|

|

|

|

|||||

|

|

|

Monster Beverage Corporation MNST is set to report third-quarter 2025 results on Nov. 6, after the closing bell. The beverage company is anticipated to have witnessed revenue and earnings growth.

The Zacks Consensus Estimate for revenues is pegged at $2.11 billion, indicating growth of 12.1% from the figure reported in the year-ago quarter. The consensus estimate for earnings of 48 cents per share implies a rise of 20% from the year-ago quarter’s actual. The consensus mark has been stable in the past 30 days.

Monster Beverage Corporation price-consensus-eps-surprise-chart | Monster Beverage Corporation Quote

In the last reported quarter, the company registered a positive earnings surprise of 8.3%. It has delivered an average positive earnings surprise of 0.19% in the trailing four quarters.

Monster Beverage’s quarterly performance is likely to have benefited from continued strength in global demand for energy drinks, with double-digit category growth across major regions such as North America, EMEA and Asia-Pacific. The company’s diverse portfolio, spanning flagship Monster Energy, the expanding Ultra family and affordable strategic brands, positions it well to capture rising household penetration and evolving consumer preferences for functional beverages. Continued category momentum, especially in Zero Sugar and flavored variants, is expected to remain a central growth catalyst into the to-be-reported quarter.

Innovation remains a cornerstone for Monster Beverage’s growth strategy. The upcoming launches of new flavors such as Monster Energy Electric Blue, Orange Dreamsicle and Ultra Wild Passion, along with the U.S. debut of Monster Energy Lando Norris Zero Sugar, are expected to sustain consumer engagement and retail excitement. The company’s refreshed branding for the Ultra line, coupled with expanded merchandising visibility and social media virality, is likely to further drive velocity in stores. These innovation efforts not only broaden the consumer base but also strengthen Monster Beverage’s premium image in an increasingly competitive beverage landscape.

Pricing actions and cost management are anticipated to play a significant role in shaping profitability in the quarter to be reported. Monster Beverage has indicated selective price adjustments in the United States during the fourth quarter of 2025, along with reductions in promotional allowances. These moves are designed to offset modest tariff-related pressures and maintain strong gross margins. The company’s ongoing supply chain optimization and strategic hedging against aluminum price volatility are expected to help stabilize input costs and protect margins despite a complex trade environment.

International expansion remains a key growth lever. With net sales outside the United States now representing 41% of total revenues, Monster Beverage’s geographic diversification continues to strengthen. Strong performance in EMEA, led by double-digit gains and growing market share, alongside accelerating sales in Asia-Pacific, particularly in China, India and South Korea, underscores the company’s global traction. Affordable energy brands like Predator and Fury are fueling emerging market growth, while Monster Beverage’s collaboration with Coca-Cola bottlers enhances distribution efficiency. Together, these factors set the stage for sustained earnings growth and continued outperformance in the energy drink category in the to-be-reported quarter.

On the flip side, MNST has been grappling with high operating expenses due to higher costs associated with sponsorships, endorsements and payroll. These rising expenses have been further compounded by increased stock-based compensation tied to new equity awards and ongoing litigation provisions. While these investments support brand visibility and talent retention, they have also placed upward pressure on general and administrative costs, signaling the need for tighter expense management to preserve margins in the coming quarter.

Our proven model does not conclusively predict an earnings beat for Monster Beverage this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. But that’s not the case here.

Monster Beverage currently has an Earnings ESP of -2.30% and a Zacks Rank of 3. You can uncover the best stocks before they’re reported with our Earnings ESP Filter.

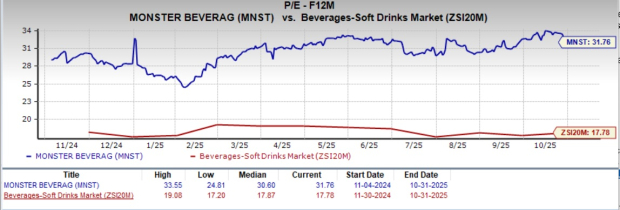

From a valuation perspective, Monster Beverage stock is trading at a premium relative to the industry benchmarks. With a forward 12-month price-to-earnings ratio of 31.38x, the stock is trading above the Beverages - Soft Drinks industry’s average of 17.78x.

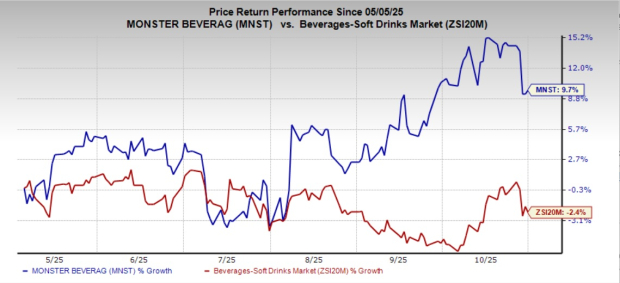

The recent market movements show that MNST’s shares have gained 9.7% in the past six months against the industry's 2.4% decline.

Here are some companies, which, according to our model, have the right combination of elements to beat on earnings this reporting cycle.

Ollie's Bargain Outlet Holdings, Inc. OLLI currently has an Earnings ESP of +6.54% and a Zacks Rank of 2. The Zacks Consensus Estimate for third-quarter fiscal 2025 EPS is pegged at 71 cents, which implies a 22.4% decrease year over year. You can see the complete list of today’s Zacks #1 Rank stocks here.

The consensus mark for Ollie's Bargain’s quarterly revenues is pegged at $615.7 million, which indicates growth of 18.9% from the figure reported in the prior-year quarter. OLLI delivered a trailing four-quarter earnings surprise of 4.2%, on average.

Vital Farms VITL currently has an Earnings ESP of +2.65% and a Zacks Rank of 2. VITL is anticipated to register increases in its top and bottom lines when it reports third-quarter 2025 results. The Zacks Consensus Estimate for Vital Farms’ quarterly revenues is pegged at $191 million, indicating growth of 32.2% from the figure reported in the prior-year quarter.

The consensus estimate for Vital Farms’ bottom line has increased by a penny in the past seven days to 30 cents per share. This implies a surge of 87.5% from the year-ago quarter’s reported figure. VITL delivered an earnings beat of 35.8%, on average, in the trailing four quarters.

The Campbell's Company CPB has an Earnings ESP of +1.49% and a Zacks Rank of 3 at present. CPB is likely to register top and bottom-line declines when it releases first-quarter fiscal 2026 results. The Zacks Consensus Estimate for its quarterly revenues is pegged at $2.7 billion, which implies a dip of 3.7% from the figure in the prior-year quarter.

The consensus estimate for Campbell's bottom line has been unchanged at 74 cents per share in the past 30 days. The estimate indicates a 16.9% decline from the year-ago quarter’s actual. CPB delivered an earnings surprise of 6.2%, in the trailing four quarters.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 5 hours | |

| Jul-25 | |

| Jul-23 | |

| Jul-22 | |

| Jul-20 |

Monster Stock Creates Add-On Entry After Powerful Earnings-Fueled Breakout

MNST

Investor's Business Daily

|

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-17 | |

| Jul-14 | |

| Jul-14 | |

| Jul-13 | |

| Jul-08 | |

| Jul-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite