|

|

|

|

|||||

|

|

|

What a fantastic six months it’s been for Allegro MicroSystems. Shares of the company have skyrocketed 44.5%, hitting $27. This run-up might have investors contemplating their next move.

Is now the time to buy Allegro MicroSystems, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free for active Edge members.

We’re glad investors have benefited from the price increase, but we're cautious about Allegro MicroSystems. Here are three reasons we avoid ALGM and a stock we'd rather own.

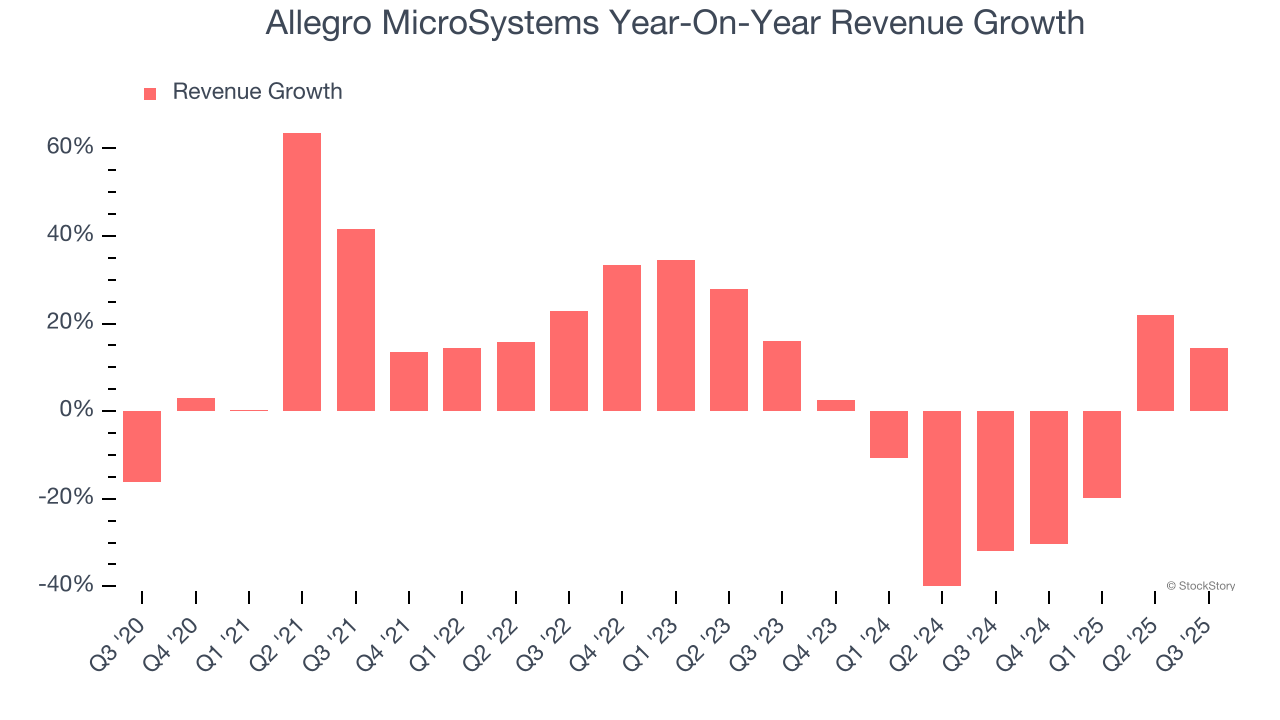

We at StockStory place the most emphasis on long-term growth, but within semiconductors, a stretched historical view may miss new demand cycles or industry trends like AI. Allegro MicroSystems’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 14.2% annually.

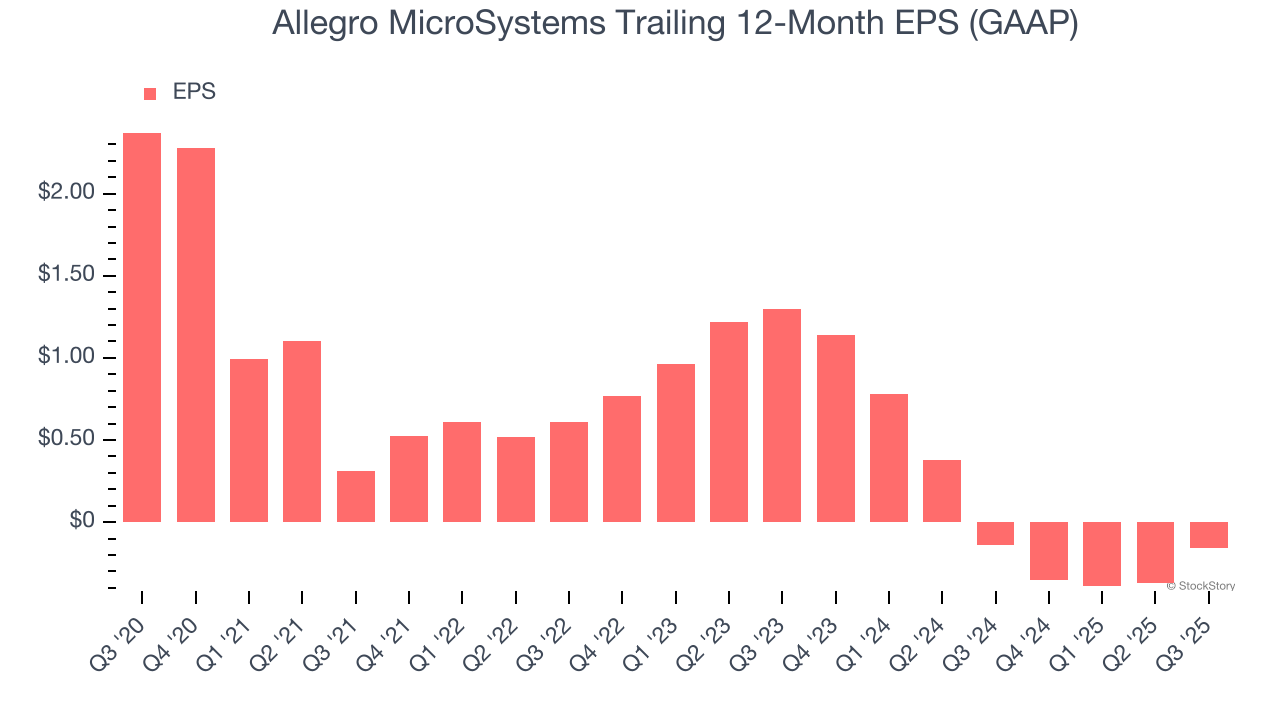

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Allegro MicroSystems, its EPS declined by 15.6% annually over the last five years while its revenue grew by 6.1%. This tells us the company became less profitable on a per-share basis as it expanded.

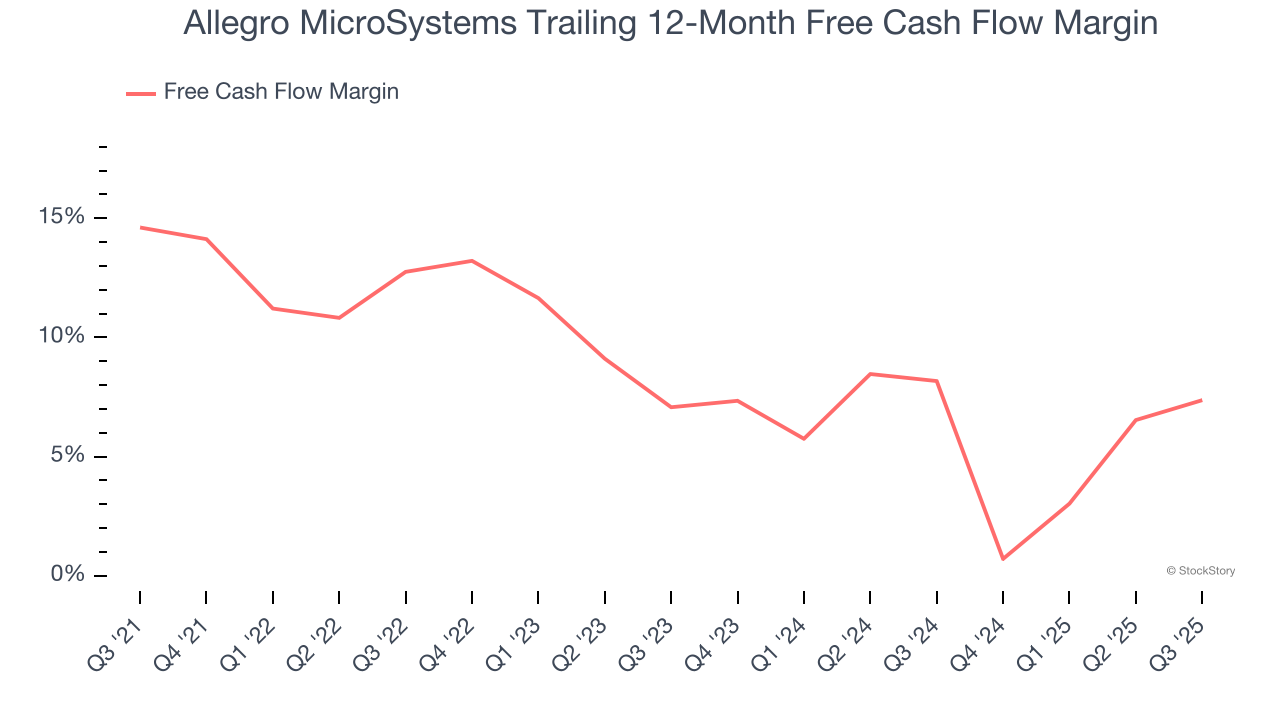

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Allegro MicroSystems has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 7.8%, lousy for a semiconductor business.

Allegro MicroSystems isn’t a terrible business, but it doesn’t pass our bar. After the recent rally, the stock trades at 36× forward P/E (or $27 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - you can find more timely opportunities elsewhere. We’d suggest looking at the most dominant software business in the world.

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Jul-30 | |

| Jul-30 | |

| Jul-20 | |

| Jul-16 | |

| Jul-13 | |

| Jul-09 | |

| Jul-02 | |

| Jul-02 | |

| Jul-01 | |

| Jun-29 |

Allegro MicroSystems Spikes To All-Time High On 'Best Idea' Rating

ALGM +14.65%

Investor's Business Daily

|

| Jun-18 | |

| May-13 | |

| May-13 | |

| May-07 | |

| May-07 |

Allegro MicroSystems Stock Dips Despite Beat-And-Raise Earnings Report

ALGM -6.70%

Investor's Business Daily

|

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite