|

|

|

|

|||||

|

|

|

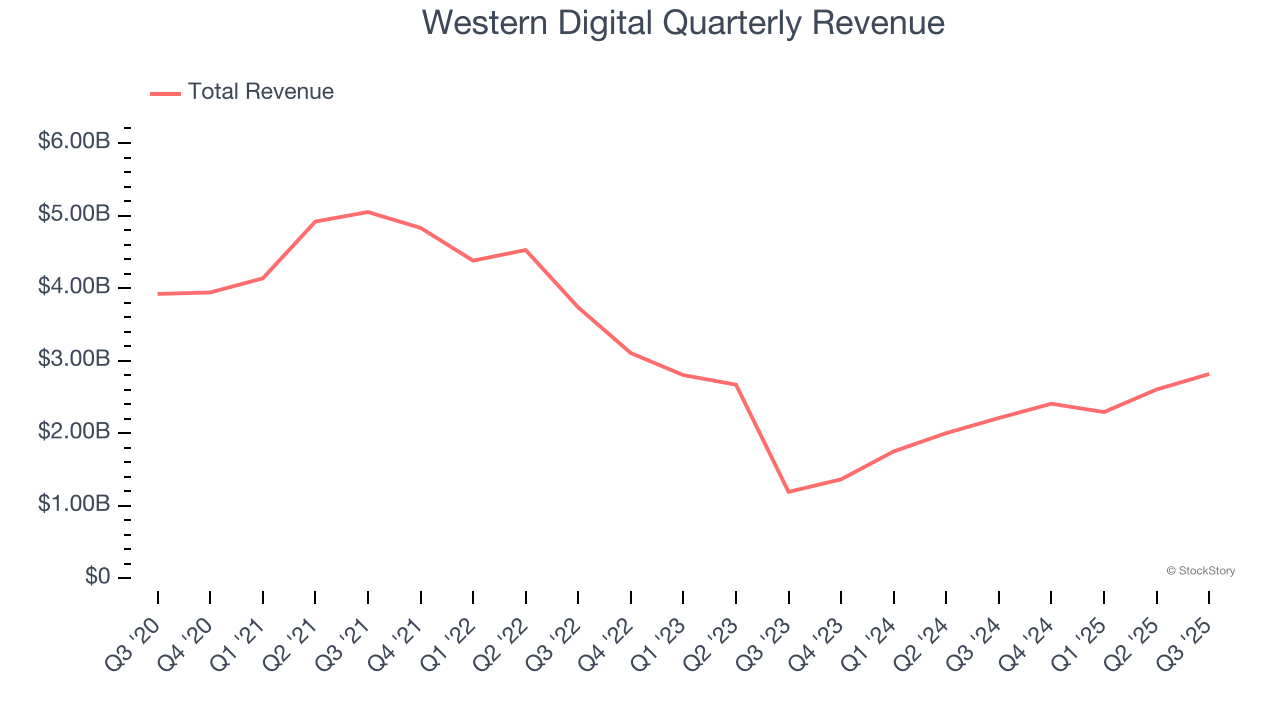

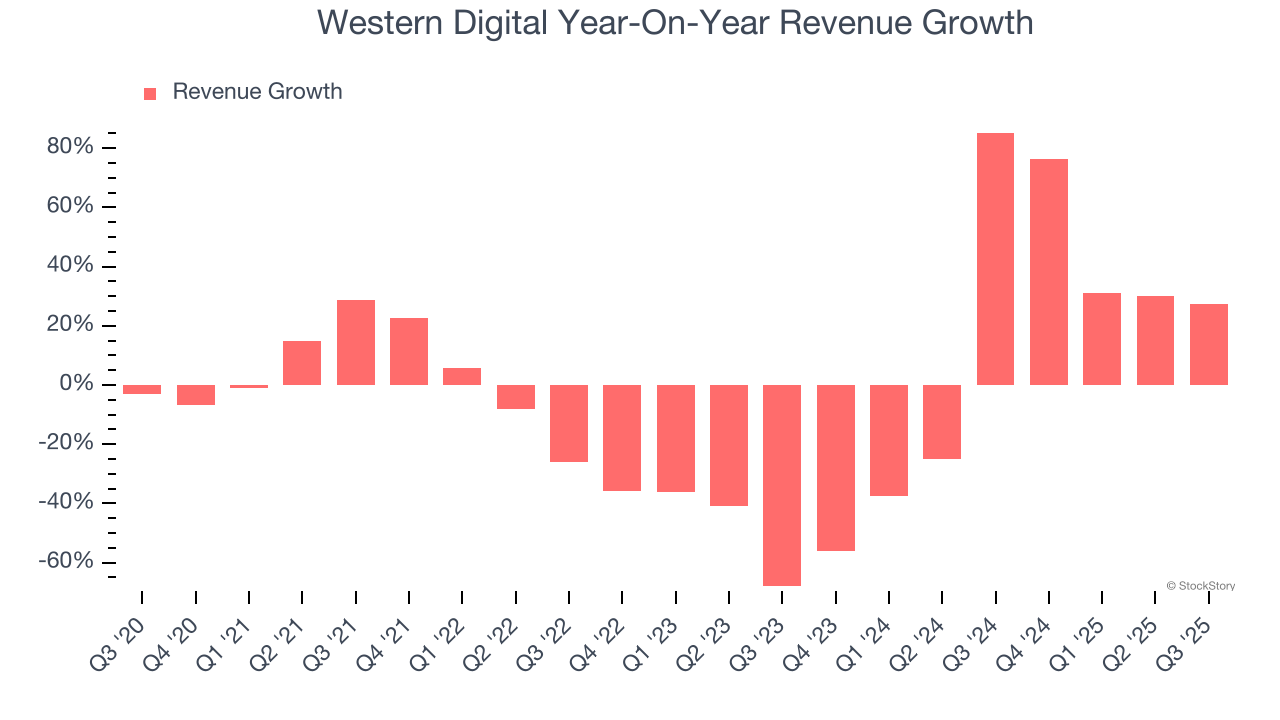

Leading data storage manufacturer Western Digital (NASDAQ: WDC) reported Q3 CY2025 results exceeding the market’s revenue expectations, with sales up 27.4% year on year to $2.82 billion. Its non-GAAP profit of $1.78 per share was 12.9% above analysts’ consensus estimates.

Is now the time to buy Western Digital? Find out by accessing our full research report, it’s free for active Edge members.

“Western Digital continues to execute well in a strong demand environment driven by growth of data storage in the cloud. In our fiscal first quarter, we achieved revenue and gross margin above the high end of our guidance range, while delivering strong free cash flow,” said Irving Tan, CEO of Western Digital.

Founded in 1970 by a Motorola employee, Western Digital (NASDAQ: WDC) is a leading producer of hard disk drives, SSDs and flash memory.

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Western Digital’s demand was weak and its revenue declined by 9.4% per year. This was below our standards and suggests it’s a lower quality business. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

We at StockStory place the most emphasis on long-term growth, but within semiconductors, a half-decade historical view may miss new demand cycles or industry trends like AI. Western Digital’s annualized revenue growth of 1.8% over the last two years is above its five-year trend, but we were still disappointed by the results.

This quarter, Western Digital reported robust year-on-year revenue growth of 27.4%, and its $2.82 billion of revenue topped Wall Street estimates by 2.8%. Beyond the beat, this marks 5 straight quarters of growth, implying that Western Digital is in the middle of its cycle - a typical upcycle generally lasts 8-10 quarters.

Looking ahead, sell-side analysts expect revenue to grow 14.9% over the next 12 months, an improvement versus the last two years. This projection is particularly noteworthy for a company of its scale and implies its newer products and services will fuel better top-line performance.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

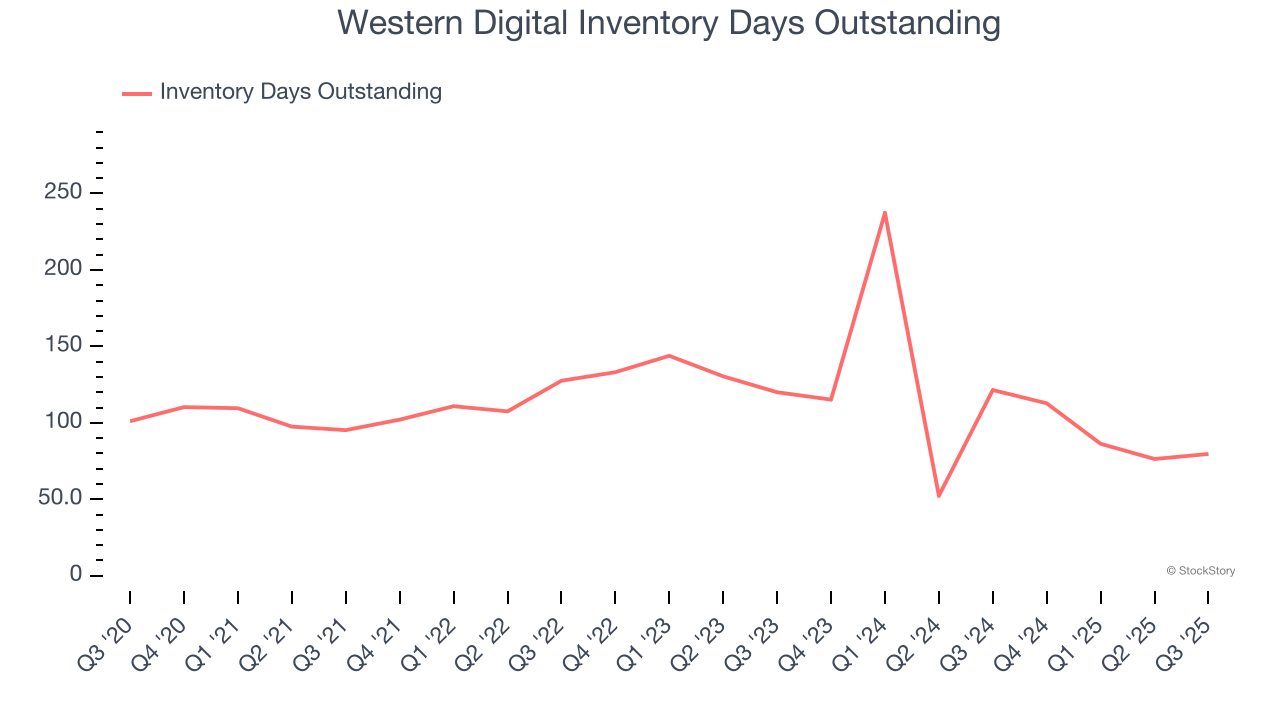

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Western Digital’s DIO came in at 80, which is 34 days below its five-year average. These numbers show that despite the recent increase, there’s no indication of an excessive inventory buildup.

It was good to see Western Digital beat analysts’ revenue, operating profit, and EPS expectations this quarter. Zooming out, we think this was a good print. The stock traded up 12.3% to $155.18 immediately after reporting.

Western Digital put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-22 | |

| Feb-22 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-18 | |

| Feb-18 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite