|

|

|

|

|||||

|

|

|

Supermicro operates on the pick-and-shovel side of the artificial intelligence market.

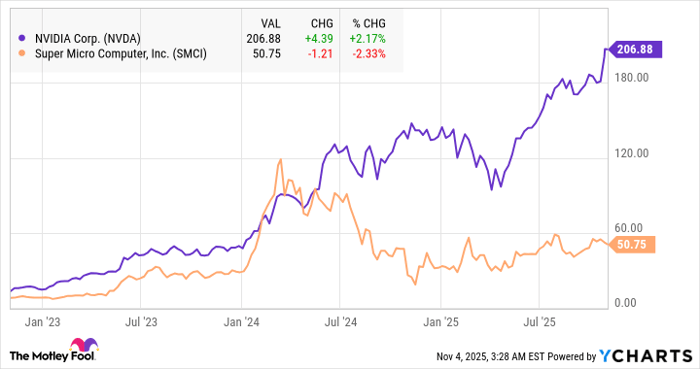

Its share price growth over the past three years has lagged behind AI industry leaders like Nvidia.

Super Micro Computer (NASDAQ: SMCI) was, for a time, a Wall Street darling. After the generative artificial intelligence (AI) trend began to gain ground in late 2022, demand for its computer servers and liquid cooling systems soared amid the scramble for AI hardware.

From just over $8 a share at the start of 2023, the red-hot stock peaked at roughly $119 per share in March 2024. But its boom was short-lived. It has since dropped by 57% from that peak to around $51 at the time of this writing as slowing top-line growth and a damning short-seller report have sapped investors' optimism about the tech company.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Despite the challenges, Supermicro is still an interesting way to get exposure to the pick-and-shovel side of the AI opportunity. Its stock price decline has also given it a discounted valuation compared to less controversial AI industry alternatives like Nvidia or TSMC. But what might the next five years have in store for the company?

If you compare the stock performances of Supermicro and Nvidia, you will notice that the stocks were moving generally in parallel in the early stages of the AI boom that OpenAI sparked with its release of ChatGPT. This is because they were both positioned at the core of AI infrastructure demand. Nvidia made the advanced graphics processing units (GPUs) needed to run and train large language models (LLMs), while Supermicro bundled these GPUs and other key hardware into user-ready computer servers.

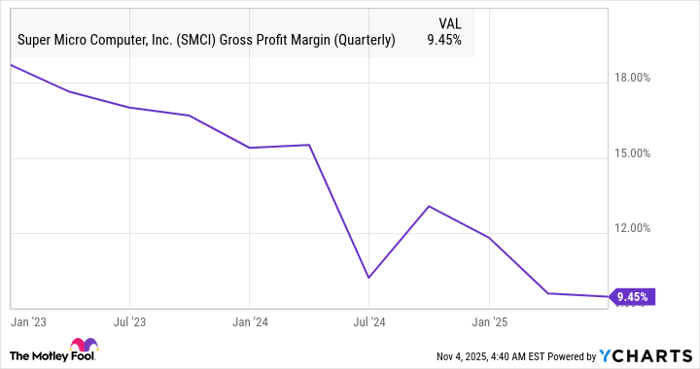

There are some key reasons why their performances eventually diverged. For starters, Nvidia has a much stronger economic moat because it actually designs and creates cutting-edge chips (with the help of its manufacturing partner, TSMC). This meant it enjoyed faster sales growth and higher margins. In its fiscal 2026 second quarter, the chipmaker boasted a software-like gross margin of 72.4%. Supermicro's was a comparatively measly 9.5% in its most recently reported quarter.

Supermicro has also been plagued by legal uncertainties following a short-seller report on Aug. 27, 2024, that accused it of accounting irregularities, self-dealing, and sanctions evasion related to the war between Russia and Ukraine. The crisis that followed that report led the company to delay some of its financial reports, and accounting giant Ernst & Young resigned as its auditor.

The good news for Supermicro is that in December 2024, an independent special committee found no evidence of wrongdoing at the company. It's also back in compliance with the Nasdaq's reporting and auditing requirements.

Image source: Getty Images.

In Supermicro's fiscal 2026 first quarter, which ended Sept. 30, its revenue dropped by 15% year over year to $5 billion, while net income dropped 60% to $168 million. The company is benefiting from industrywide tailwinds like the popularity of Nvidia's Blackwell GPUs and new opportunities like sovereign AI (in other words, nations building out government-owned data center infrastructure to support AI), but this hasn't been enough to reignite its growth to the levels it enjoyed in previous years.

Furthermore, the AI boom is getting long in the tooth. While large tech companies continue to spend billions on Nvidia's cutting-edge hardware, it is unclear how much longer this can last, particularly in light of the thus-far uninspiring returns on investment from all that spending -- or rather, the lack of them. AI-pure play OpenAI, for example, expects to burn through $115 billion by 2029. And according to a report from the Massachusetts Institute of Technology, a whopping 95% of corporate AI pilots fail to generate meaningful returns.

As an infrastructure provider, Supermicro is somewhat shielded from challenges to the consumer-facing side of the industry. It can keep making money as long as clients continue buying its hardware. That said, unlike Nvidia, Supermicro faces stiff competition because of its shallow moat. It isn't the only company that can install chips into servers. This helps explain its declining gross margins over the last few years.

SMCI Gross Profit Margin (Quarterly) data by YCharts.

Supermicro stock looks like a hold or a sell. With a forward price-to-earnings (P/E) multiple of just 20, the stock is cheaper than other AI infrastructure picks like Nvidia or TSMC, which trade at forward P/Es of 30 and 25, respectively. But given its lackluster growth and weak margins, there isn't much for long-term investors to get excited about. I expect that Supermicro shares will generally perform in line with the broader market over the next five years, but they could also underperform if demand for AI fails to meet expectations.

Before you buy stock in Super Micro Computer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Super Micro Computer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $595,194!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,153,334!*

Now, it’s worth noting Stock Advisor’s total average return is 1,036% — a market-crushing outperformance compared to 191% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of November 10, 2025

Will Ebiefung has positions in Super Micro Computer. The Motley Fool has positions in and recommends Nvidia and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-16 | |

| Jul-16 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-14 | |

| Jul-10 | |

| Jul-09 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite