|

|

|

|

|||||

|

|

|

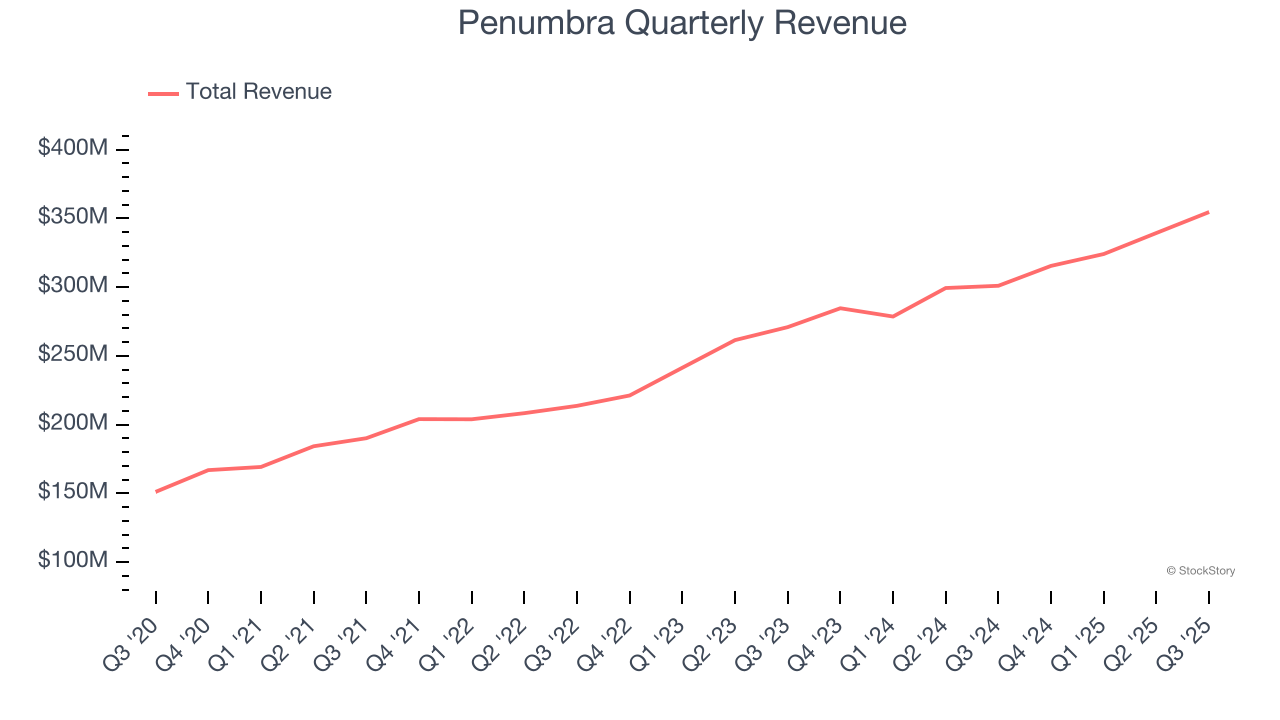

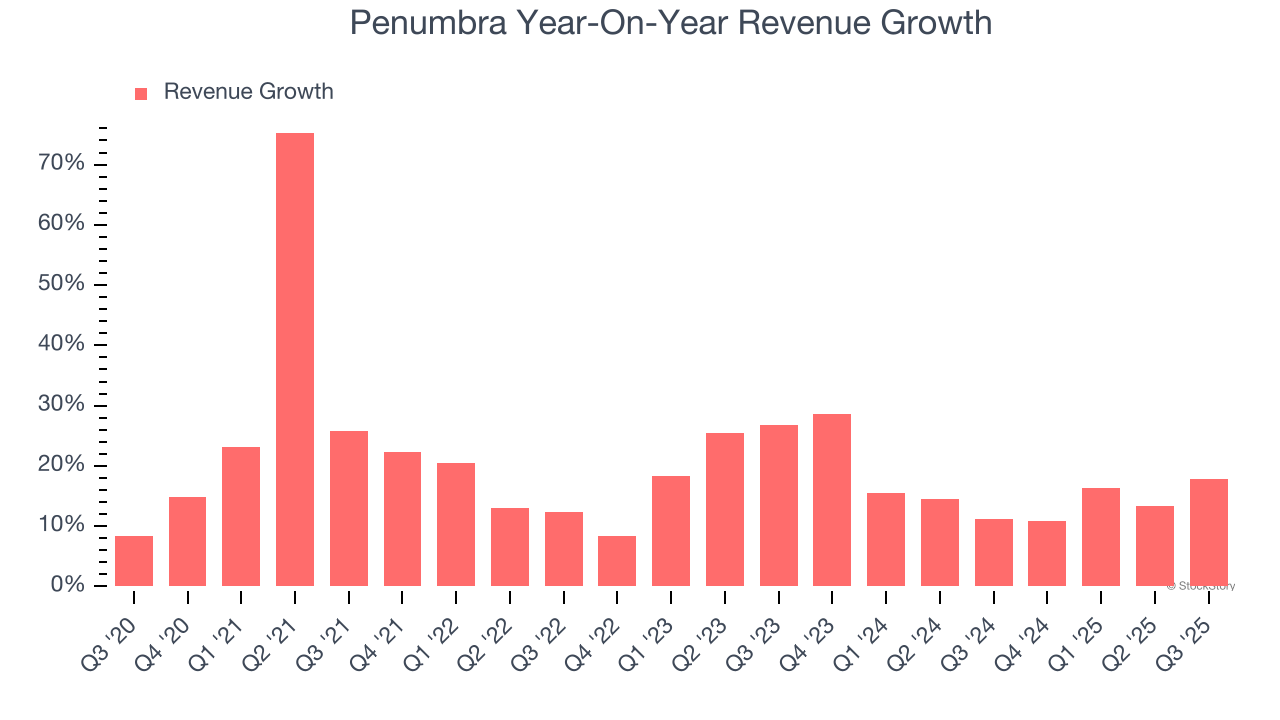

Medical device company Penumbra (NYSE:PEN) reported Q3 CY2025 results exceeding the market’s revenue expectations, with sales up 17.8% year on year to $354.7 million. Its non-GAAP profit of $0.97 per share was 5.3% above analysts’ consensus estimates.

Is now the time to buy Penumbra? Find out by accessing our full research report, it’s free for active Edge members.

Founded in 2004 to address challenging medical conditions with significant unmet needs, Penumbra (NYSE:PEN) develops and manufactures innovative medical devices for treating vascular diseases and providing immersive healthcare rehabilitation solutions.

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Luckily, Penumbra’s sales grew at an impressive 19.9% compounded annual growth rate over the last five years. Its growth beat the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Penumbra’s annualized revenue growth of 15.8% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

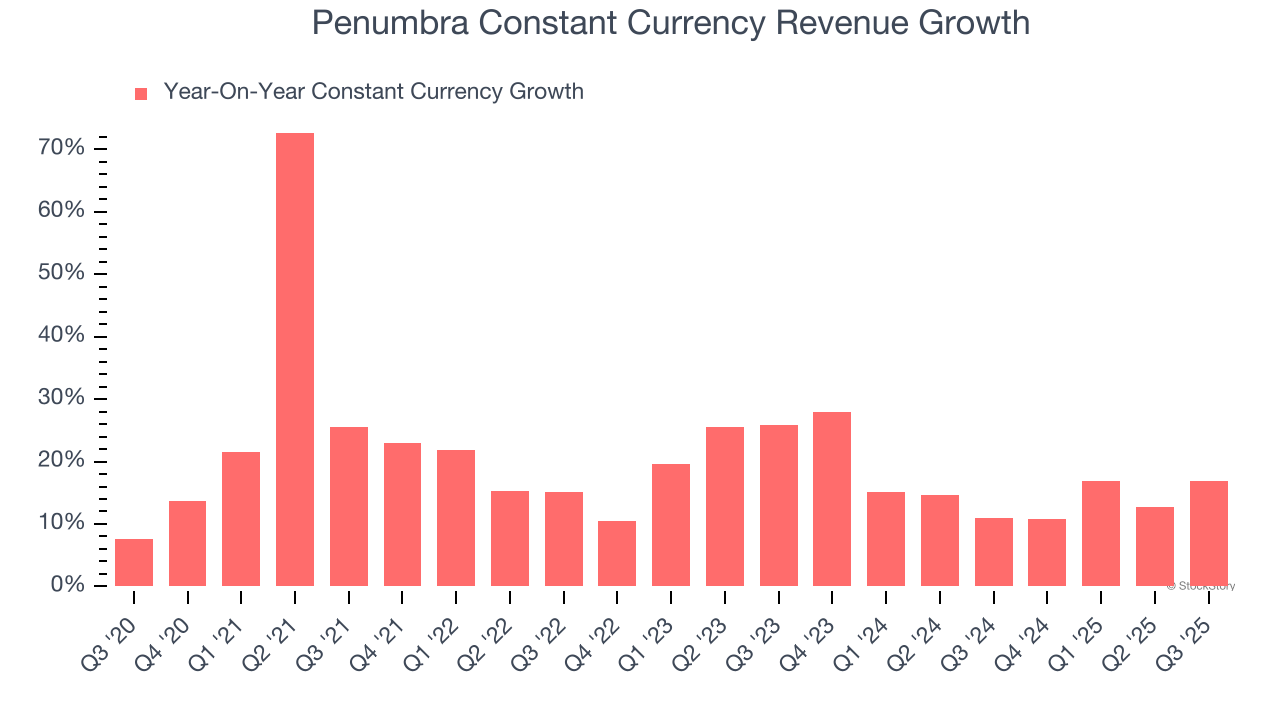

We can dig further into the company’s sales dynamics by analyzing its constant currency revenue, which excludes currency movements that are outside their control and not indicative of demand. Over the last two years, its constant currency sales averaged 15.7% year-on-year growth. Because this number aligns with its normal revenue growth, we can see that Penumbra has properly hedged its foreign currency exposure.

This quarter, Penumbra reported year-on-year revenue growth of 17.8%, and its $354.7 million of revenue exceeded Wall Street’s estimates by 4.2%.

Looking ahead, sell-side analysts expect revenue to grow 12.8% over the next 12 months, a deceleration versus the last two years. Still, this projection is noteworthy and indicates the market sees success for its products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

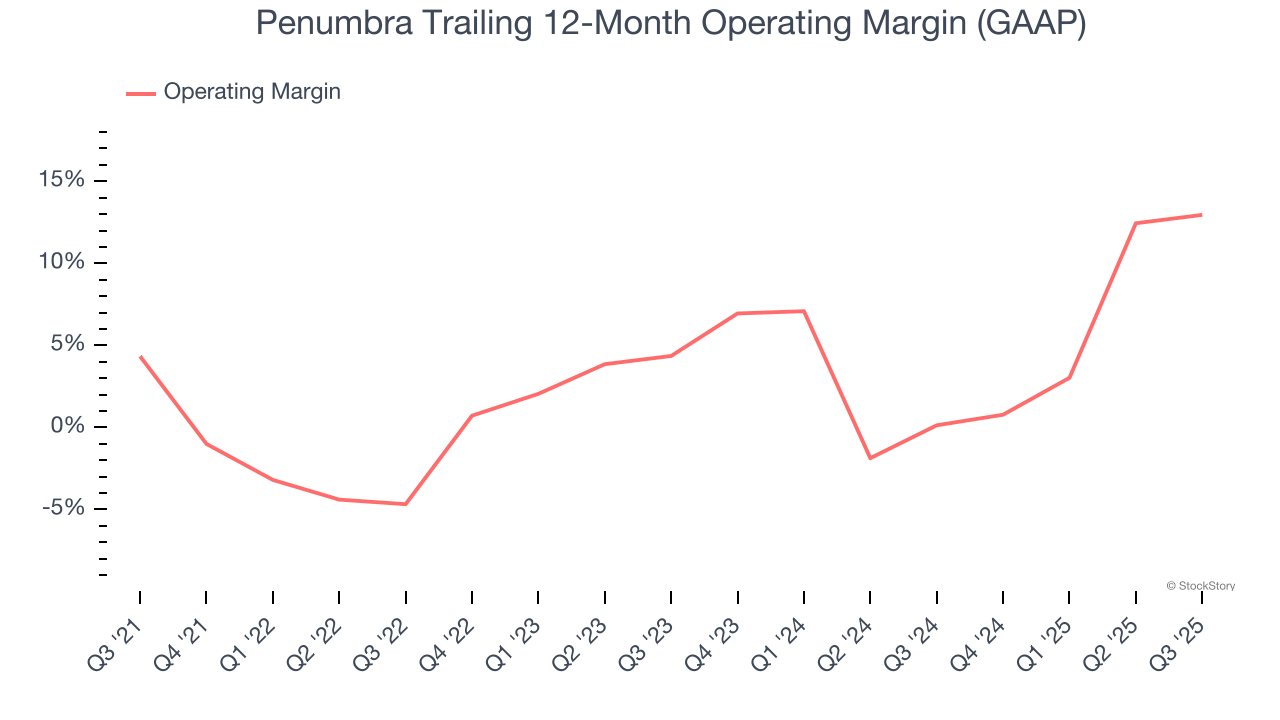

Penumbra was profitable over the last five years but held back by its large cost base. Its average operating margin of 4.2% was weak for a healthcare business.

On the plus side, Penumbra’s operating margin rose by 8.6 percentage points over the last five years, as its sales growth gave it operating leverage. The company’s two-year trajectory shows its performance was mostly driven by its recent improvements.

This quarter, Penumbra generated an operating margin profit margin of 13.8%, up 2 percentage points year on year. This increase was a welcome development and shows it was more efficient.

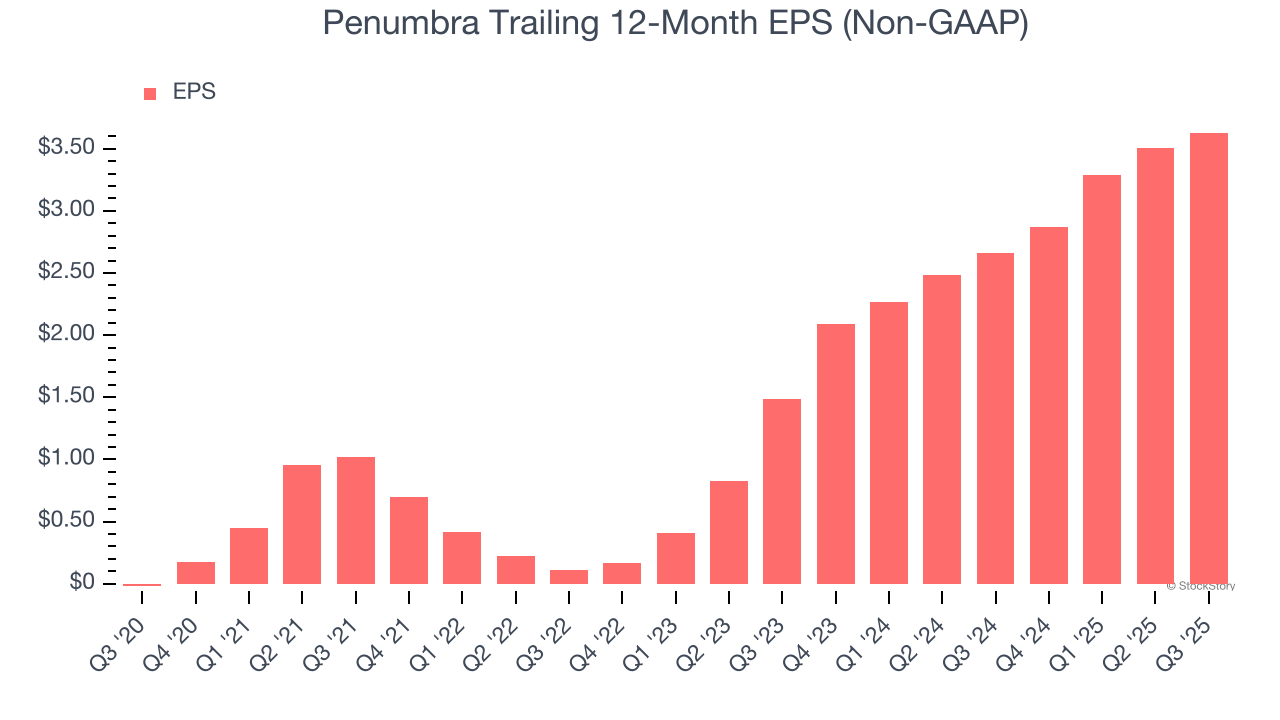

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Penumbra’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q3, Penumbra reported adjusted EPS of $0.97, up from $0.85 in the same quarter last year. This print beat analysts’ estimates by 5.3%. Over the next 12 months, Wall Street expects Penumbra’s full-year EPS of $3.63 to grow 27.9%.

We were impressed by how significantly Penumbra blew past analysts’ constant currency revenue expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The stock traded up 18.7% to $268 immediately after reporting.

Sure, Penumbra had a solid quarter, but if we look at the bigger picture, is this stock a buy? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Jul-07 | |

| Jun-18 | |

| Jun-17 | |

| Jun-16 |

Penumbras Thunderbolt approval poised to accelerate neuro thrombectomy innovation

PEN

Medical Device Network

|

| Jun-15 | |

| Jun-12 | |

| Jun-12 | |

| Jun-11 | |

| May-06 | |

| May-06 | |

| Apr-20 | |

| Apr-13 | |

| Apr-10 | |

| Apr-09 | |

| Mar-31 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite