|

|

|

|

|||||

|

|

|

Coinbase COIN stock may be popping up on investors' radars as a buy-the-dip target amid weakness in the cryptocurrency market and broader valuation concerns in the tech sector. Trading at around $257 a share, COIN is now more than 40% from its 52-week and all-time high of $444.

Considering its fortunes are closely tied to digital assets, Coinbase stock has plunged over 25% this month with the price of Bitcoin (BTCUSD) droppping further below $100,000.

Although Coinbase is likely to benefit from higher trading volumes as the largest cryptocurrency operator in the U.S., the volatile drop in these asset prices has diminished investor sentiment as it relates to reduced fee revenue, which could ultimately lead to weaker growth prospects.

Despite the pullback in COIN, Coinbase most recently exceeded its Q3 expectations in late October and alluded to a cautiously optimistic outlook amid crypto volatility. Coinbase noted that the Crypto bull market still has room to run, emphasizing resilient liquidity conditions and a supportive macro backdrop that includes clearer regulatory frameworks.

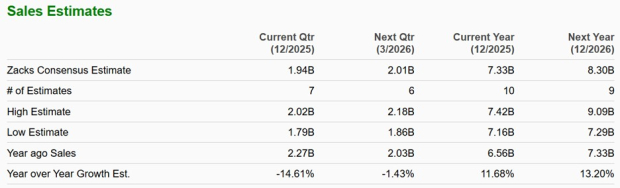

Based on Zacks' estimates, Coinbase's total sales are now expected to rise 11% this year and are projected to increase another 13% in fiscal 2026 to $8.3 billion.

On the bottom line, Coinbase’s annual earnings are currently slated to be up 5% in FY25 to $8.01. However, FY26 EPS is projected to fall to $5.87 with analysts anticipating lower trading activity, fee compression, and higher operating expenses despite strong user growth.

Paying attention to the trend of earnings estimate revisions, FY25 EPS estimates are up 14% in the last 30 days, with FY26 EPS projections slightly down.

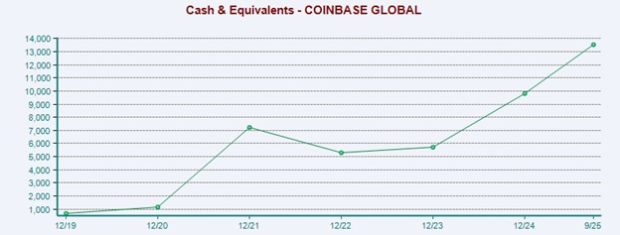

Reassuringly, Coinbase’s cash & equivalents have ballooned to over $13.5 billion. Furthermore, the company has $31.35 billion in total assets, which is nicely above its total liabilities of $15.32 billion.

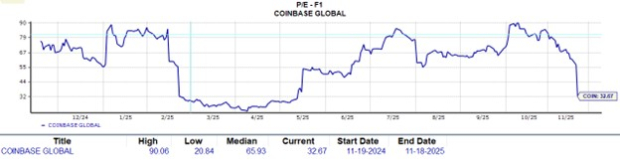

Of course, the most appealing aspect of potentially buying the dip in Coinbase stock is that COIN is starting to trade at a far more reasonable valuation. In terms of price to forward earnings, COIN is now trading at 32X compared to a lofty one-year high of 90X and a median of 65X.

It’s easy to see how Coinbase is shaping up to be one of the most appealing buy-the-dip candidates to consider, but for now, COIN lands a Zacks Rank #3 (Hold). Even with Coinbase stock trading at a more attractive price, an uptick in FY26 EPS revisions will likely be needed to solidify a buy rating.

To that point, this could keep Coinbase at a more soothing forward earnings multiple; otherwise, COIN could eventually look overvalued again, considering the anticipated drop in its bottom line.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 4 hours | |

| Jul-18 | |

| Jul-18 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite