|

|

|

|

|||||

|

|

|

Nebius Group N.V. NBIS will report third-quarter 2025 results on Nov. 11, before market open.

The Zacks Consensus Estimate for the bottom line for the to-be-reported quarter is pegged at a loss of 50 cents. The estimate has remained unchanged in the past 30 days. The consensus estimate for total revenues is pinned at $150.6 million.

Based in Amsterdam, Nebius is positioning itself as a specialized artificial intelligence (AI) infrastructure company. Its core operation is Nebius, which is an AI-powered cloud platform designed for intensive AI and machine learning (ML) workloads in both owned and colocation data center capacity. The company recently launched Nebius AI Cloud 3.0 “Aether,” a next-generation cloud platform designed for enterprise-scale AI. Nebius resumed trading as a public company in October 2024.

Our proven model does not conclusively predict an earnings beat for NBIS this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold) increases the chances of an earnings beat. But that is not the case here. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

NBIS has an Earnings ESP of 0.00% and a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank stocks here.

Soaring demand for AI cloud services amid the expansion of generative AI, ML and high-performance computing applications is likely to have driven its top-line performance in the to-be-reported quarter. Strong demand for copper GPUs and near-peak utilization are likely to have positively impacted third-quarter earnings. The company reported a ninefold surge in AI cloud revenue in the previous quarter. In September 2025, the company closed a deal with Microsoft for $17.4 billion, which involves NBIS providing dedicated GPU capacity to the latter from the new data center in Vineland, NJ, beginning later this year through 2031.

Additionally, the company’s upgraded cloud software to support large-scale clusters, expanding enterprise customer base with clients like Cloudflare, Prosus and Shopify, and its strengthened position as a preferred provider for AI-native startups are likely to have further supported revenue growth. On the last earnings call, management stated that it projects full-year ARR to be in the range of $900 million–$1.1 billion. Also, the company is focusing on building a global footprint, with capacity in the United States, Europe and the Middle East.

Nebius Group N.V. price-eps-surprise | Nebius Group N.V. Quote

However, the intense competition from behemoths remains a concern. Nebius is a relatively new entrant in the AI cloud infrastructure space, which boasts behemoths like Microsoft MSFT and Amazon AMZN and other upcoming players like CoreWeave CRWV.

Moreover, broader macroeconomic uncertainties and heavy capital spending remain challenges. NBIS projected that its 2025 capex would be $2 billion, which indicates a huge cash outlay even with a $4 billion capital raised as announced on the last earnings call. Later, NBIS announced the closing of its public offering of Class A ordinary shares and private offering of convertible senior notes, which have gross proceeds of nearly $4.2 billion as of Sept. 15, 2025. Elevated Capital expenditure levels pose a risk if revenue growth fails to keep pace with the company’s capital intensity, particularly in an environment where AI demand may fluctuate amid competitive pricing pressures and evolving regulatory frameworks.

Also, scaling aggressively (multiple data centers in various regions) involves execution risk. Moreover, Nebius’s reliance on equity stakes in Toloka, ClickHouse and Avride for funding is risky, as any drop in their valuations could weaken liquidity and disrupt its growth plans.

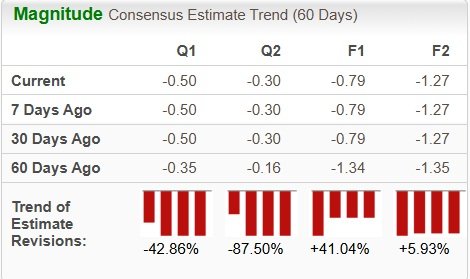

Analysts have significantly revised their earnings estimates downward for NBIS’ bottom line over the past 60 days.

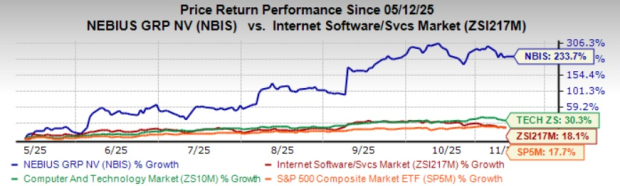

Nebius shares have risen 233.7% over the past six months, outperforming the Zacks Computer & Technology sector and the Zacks Internet Software Services industry’s growth of 30.3% and 18.1%, respectively. The S&P 500 Composite has returned 17.7% over the same time frame.

The gain is better than its peers, like Microsoft (up 10.6%), Amazon (up 17.1%) and CoreWeave, another hypergrowth pure play AI infrastructure company, which has registered a rally of 77.8% in the same period.

NBIS stock is also not so cheap, as its Value Style Score of F suggests a stretched valuation at this moment.

In terms of Price/Book, NBIS shares are trading at 6.95X, higher than the Internet Software Services industry’s ratio of 4.28, indicating more risk than opportunity.

In comparison, MSFT, AMZN and CRWV trade at multiples of 10.17X, 7.07X and 19.12X, respectively.

Intense competition and high capex pressure weigh on short-term prospects. While the company’s robust demand for AI cloud services and data center expansion augurs well, stretched valuation is concerning. Given these risks and limited near-term upside, investors could benefit from offloading NBIS ahead of the third-quarter results. Investors looking to invest should wait for a better entry point.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite