|

|

|

|

|||||

|

|

|

Over the past six months, MasterCraft has been a great trade, beating the S&P 500 by 8.5%. Its stock price has climbed to $22.01, representing a healthy 32.4% increase. This run-up might have investors contemplating their next move.

Is now the time to buy MasterCraft, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free for active Edge members.

Despite the momentum, we're swiping left on MasterCraft for now. Here are three reasons you should be careful with MCFT and a stock we'd rather own.

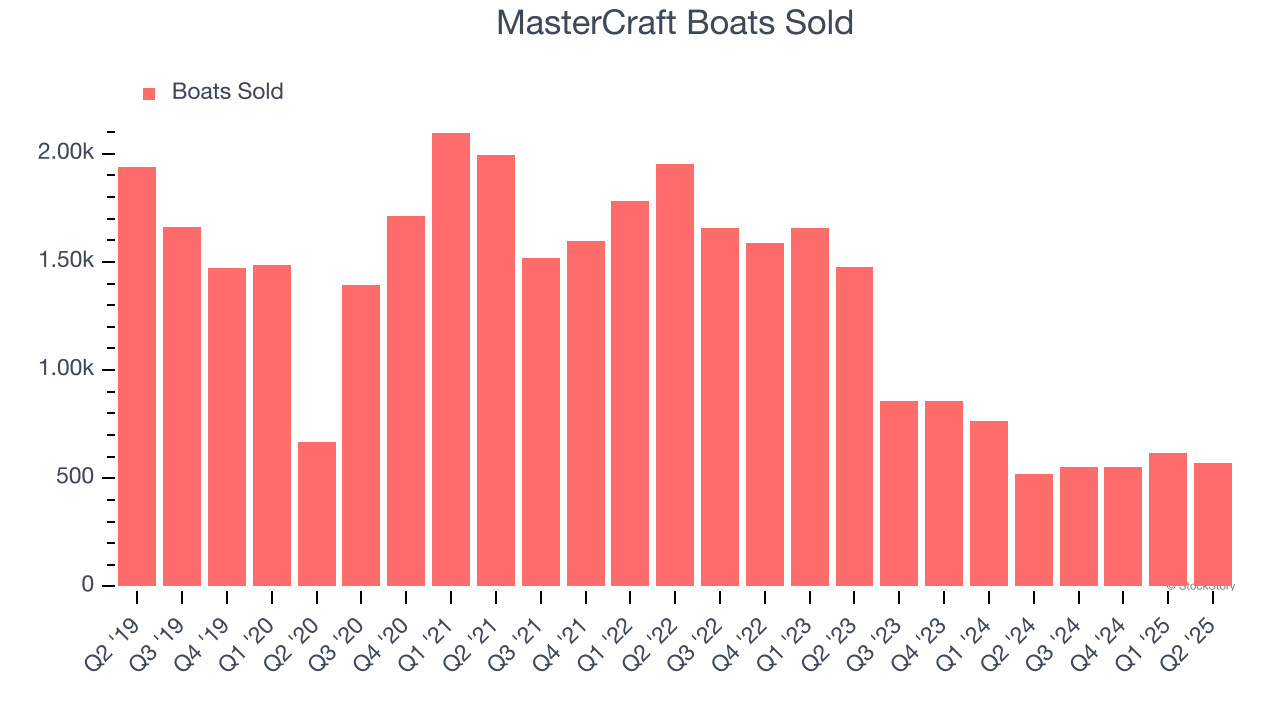

Revenue growth can be broken down into changes in price and volume (for companies like MasterCraft, our preferred volume metric is boats sold). While both are important, the latter is the most critical to analyze because prices have a ceiling.

MasterCraft’s boats sold came in at 570 in the latest quarter, and over the last two years, averaged 36.7% year-on-year declines. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests MasterCraft might have to lower prices or invest in product improvements to grow, factors that can hinder near-term profitability.

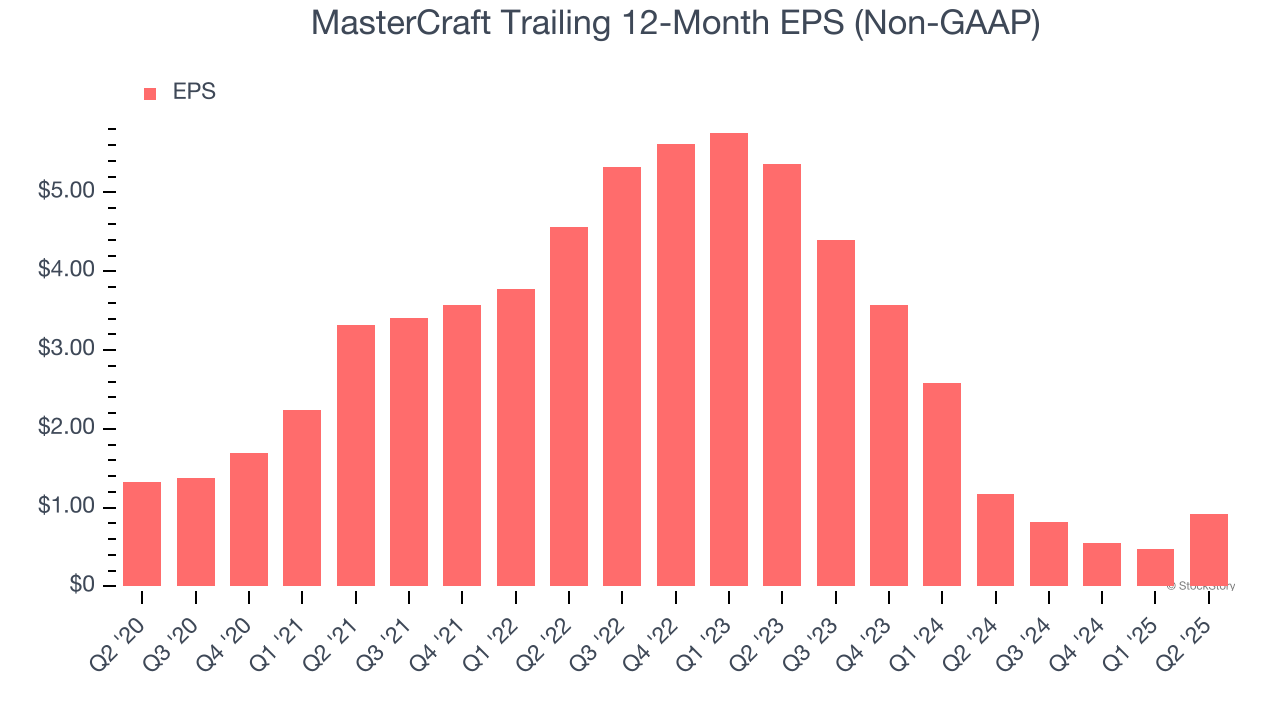

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for MasterCraft, its EPS declined by 7% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, MasterCraft’s ROIC has decreased significantly over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

MasterCraft isn’t a terrible business, but it isn’t one of our picks. With its shares beating the market recently, the stock trades at 17.7× forward P/E (or $22.01 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are more exciting stocks to buy at the moment. We’d suggest looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

When Trump unveiled his aggressive tariff plan in April 2025, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Jun-29 | |

| May-15 | |

| May-07 | |

| May-07 | |

| May-07 | |

| May-06 | |

| Apr-15 | |

| Apr-14 | |

| Mar-16 | |

| Mar-09 | |

| Mar-06 | |

| Mar-05 | |

| Mar-05 | |

| Mar-04 | |

| Mar-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite