|

|

|

|

|||||

|

|

|

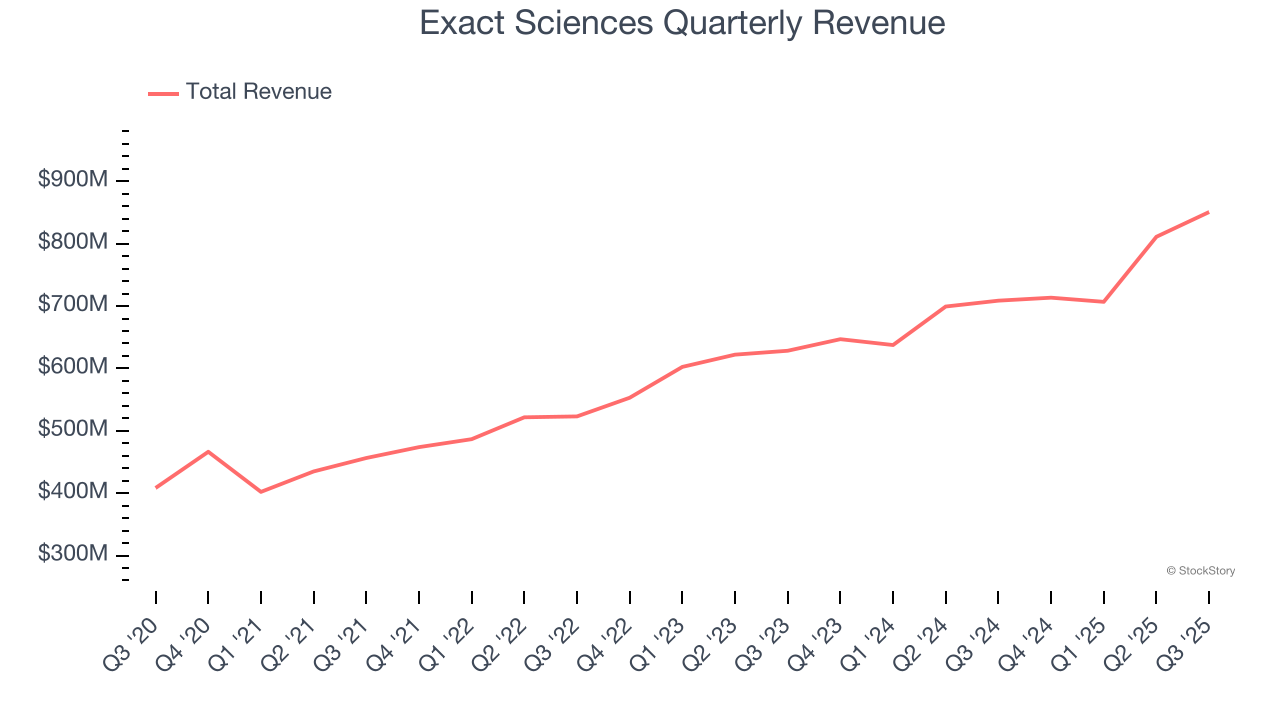

Diagnostic company Exact Sciences Corporation (NASDAQ:EXAS) reported revenue ahead of Wall Streets expectations in Q3 CY2025, with sales up 20% year on year to $850.7 million. The company’s full-year revenue guidance of $3.23 billion at the midpoint came in 2.2% above analysts’ estimates. Its non-GAAP profit of $0.24 per share was 49.4% above analysts’ consensus estimates.

Is now the time to buy Exact Sciences? Find out by accessing our full research report, it’s free for active Edge members.

With a mission to detect cancer earlier when it's more treatable, Exact Sciences (NASDAQ:EXAS) develops and markets cancer screening and diagnostic tests, including its flagship Cologuard stool-based colorectal cancer screening test.

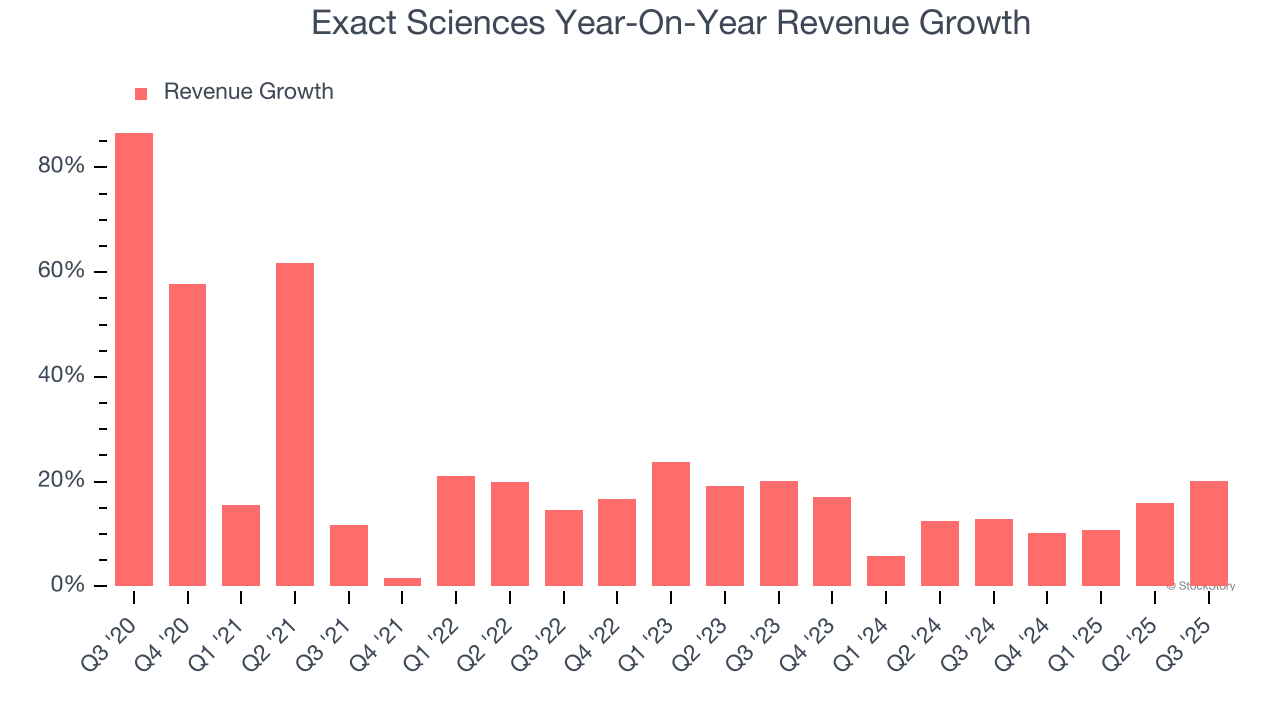

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Exact Sciences grew its sales at an impressive 18.5% compounded annual growth rate. Its growth beat the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Exact Sciences’s annualized revenue growth of 13.2% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

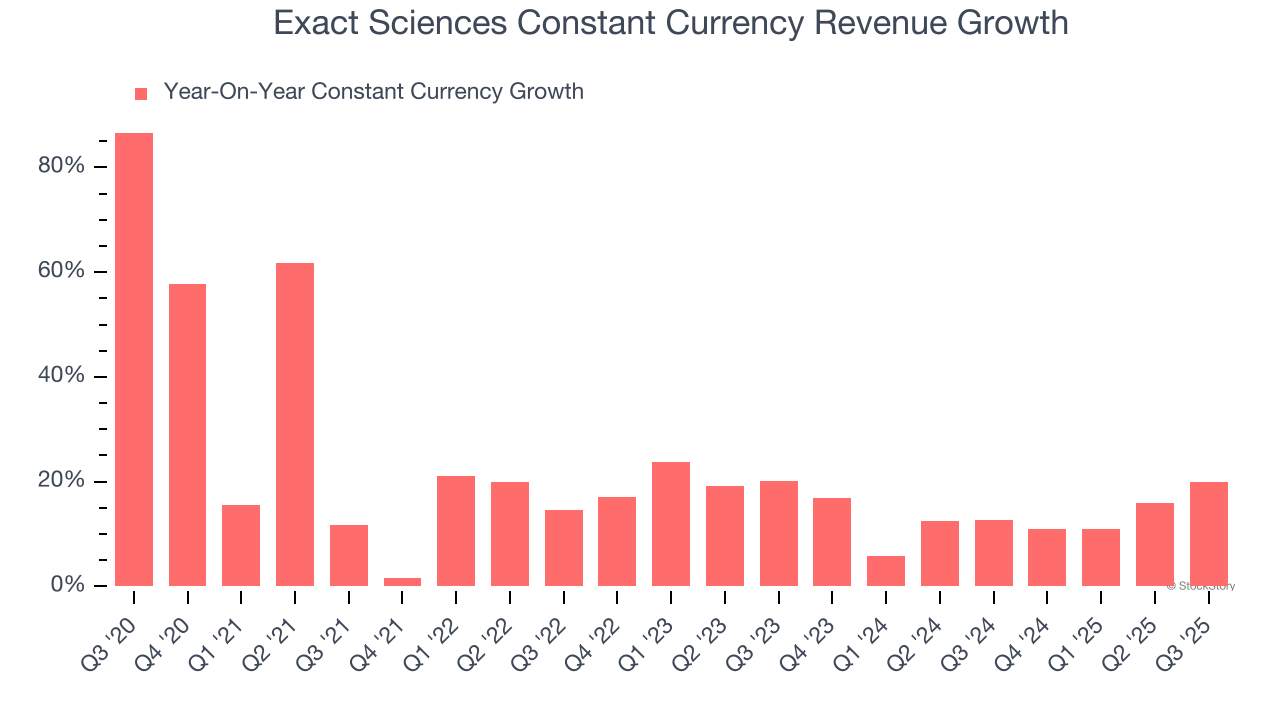

Exact Sciences also reports sales performance excluding currency movements, which are outside the company’s control and not indicative of demand. Over the last two years, its constant currency sales averaged 13.2% year-on-year growth. Because this number aligns with its normal revenue growth, we can see that Exact Sciences has properly hedged its foreign currency exposure.

This quarter, Exact Sciences reported robust year-on-year revenue growth of 20%, and its $850.7 million of revenue topped Wall Street estimates by 5%.

Looking ahead, sell-side analysts expect revenue to grow 12% over the next 12 months, similar to its two-year rate. Despite the slowdown, this projection is healthy and suggests the market is baking in success for its products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

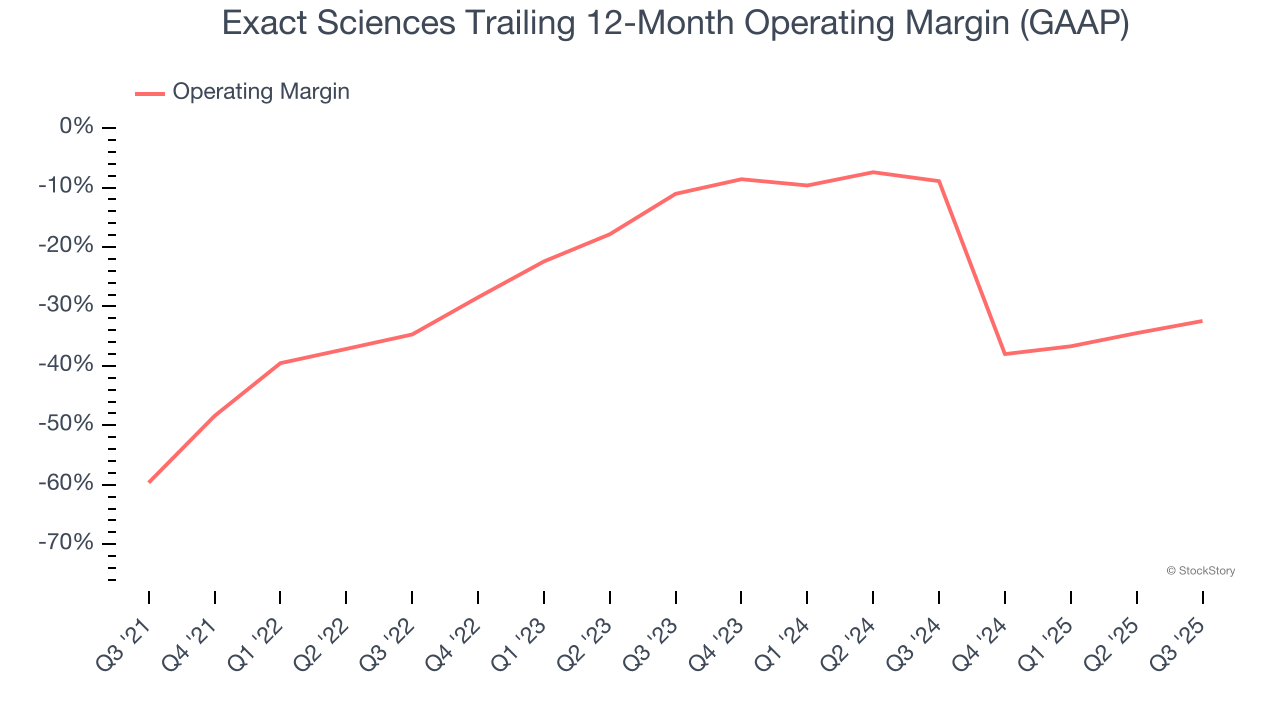

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Exact Sciences’s high expenses have contributed to an average operating margin of negative 27.2% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, Exact Sciences’s operating margin rose by 27.2 percentage points over the last five years, as its sales growth gave it operating leverage. Zooming into its more recent performance, however, we can see the company’s margin has decreased by 21.4 percentage points on a two-year basis. If Exact Sciences wants to pass our bar, it must prove it can expand its profitability consistently.

Exact Sciences’s operating margin was negative 3% this quarter.

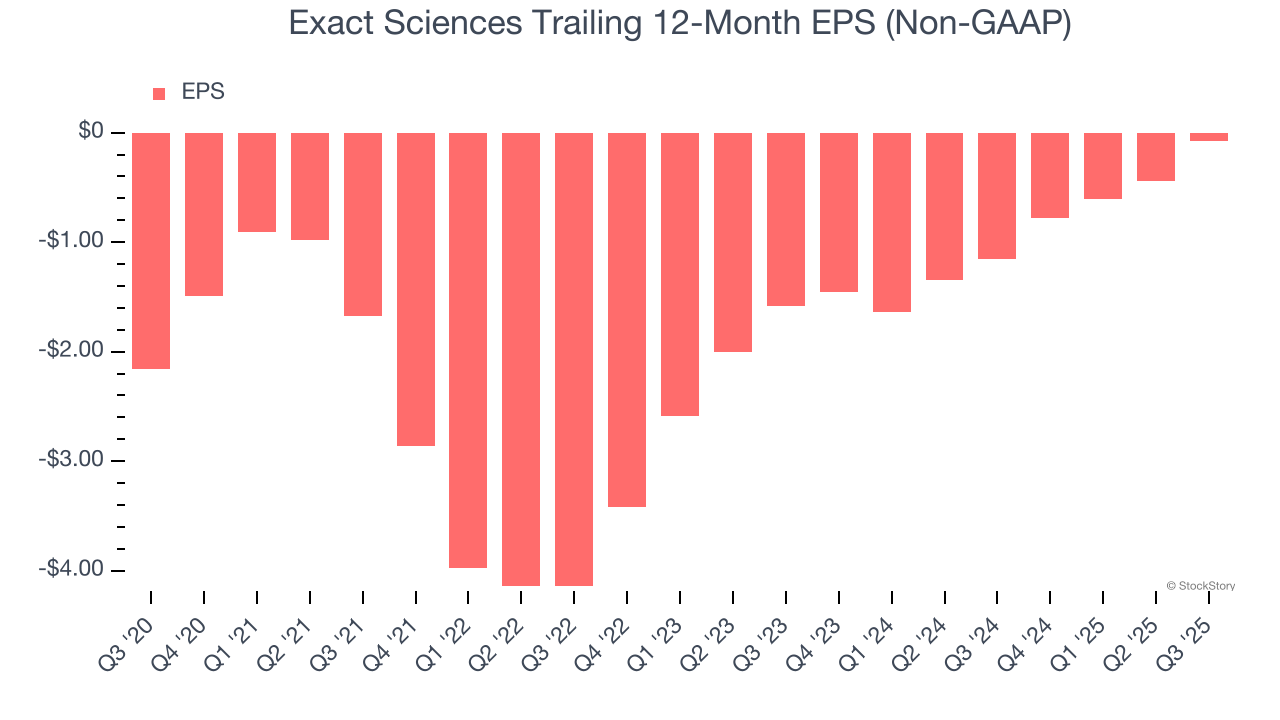

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Although Exact Sciences’s full-year earnings are still negative, it reduced its losses and improved its EPS by 48.5% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability.

In Q3, Exact Sciences reported adjusted EPS of $0.24, up from negative $0.13 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street is optimistic. Analysts forecast Exact Sciences’s full-year EPS of negative $0.08 will flip to positive $0.89.

It was good to see Exact Sciences beat analysts’ revenue and EPS expectations convincingly this quarter. Full-year revenue guidance was raised, and full-year EBITDA guidance came in ahead of expectations. Zooming out, we think this quarter featured some important positives. The stock traded up 6.9% to $71.65 immediately following the results.

Exact Sciences had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 | |

| Feb-09 | |

| Feb-08 | |

| Feb-06 | |

| Feb-03 | |

| Feb-03 | |

| Feb-03 | |

| Feb-02 | |

| Jan-28 | |

| Jan-27 | |

| Jan-27 | |

| Jan-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite