|

|

|

|

|||||

|

|

|

NVIDIA Corp. NVDA — the undisputed global leader of generative artificial intelligence (AI)-powered graphical processing units (GPUs) — reported strong third-quarter fiscal 2026 earnings results. Adjusted earnings per share came in at $1.30, surpassing the Zacks Consensus Estimate of $1.24 and the year-ago figure of $0.81.

Revenues came in at $57.01 billion, outpacing the Zacks Consensus Estimate by 4.14% and the year-ago revenues of $35.08 billion. Year over year, third-quarter revenue increased 62.5%, marking the tenth consecutive quarter in which the revenue growth rate exceeded 50% from the prior year.

Revenues from Data Center (89.8% of revenues) jumped 66% year over year and 25% from the previous quarter to $51.22 billion. This robust rise was mainly driven by higher shipments of the Blackwell GPU computing platforms.

Within the data center revenues, around $43 billion came from compute (GPU) revenues and $8.22 billion from networking revenues. GPU revenues were primarily driven by initial sales of GB300 chips.

CEO Jensen Huang said "Blackwell sales are off the charts, and cloud GPUs are sold out." CFO Colette Kress added "Blackwell Ultra is now our leading architecture across all customer categories while our prior Blackwell architecture saw continued strong demand."

NVDA has decided to announce its roadmap for Rubin Next, to be introduced in 2027, and Feynman AI chips to be launched in 2028. NVIDIA is supported by an extremely bullish demand scenario. The company expects between $3 trillion and $4 trillion in AI infrastructure spending by the end of the decade.

Four major clients of NVDA, namely, Microsoft Corp. MSFT, Alphabet Inc. GOOGL, Meta Platforms Inc. META and Amazon.com Inc. AMZN have decided to invest a massive $380 billion in 2025 as capital expenditure for AI-infrastructure development. All these companies have forecast their AI capex spending to rise in 2026.

For the fourth quarter of fiscal 2026, NVIDIA anticipates revenues of $65 billion (+/-2%), above the Zacks Consensus Estimate of $60.3 billion. The non-GAAP gross margin is projected to be 75% (+/-50 bps). Non-GAAP operating expenses are estimated at $5 billion.

NVIDIA is increasingly focusing on powering advanced driver-assistance systems, autonomous vehicles, and robotics. Apart from the robust business of data centers and gaming, the automobile industry, especially the self-driving and new energy vehicles, is turning out to be the next catalyst.

In third-quarter fiscal 2026, automotive revenues jumped 31.9% year over year to $592 million. NVDA is expecting automotive segment revenue to cross $5 billion in fiscal 2026. Management is highly optimistic as this business could become a multitrillion-dollar opportunity in the future.

Nvidia’s Gaming business generated $4.27 billion in sales in the last reported quarter, up 30.1% year over year. OEM and Other revenues came in at $174 million, up 79.4% year over year.

NVIDIA has a return on equity (ROE) of 108% compared with the S&P 500’s ROE of 17% and the industry’s ROE of a mere 3%. NVDA has a forward P/E (price/earnings) of 41.4% compared with the industry’s P/E of 40% and the S&P 500’s P/E of 19.4%. The stock has a long-term (3-5 years) EPS growth rate of 42.3%, significantly above the S&P 500 Index’s 15.1% growth rate.

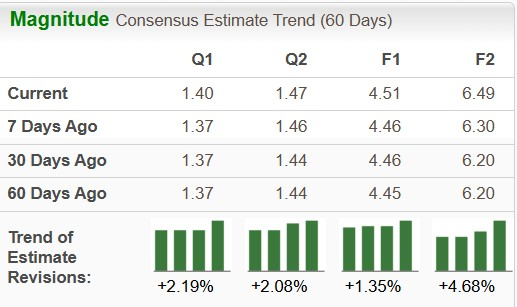

NVDA has an expected revenue and earnings growth rate of 36.1% and 43.9%, respectively, for next year (ending January 2027). The Zacks Consensus Estimate for next-year’s earnings has improved 3% over the last seven days.

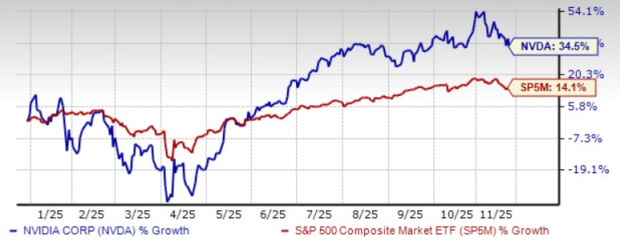

Year to date, NVIDIA has provided a 34.5% return. Yet, the short-term average price target of brokerage firms for the stock represents an increase of 32.3% from the last closing price of $180.98. The brokerage target price is currently in the range of $140-$350. This indicates a maximum upside of 93.4% and a downside of 22.7%.

NVIDIA currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

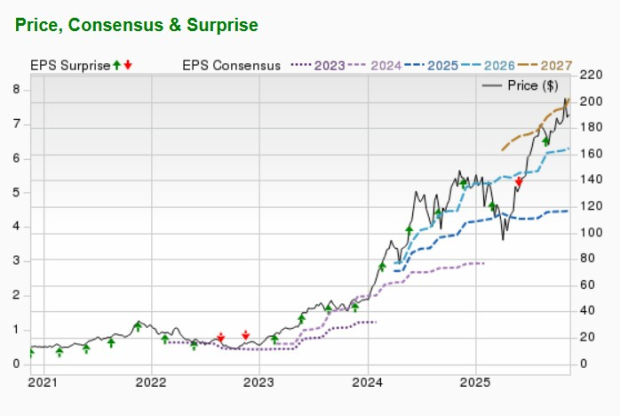

NVIDIA represents a rare opportunity to invest in a company with proven execution and substantial unrealized potential in the AI revolution. Astonishing growth potential of the global AI infrastructure market and NVDA’s strong guidance and business visibility despite revenue loss in China are noteworthy. As a result, the average target price of brokerage firms is expected to witness solid near-term upside.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 min | |

| 7 min | |

| 22 min | |

| 23 min | |

| 28 min | |

| 58 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite