0.00% and a Zacks Rank #4 (Sell). You can see the complete list of today’s Zacks #1 Rank stocks here.

For the third quarter of 2025, AbbVie expects adjusted earnings to be in the range of $1.74-$1.78 per share. The company expects net revenues of approximately $15.5 billion. Currency is expected to have a positive impact of around 1% on sales.

AbbVie’s top-line growth in the quarter is likely to have been driven by higher sales of newer immunology drugs, Skyrizi and Rinvoq. Approvals in new indications are expected to have been driving strong revenues for these drugs. The Zacks Consensus Estimate for Skyrizi sales is pegged at $4.56 billion, while the same for Rinvoq is pinned at $2.16 billion. Our model estimate for Skyrizi and Rinvoq sales is pegged at $4.54 billion and $2.16 billion, respectively.

ABBV lost patent protection for its blockbuster immunology drug Humira in the United States in January 2023 and has been facing sales erosion ever since. The drug lost exclusivity in ex-U.S. territories in 2018. The Zacks Consensus Estimate for Humira sales is pegged at $1.15 billion, while our estimate for the same is pinned at $1.16 billion.

In the oncology franchise, we expect J&J JNJ-partnered Imbruvica sales to have declined due to competition from novel oral therapies. The Zacks Consensus Estimate and our model estimate for the J&J-partnered drug’s sales are pegged at $708 million and $703 million, respectively.

Roche RHHBY-partnered Venclexta sales are likely to have risen as new patient starts might have improved, driven by strong demand for both CLL and AML indications. The Zacks Consensus Estimate and our model estimate for the Roche-partnered drug’s sales are pegged at $712 million and $727 million, respectively.

We expect AbbVie to record modest revenues from the recently approved lung cancer therapy Emrelis.

Sales of the neuroscience franchise have shown strong growth in recent quarters. The growth is likely to have been driven by higher sales of Botox Therapeutic, depression drug Vraylar and new migraine drugs — Ubrelvy and Qulipta. Similar to the previous quarters, we expect most of the sales of the recently launched Parkinson’s disease drug Vyalev coming from ex-U.S. markets in the to-be-reported quarter, though U.S. uptake should start contributing as well.

The Zacks Consensus Estimate and our model estimate for neuroscience product sales are pegged at $2.74 billion and $2.73 billion, respectively.

In the aesthetics franchise, we expect overall sales to have recovered from the sluggish sales of Botox and Juvederm fillers, as experienced in the past few quarters. The improvement is likely driven by stabilizing demand for the facial injectable market in the United States and easing macroeconomic pressures, which is expected to have improved consumer sentiment. The Zacks Consensus Estimate and our model estimate for aesthetics product sales are pegged at $1.27 billion and $1.30 billion, respectively.

Nonetheless, a single quarter’s results are not so important for long-term investors. Let us delve deeper to understand whether to buy, sell or hold the stock at present.

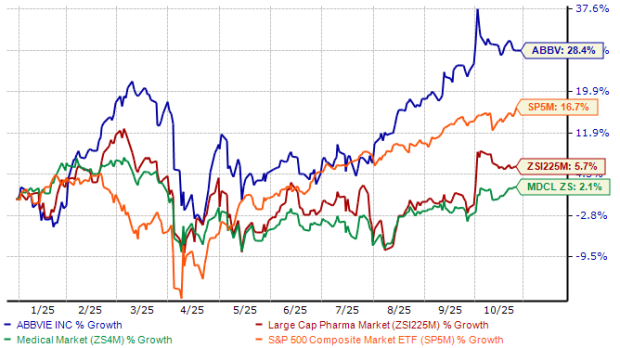

Shares of AbbVie have surged over 28% this year so far compared with the industry’s 6% growth. The stock has also outperformed the sector and the S&P 500 index, as seen in the chart below.

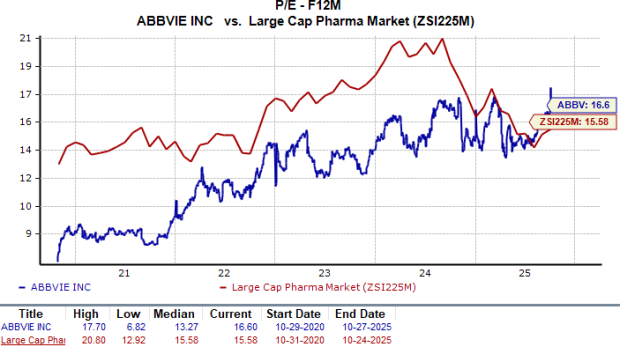

From a valuation standpoint, AbbVie is trading at a premium to the industry. Based on the price/earnings (P/E) ratio, the company’s shares currently trade at 16.60 times forward earnings, slightly higher than its industry’s average of 15.58. The stock is also trading above its five-year mean of 13.27.

AbbVie has faced its biggest challenge — Humira biosimilar erosion — quite well through the successful launches of Skyrizi and Rinvoq. Driven by the performance of these two drugs, the company expects to return to robust revenue growth in 2025, just the second year following the U.S. Humira LOE, with a projected high single-digit revenue CAGR through 2029.

While competitive pressure on Imbruvica and declining filler sales pose some headwinds, sales growth from drugs like Venclexta, Vraylar, Ubrelvy, Elahere, Epkinly and Qulipta helps more than offset these losses. These therapies, though smaller in scale than the immunology medications, provide valuable diversification and steady growth that support AbbVie’s overall performance.

However, the company’s recent spree of acquisitions and licensing deals has begun to weigh on near-term earnings expectations. For the third quarter of 2025, AbbVie expects its EPS to be impacted by $1.50 due to an IPR&D charge of around $2.7 billion, reflecting payments tied to its aggressive business development activities. This includes the recent acquisition of privately held biotech Capstan Therapeutics, which added an investigational in vivo tLNP anti-CD19 CAR-T therapy to AbbVie’s immunology pipeline. The deal was valued at up to $2.1 billion.

While these transactions broaden AbbVie’s pipeline reach, they have also added substantial near-term expenses that are weighing on profitability and triggering downward revisions in EPS estimates.

Given the elevated IPR&D expenses, short-term investors may consider exiting ABBV stock, as profitability and EPS are likely to remain under pressure in the near term. However, long-term investors may choose to stay invested, since rising sales from Skyrizi, Rinvoq, and other key therapies, along with an expanding pipeline, highlight AbbVie’s sustained efforts to strengthen its long-term growth and profitability outlook.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 6 hours | |

| 8 hours | |

| 13 hours | |

| 18 hours | |

| 22 hours | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite