|

|

|

|

|||||

|

|

|

BGC currently trades at $9.14 per share and has shown little upside over the past six months, posting a middling return of 0.9%. The stock also fell short of the S&P 500’s 23.8% gain during that period.

Does this present a buying opportunity for BGC? Or is its underperformance reflective of its story and business quality? Find out in our full research report, it’s free for active Edge members.

Tracing its roots back to 1945 and named after founder Bernard Gerald Cantor, BGC Group (NASDAQ:BGC) operates a global brokerage and financial technology platform that facilitates trading across fixed income, foreign exchange, equities, energy, and commodities markets.

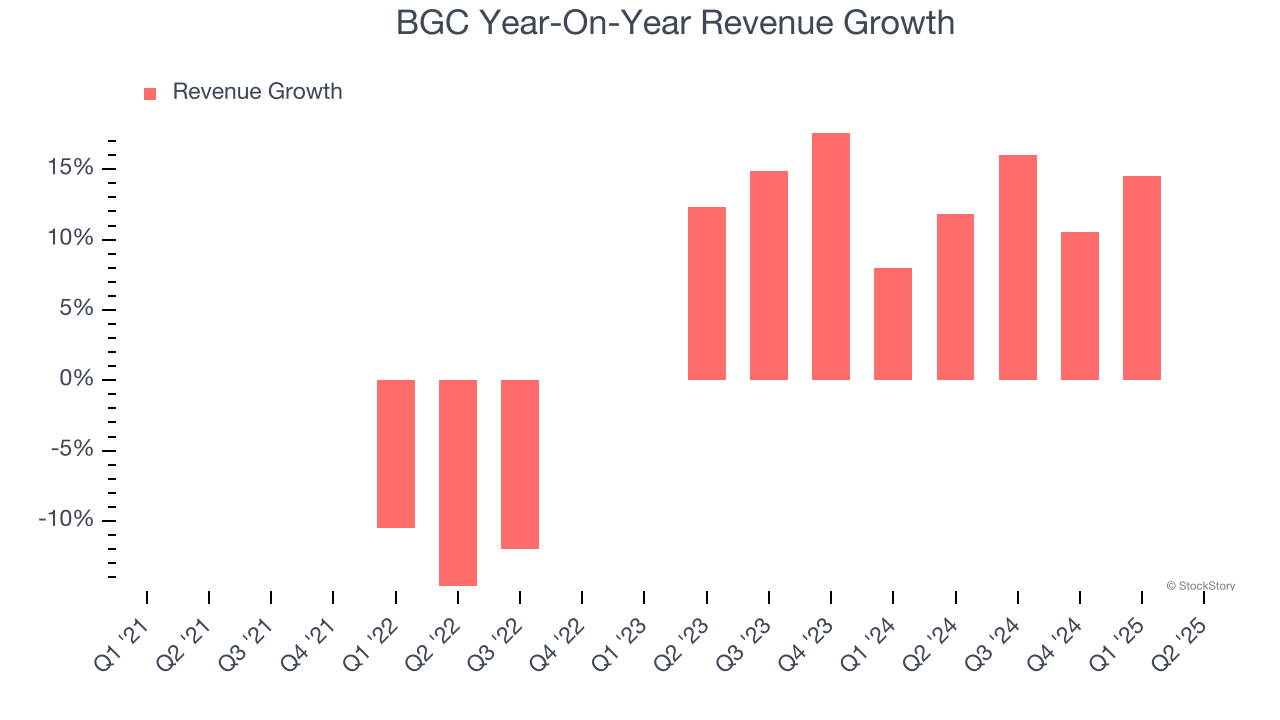

Long-term growth is the most important, but within financials, a stretched historical view may miss recent interest rate changes and market returns. BGC’s annualized revenue growth of 16.8% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

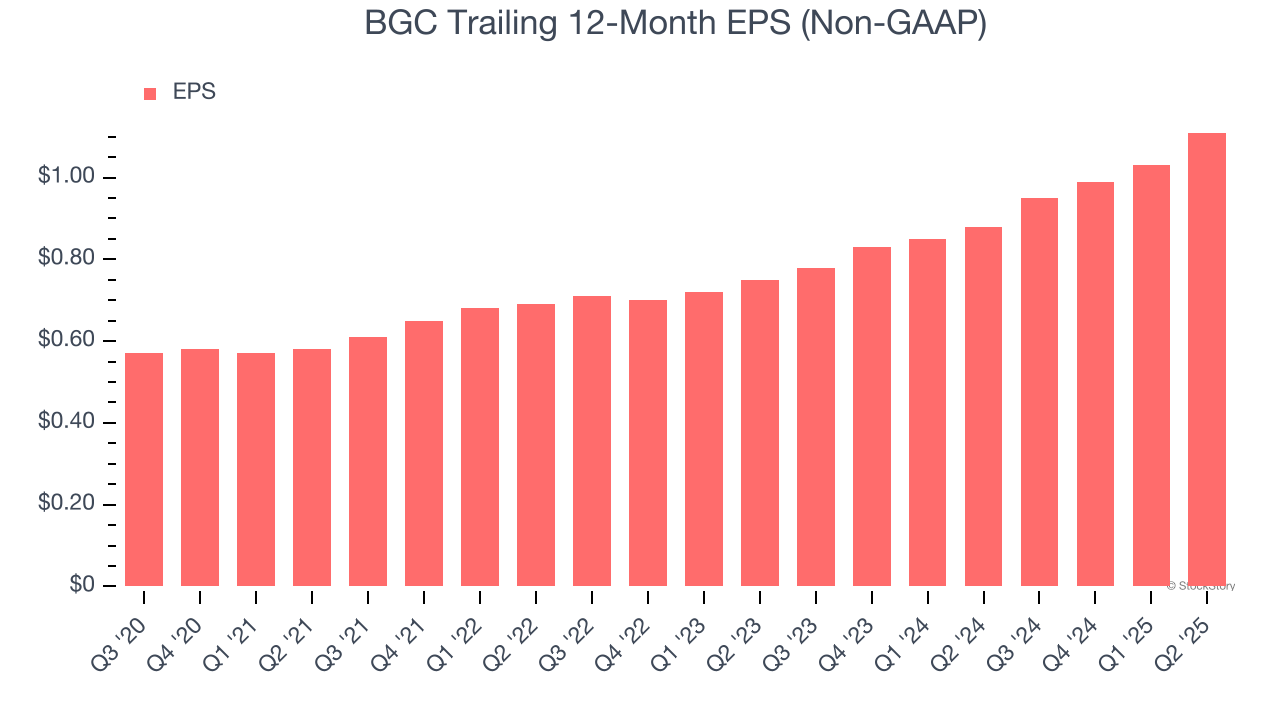

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

BGC’s EPS grew at a solid 13.1% compounded annual growth rate over the last five years, higher than its 5% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

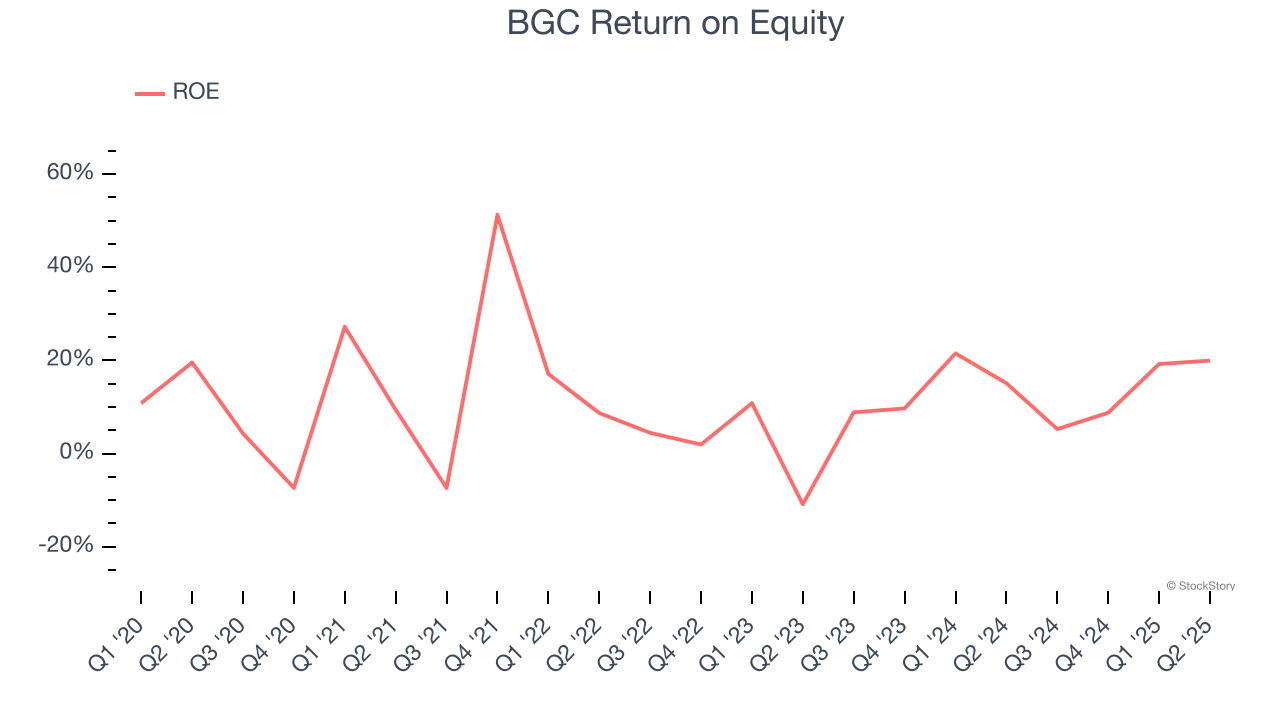

Return on equity, or ROE, tells us how much profit a company generates for each dollar of shareholder equity, a key funding source for banks. Over a long period, banks with high ROE tend to compound shareholder wealth faster through retained earnings, buybacks, and dividends.

Over the last five years, BGC has averaged an ROE of 10.9%, respectable for a company operating in a sector where the average shakes out around 10% and those putting up 25%+ are greatly admired. This shows BGC has a narrow competitive moat.

There are definitely things to like about BGC. With its shares underperforming the market lately, the stock trades at 7.1× forward P/E (or $9.14 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free for active Edge members.

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-28 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-15 | |

| Jun-29 | |

| Jun-25 | |

| Jun-18 | |

| Jun-01 | |

| May-07 | |

| May-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite