|

|

|

|

|||||

|

|

|

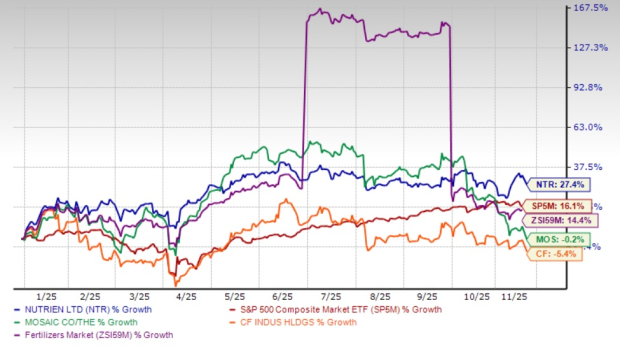

Nutrien Ltd.’s NTR shares have gained 27.4% year to date, outperforming the Zacks Fertilizers industry’s rise of 14.4% and the S&P 500’s increase of 16.1%. NTR is benefiting from healthy demand for crop nutrients, its actions to reduce costs and strategic acquisitions. Improving fertilizer prices are providing further support.

NTR’s peers, The Mosaic Company MOS and CF Industries Holdings, Inc. CF, have lost 0.2% and 5.4%, respectively, over the same period.

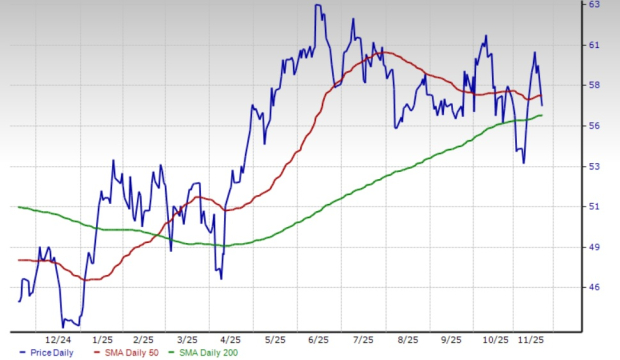

Technical indicators show that NTR is currently trading above its 200-day simple moving average (SMA). The stock slipped below its 50-day SMA yesterday. Following a golden crossover on Feb. 24, 2025, the 50-day SMA is reading higher than the 200-day SMA, indicating a bullish trend.

Let’s take a look at NTR’s fundamentals to better analyze how to play the stock.

Nutrien is well-placed to benefit from higher demand for fertilizers, backed by the strength in global agriculture markets. It is seeing healthy fertilizer demand in its major markets. Tight inventories are expected to support crop commodity prices in 2025. Strong demand and supply tightness have also led to an uptick in fertilizer prices this year.

Favorable farmer economics, improved affordability and low inventory levels are expected to drive potash demand globally. The phosphate market is also supported by low producer and channel inventories. Restricted exports from China have also led to supply tightness in this market. Demand for nitrogen fertilizer also remains healthy in major markets. Global nitrogen requirement is driven by demand in North America, India and Brazil. A resurgence in industrial nitrogen demand also bodes well.

The company expects record crop production prospects in the United States and sees strong demand for crop inputs. NTR saw record potash sales volumes in the first nine months of 2025, driven by favorable potash affordability and robust consumption in North America and major offshore markets. Third-quarter volumes also rose due to strong demand in North America and offshore. NTR has raised potash sales volume guidance for 2025 to 14-14.5 million tons, driven by anticipated higher global demand.

NTR should also gain from acquisitions and increased adoption of its digital platform. It continues to expand its footprint in Brazil through acquisitions. It is expected to continue pursuing targeted opportunities in its core markets. The company expects to utilize part of its free cash flow for incremental growth investments, including tuck-in acquisitions in the retail business in 2025.

Cost and operational efficiency initiatives are also expected to aid the company’s performance. NTR remains focused on lowering the cost of production in the potash business. It has announced several strategic actions to reduce its controllable costs and boost free cash flow. NTR has accelerated operational efficiency and cost savings initiatives, and anticipates achieving around $200 million of total savings in 2025. The company is ahead of schedule on this cost-reduction goal.

NTR generates substantial cash flows and has a healthy balance sheet, which enables it to finance its strategic growth investment, pay down debt and drive shareholder value. Its operating cash flow surged 150% year over year to $1,030 million for the first nine months of 2025, supported by higher selling prices and sales volumes.

Further, Nutrien returned $1.2 billion to its shareholders in the first nine months of 2025 through dividends and share buybacks, up around 42% from the prior-year period. NTR offers a healthy dividend yield of roughly 3.7% at the current stock price. It has a payout ratio of 57%. NTR has a five-year annualized dividend growth rate of 4.8%. Backed by sound financial health, the company's dividend is perceived as safe and reliable.

Nutrien uses sulfur and natural gas as key inputs. Supply disruptions from Russia amid the war with Ukraine contributed to the rise in natural gas prices. Plant shutdowns and maintenance also resulted in a tight supply of these inputs, which, coupled with strong demand, pushed up their prices. The company saw higher sulfur input costs and natural gas prices in the third quarter, leading to a higher cost of goods sold per ton in phosphate and nitrogen businesses, respectively. The company remains exposed to a volatile input cost environment amid supply tightness.

Earnings estimates for NTR have been rising over the past 60 days, reflecting analysts’ optimism. The Zacks Consensus Estimate for 2025 and 2026 has been revised upward over the same time frame.

NTR is currently trading at a forward price/earnings of 12.49X, a 4.4% discount compared to the industry’s average of 13.06X. It is trading at a premium to Mosaic and CF Industries. Nutrien, Mosaic and CF Industries currently have a Value Score of A, each.

NTR presents an attractive investment case, benefiting from strong global demand for crop nutrients, thanks to the underlying strength of the agricultural market and attractive farm economics. Robust demand, improving fertilizer prices and strategic growth initiatives are expected to aid its performance. Cost-reduction initiatives are also expected to boost margins. Rising earnings estimates and a solid dividend yield are the other positives. However, exposure to volatile input costs and supply tightness could pressure margins. Retaining this Zacks Rank #3 (Hold) stock will be prudent for investors who already own it.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-16 | |

| Jul-16 | |

| Jul-15 | |

| Jul-14 | |

| Jul-08 | |

| Jul-08 | |

| Jul-07 | |

| Jul-02 | |

| Jun-26 | |

| Jun-22 | |

| Jun-16 | |

| Jun-16 | |

| Jun-15 | |

| Jun-15 | |

| Jun-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite