|

|

|

|

|||||

|

|

|

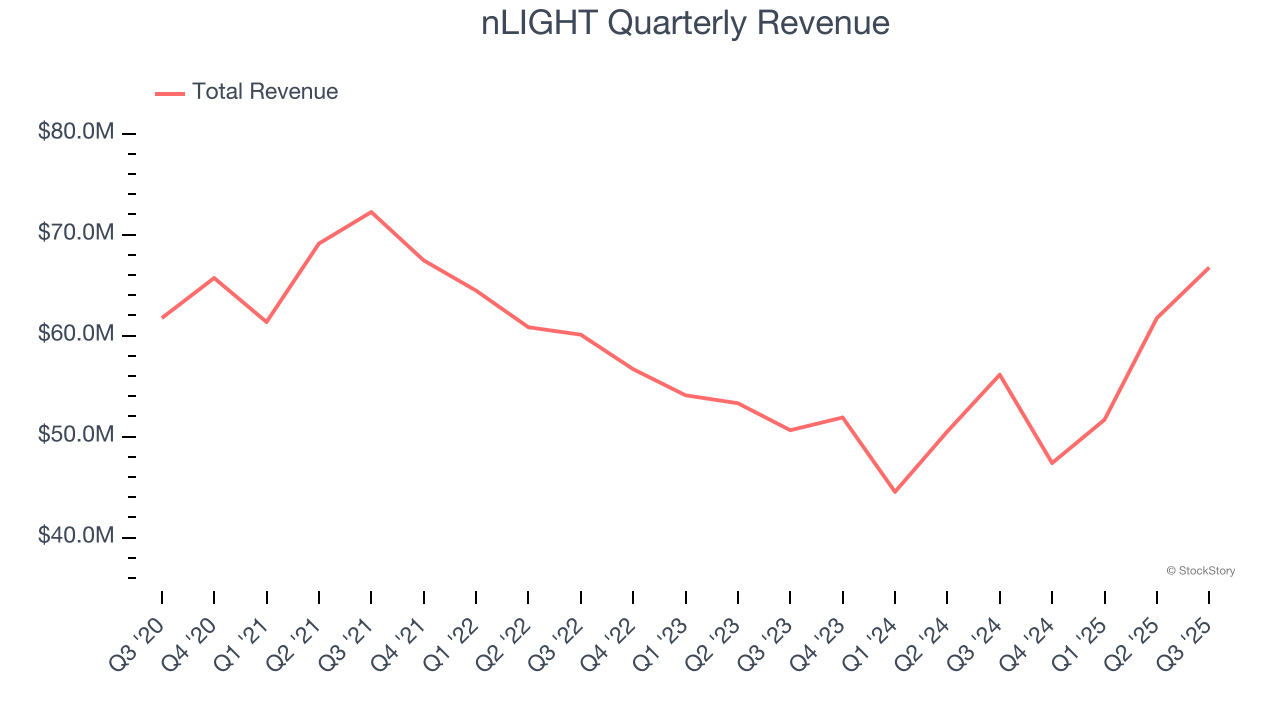

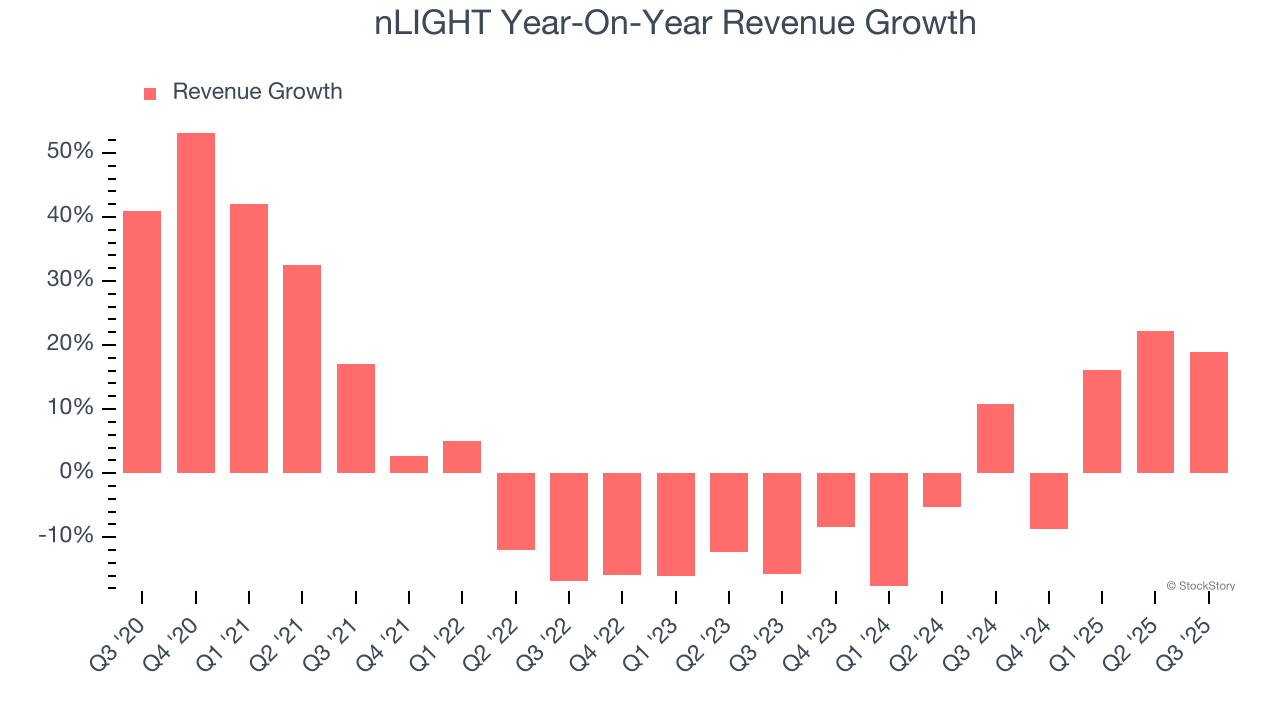

Laser company nLIGHT (NASDAQ:LASR) reported Q3 CY2025 results beating Wall Street’s revenue expectations, with sales up 18.9% year on year to $66.74 million. On top of that, next quarter’s revenue guidance ($75 million at the midpoint) was surprisingly good and 22.8% above what analysts were expecting. Its non-GAAP profit of $0.08 per share was significantly above analysts’ consensus estimates.

Is now the time to buy nLIGHT? Find out by accessing our full research report, it’s free for active Edge members.

“3Q 2025 represented another solid quarter of execution for nLIGHT with record revenue from our A&D markets driving our results,” commented Scott Keeney, nLIGHT’s President and Chief Executive Officer.

Founded by a former CEO and Harvard-educated entrepreneur Scott Keeneyn, nLIGHT (NASDAQ:LASR) offers semiconductor and fiber lasers to the industrial, aerospace & defense, and medical sectors.

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, nLIGHT’s sales grew at a sluggish 2.6% compounded annual growth rate over the last five years. This was below our standards and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. nLIGHT’s annualized revenue growth of 2.9% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

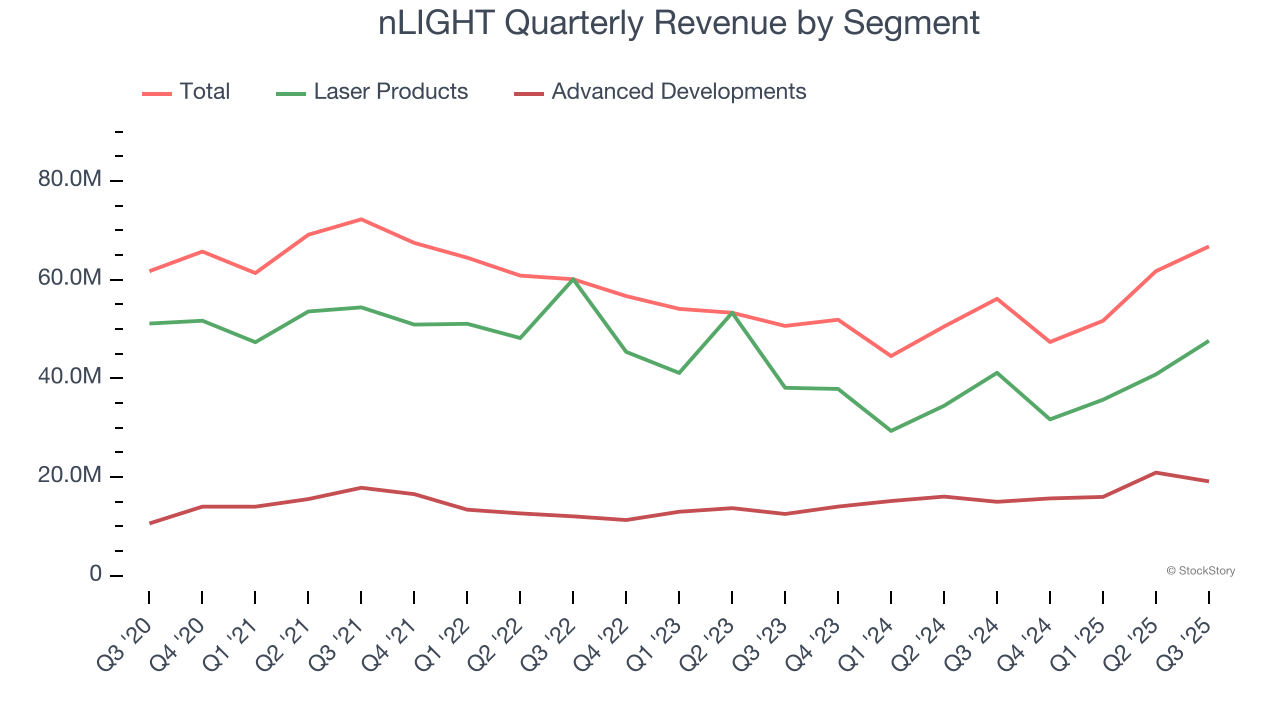

We can better understand the company’s revenue dynamics by analyzing its most important segments, Laser Products and Advanced Developments, which are 71.3% and 28.7% of revenue. Over the last two years, nLIGHT’s Laser Products revenue (lasers, amplifiers, and directed energy products) averaged 4.1% year-on-year declines. On the other hand, its Advanced Developments revenue (R&D contracts) averaged 19.1% growth.

This quarter, nLIGHT reported year-on-year revenue growth of 18.9%, and its $66.74 million of revenue exceeded Wall Street’s estimates by 5.4%. Company management is currently guiding for a 58.3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 9% over the next 12 months, an improvement versus the last two years. This projection is noteworthy and indicates its newer products and services will catalyze better top-line performance.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

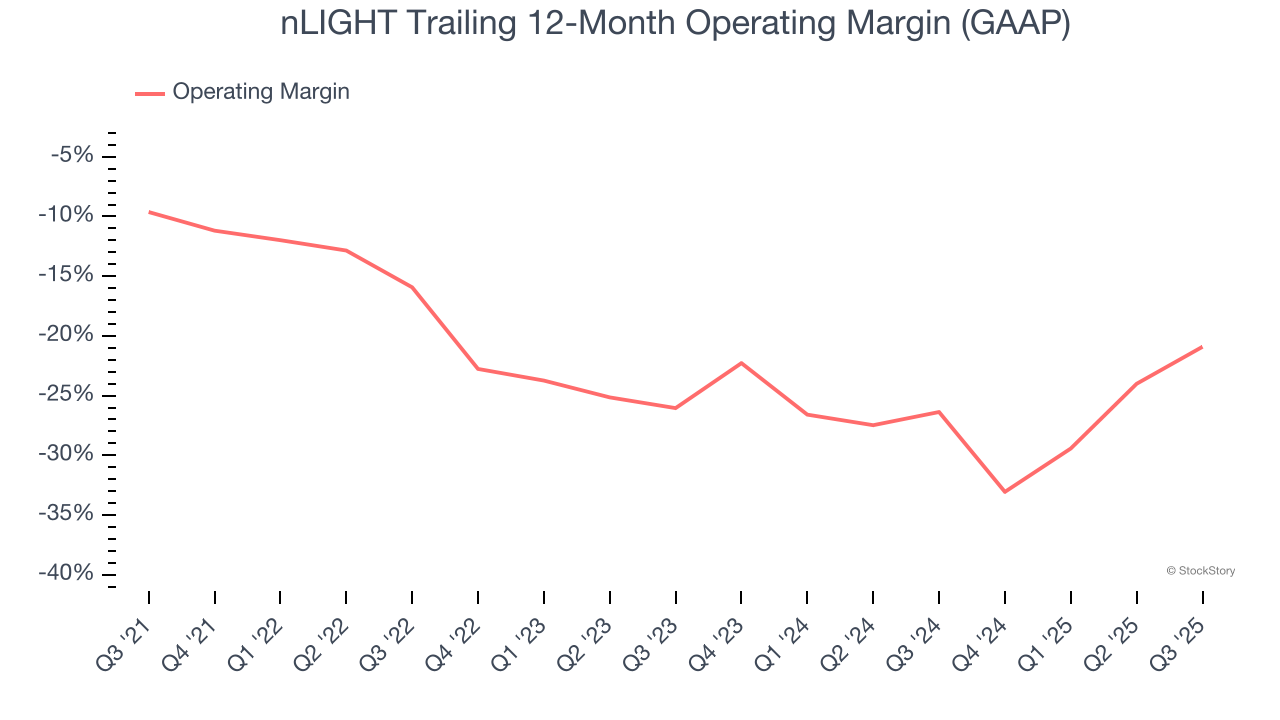

nLIGHT’s high expenses have contributed to an average operating margin of negative 19.1% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Looking at the trend in its profitability, nLIGHT’s operating margin decreased by 11.3 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. nLIGHT’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q3, nLIGHT generated a negative 10.9% operating margin. The company's consistent lack of profits raise a flag.

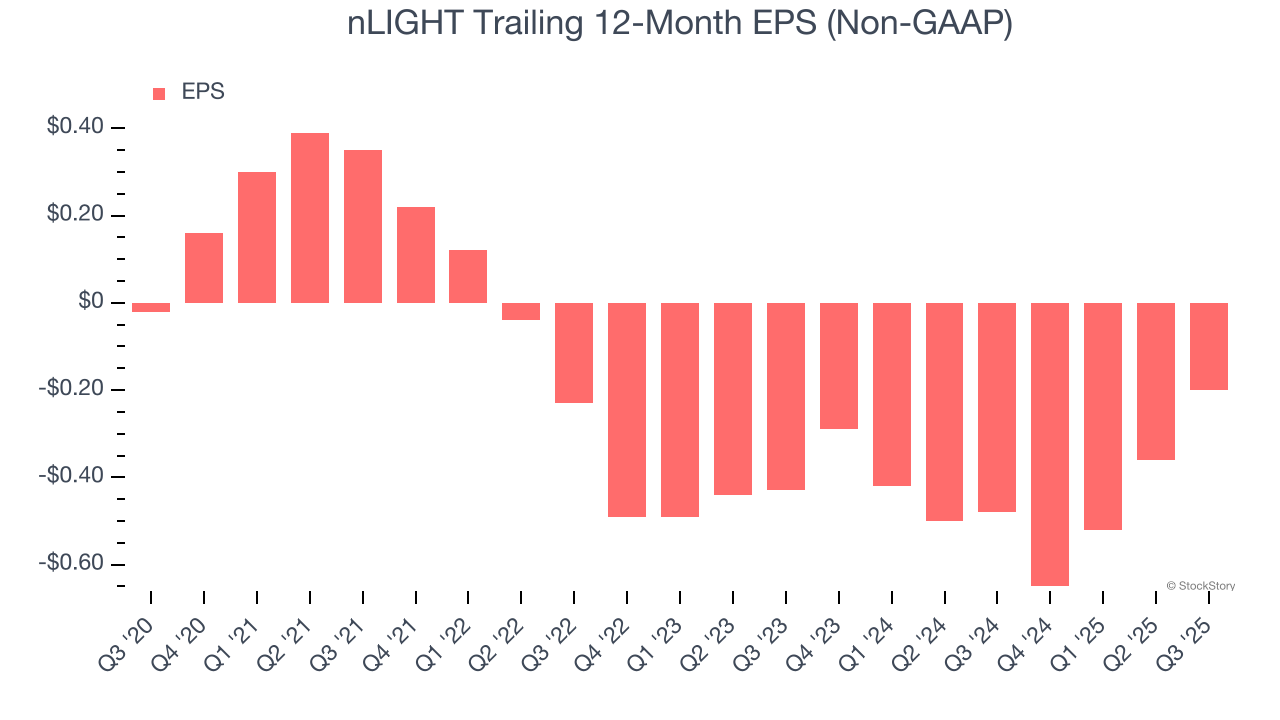

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

nLIGHT’s earnings losses deepened over the last five years as its EPS dropped 58.5% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, nLIGHT’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For nLIGHT, its two-year annual EPS growth of 31.8% was higher than its five-year trend. Its improving earnings is an encouraging data point, but a caveat is that its EPS is still in the red.

In Q3, nLIGHT reported adjusted EPS of $0.08, up from negative $0.08 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street is optimistic. Analysts forecast nLIGHT’s full-year EPS of negative $0.20 will flip to positive $0.02.

We were impressed by nLIGHT’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also glad its revenue and EPS both outperformed Wall Street’s estimates. Zooming out, we think this quarter featured a lot of important positives. The stock traded up 15.9% to $34.44 immediately after reporting.

nLIGHT may have had a good quarter, but does that mean you should invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Jul-10 | |

| Jul-10 | |

| Jul-09 | |

| Jul-09 | |

| Jun-08 | |

| May-15 | |

| May-13 | |

| May-12 | |

| May-11 | |

| May-07 | |

| May-07 | |

| May-07 | |

| May-07 | |

| May-06 | |

| Apr-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite