|

|

|

|

|||||

|

|

|

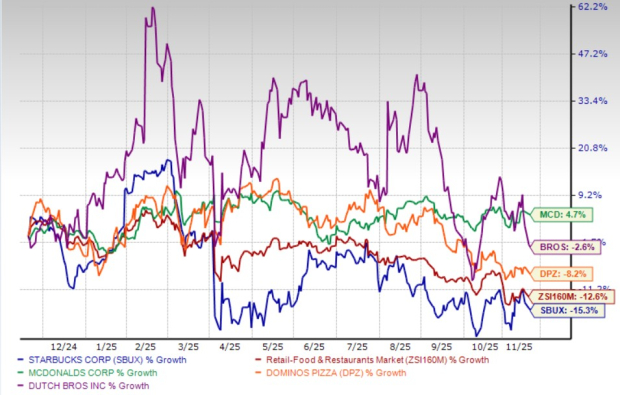

Starbucks Corporation SBUX has struggled to regain investor confidence, with shares down roughly 15% over the past year. Despite returning to positive same-store sales growth in the latest quarter, profitability remains under pressure.

Persistent headwinds, including elevated coffee costs, staffing investments and competitive dynamics, continue to weigh on margins and sentiment. In fiscal fourth-quarter 2025, the operating margin contracted 500 basis points year over year to 9.4%, primarily caused by product inflation and increased labor hours associated with the company’s revitalization strategy.

Customer traffic has also been a weak link, especially in the U.S. business. Comparable sales were flat in the quarter, as a slight improvement in ticket size could not fully offset the impact of soft transactions. The company acknowledged that turnarounds are difficult to forecast and that the investment phase will take time before returning to stronger earnings growth.

In the past year, Starbucks has also underperformed other industry players, such as McDonald's Corporation MCD, Dutch Bros Inc. BROS and Domino's Pizza, Inc. DPZ.

Starbucks is intentionally prioritizing top-line recovery before profit expansion, but that means earnings are currently lagging. Inflation in coffee beans and tariffs continues to squeeze input costs, with the CFO warning these pressures will persist at least through the first half of fiscal 2026. Meanwhile, the rollout of the Green Apron Service model, improving staffing levels and in-store service, has required additional labor investments that will only gradually annualize over the coming quarters.

With a turnaround that relies on better store-level execution, Starbucks is absorbing higher short-term costs to win back customer loyalty. EPS of 52 cents in fourth-quarter fiscal 2025 fell 34% year over year, underscoring that profits may remain muted until productivity and traffic improvements scale across the system.

In pursuit of efficiency, Starbucks has closed more than 100 unprofitable stores globally that did not meet operational standards or deliver a viable path to growth. While sales transfer has exceeded expectations, these closures still represent a reset in U.S. store economics and a modest hit to baseline revenues in the near term.

Moreover, transaction counts in the United States only recently turned the corner after seven straight quarters of declines. Younger consumers remain more selective in discretionary spending, meaning Starbucks must continually demonstrate value to stay competitive among emerging beverage concepts and lower-priced alternatives.

Despite challenges, the recovery story is taking shape. Fourth-quarter fiscal 2025 generated 5% global revenue growth and the first positive global comp in seven quarters, signaling stabilization in both the United States and key international markets. Momentum improved further in September and October, led by positive transaction-driven U.S. comps, a critical element of a durable turnaround.

Operational upgrades are already resonating with customers. Green Apron Service has boosted service quality, staffing alignment and guest perception metrics. Customer experience scores, particularly around connection and value, are strengthening, key ingredients for loyalty in a premium brand.

Starbucks’ global footprint continues to scale. International revenues hit a record $2.1 billion in fourth-quarter fiscal 2025 with strong comps in China, Japan, the United Kingdom and Mexico. China, a vital long-term market, posted 2% comparable sales growth and 9% transaction improvement, the second consecutive positive quarter, while also surpassing 8,000 stores.

Channel Development is another bright contributor, with 16% revenue growth fueled by ready-to-drink and at-home product demand through the Global Coffee Alliance. Innovations like protein beverages are expanding into major markets, helping Starbucks capture health-driven consumer trends without relying solely on cafe traffic.

The Zacks Consensus Estimate for SBUX's fiscal 2026 and 2027 EPS moved down in the last 30 days, indicating negative sentiment among analysts for its earnings.

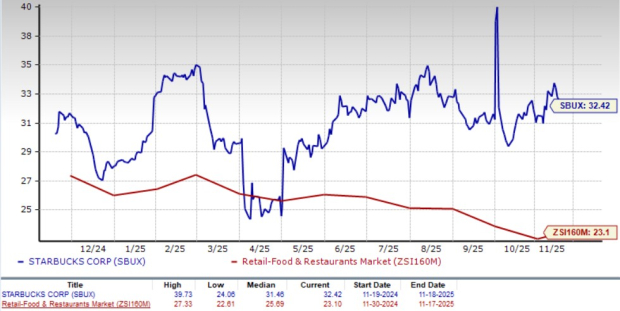

SBUX stock is trading above the industry. With a forward 12-month price/earnings ratio of 32.42X, it exceeds the industry average. The stock is also trading above other industry players like McDonald's, Dutch Bros and Domino's.

Starbucks is still in the early stages of a turnaround, and the financial pain from rising costs, heavier labor spending and soft U.S. traffic has not eased enough to restore investor confidence. Management is focused on rebuilding customer experience before profits, meaning margins and earnings are likely to remain pressured for a while.

Even with signs of operational progress, the stock already trades at a premium to peers, leaving little cushion if the recovery takes longer than expected. Until stronger demand and productivity gains fully show up in performance, the risk-reward profile appears unfavorable, making caution the smarter move for now.

Starbucks currently has a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 6 hours | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite