|

|

|

|

|||||

|

|

|

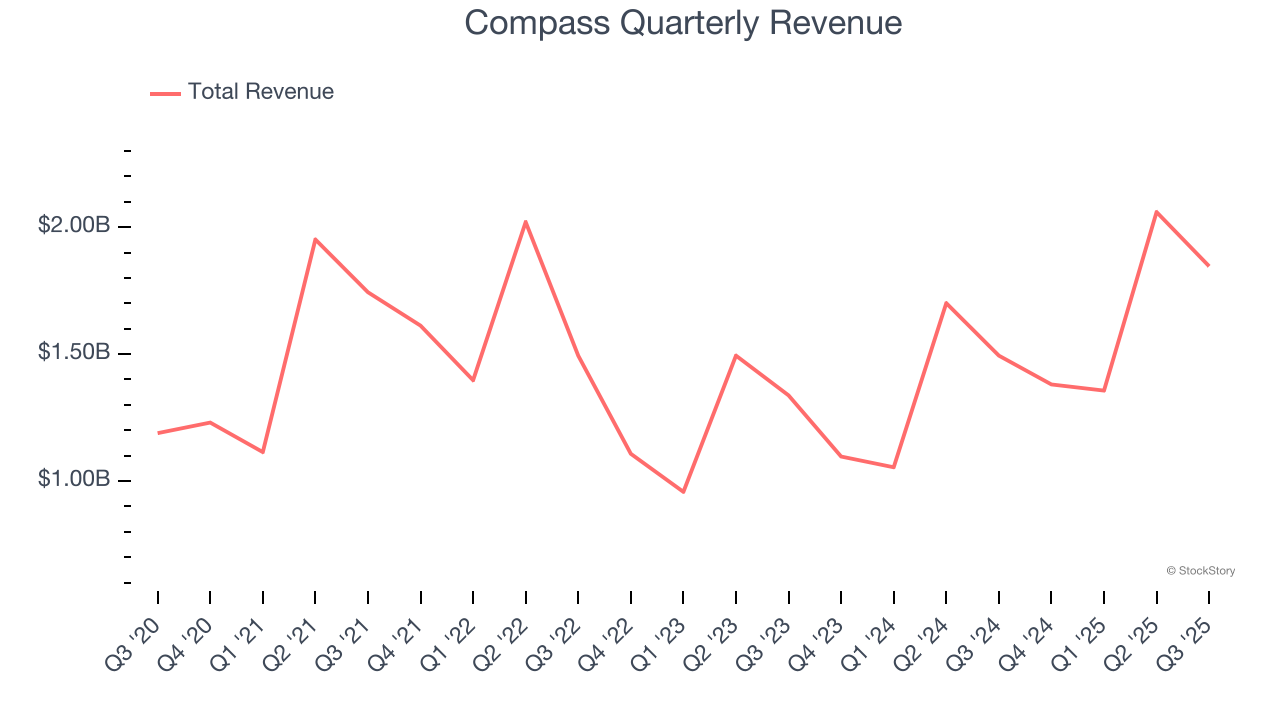

Real estate technology company Compass (NYSE:COMP) reported Q3 CY2025 results topping the market’s revenue expectations, with sales up 23.6% year on year to $1.85 billion. The company expects next quarter’s revenue to be around $1.64 billion, close to analysts’ estimates. Its GAAP loss of $0.01 per share was $0.01 above analysts’ consensus estimates.

Is now the time to buy Compass? Find out by accessing our full research report, it’s free for active Edge members.

Fueled by its mission to replace the "paper-driven, antiquated workflow" of buying a house, Compass (NYSE:COMP) is a digital-first company operating a residential real estate brokerage in the United States.

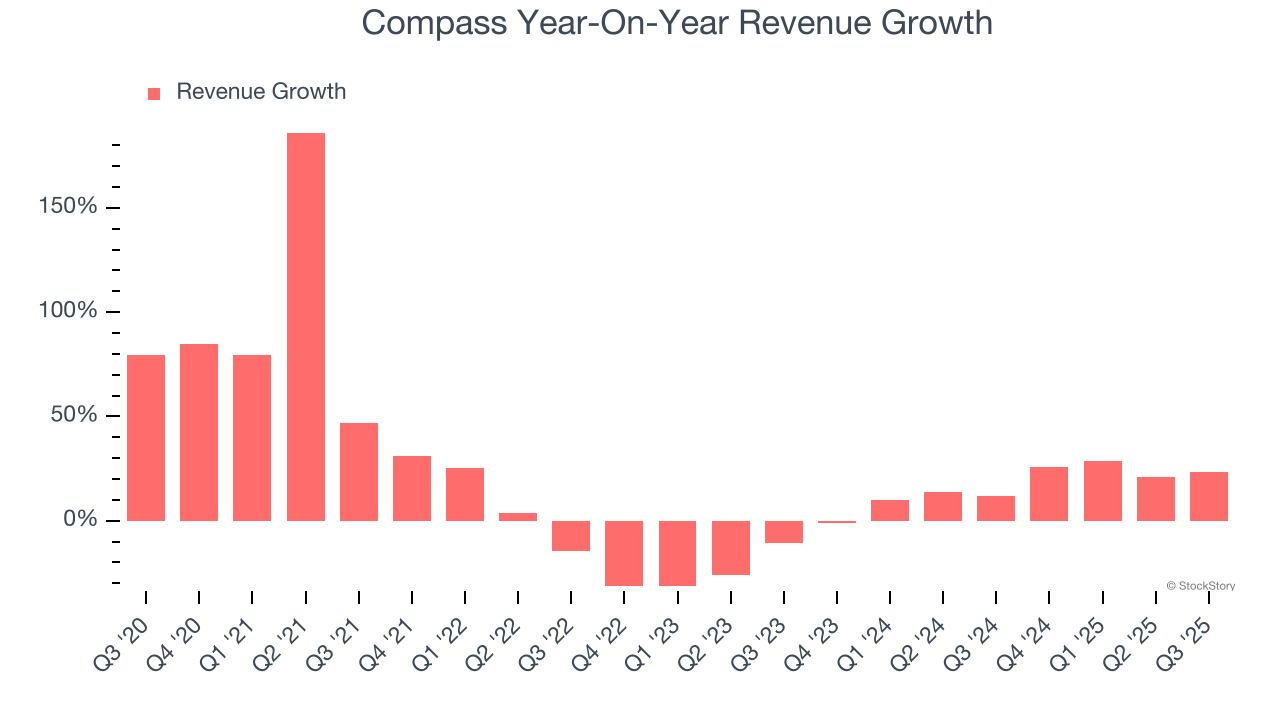

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Compass’s 16% annualized revenue growth over the last five years was decent. Its growth was slightly above the average consumer discretionary company and shows its offerings resonate with customers.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Compass’s annualized revenue growth of 16.5% over the last two years aligns with its five-year trend, suggesting its demand was stable.

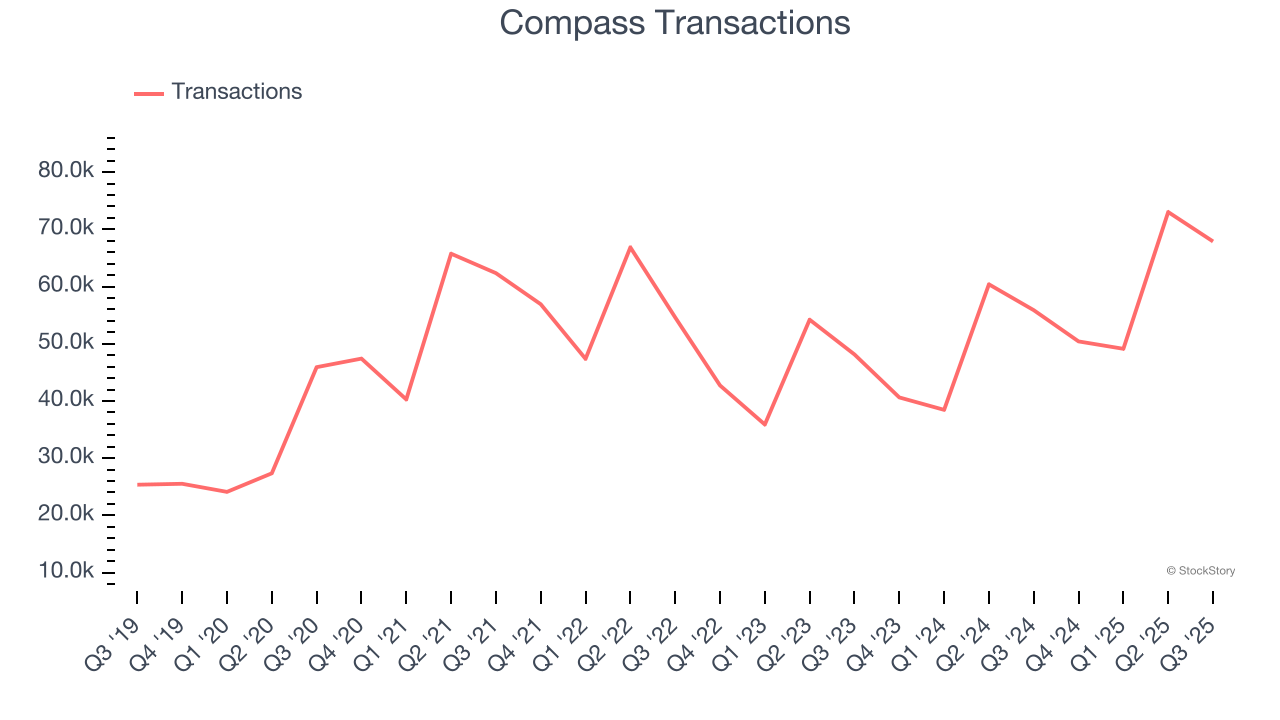

Compass also discloses its number of transactions, which reached 67,886 in the latest quarter. Over the last two years, Compass’s transactions averaged 15.5% year-on-year growth. Because this number aligns with its revenue growth during the same period, we can see the company’s monetization was fairly consistent.

This quarter, Compass reported robust year-on-year revenue growth of 23.6%, and its $1.85 billion of revenue topped Wall Street estimates by 3.2%. Company management is currently guiding for a 18.8% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 13.7% over the next 12 months, a slight deceleration versus the last two years. Still, this projection is above the sector average and implies the market sees some success for its newer products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

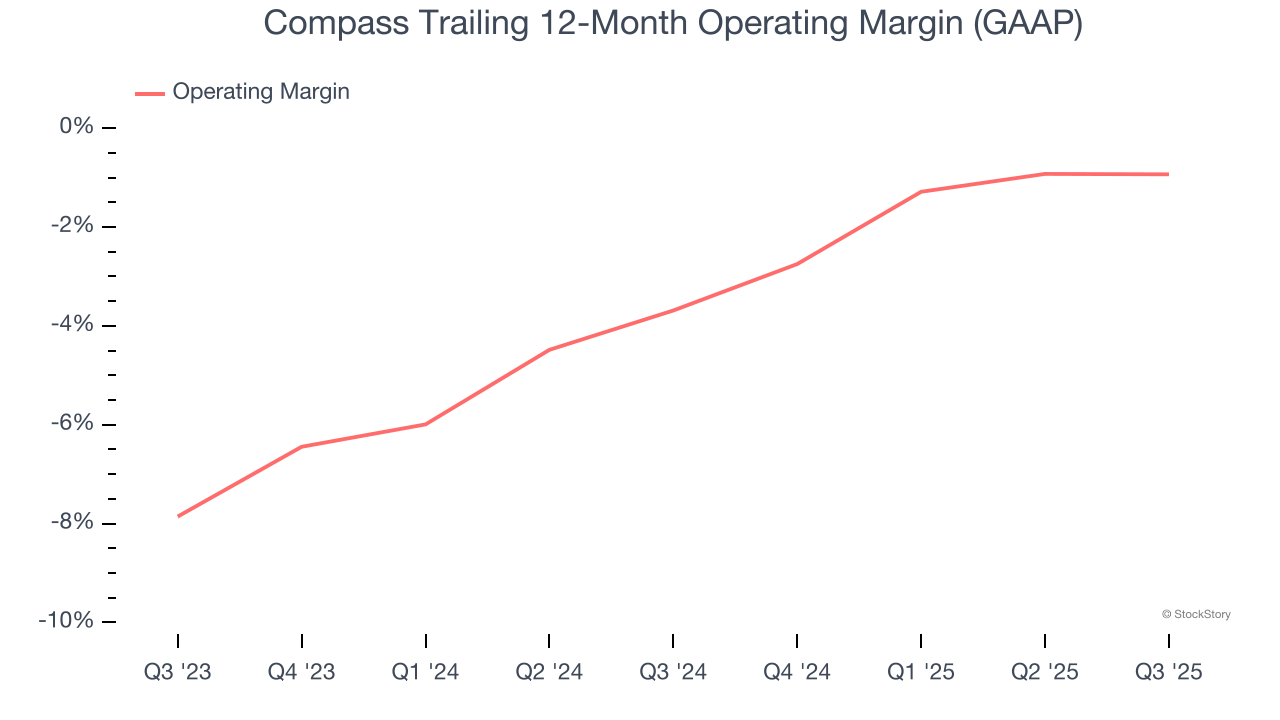

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Compass’s operating margin has been trending up over the last 12 months, but it still averaged negative 2.2% over the last two years. This is due to its large expense base and inefficient cost structure.

Compass’s operating margin was negative 0.4% this quarter.

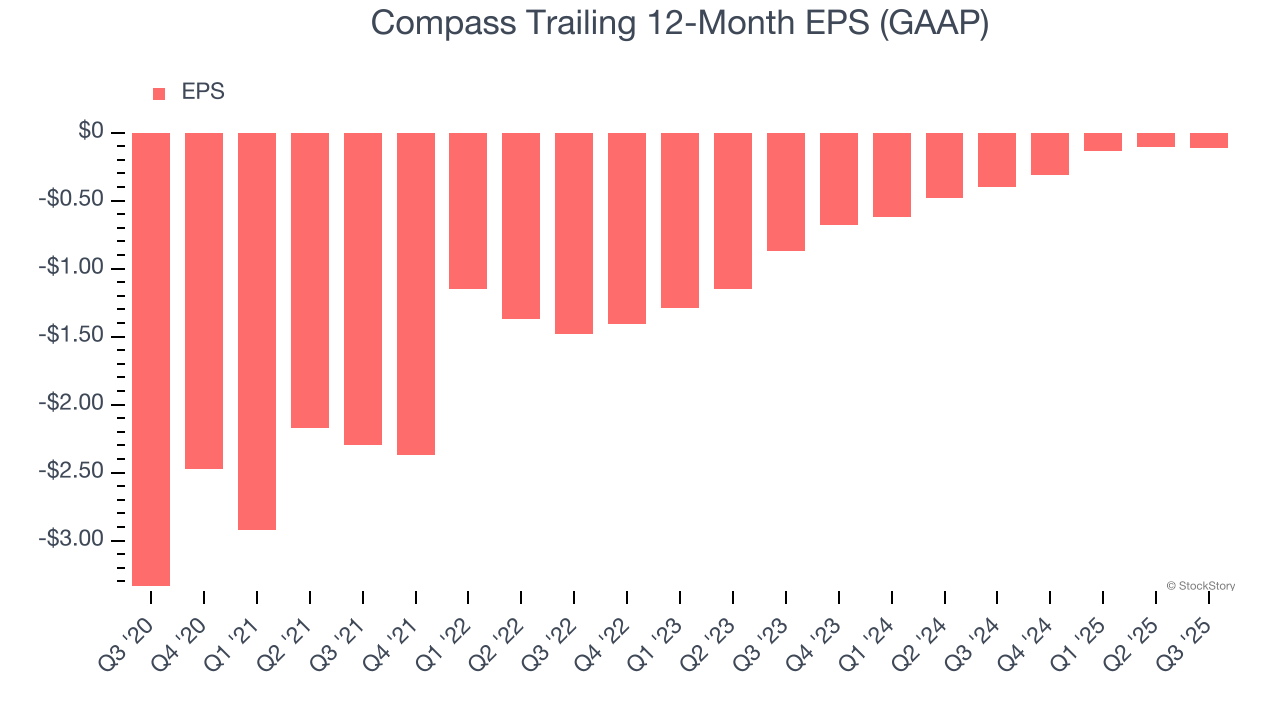

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although Compass’s full-year earnings are still negative, it reduced its losses and improved its EPS by 49.5% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability.

In Q3, Compass reported EPS of negative $0.01, in line with the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street is optimistic. Analysts forecast Compass’s full-year EPS of negative $0.11 will flip to positive $0.10.

We were impressed by Compass’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 1.5% to $7.90 immediately after reporting.

Sure, Compass had a solid quarter, but if we look at the bigger picture, is this stock a buy? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| 14 hours | |

| Mar-08 | |

| Mar-06 | |

| Mar-06 | |

| Mar-05 | |

| Mar-04 | |

| Mar-04 | |

| Mar-02 | |

| Feb-28 | |

| Feb-28 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite