|

|

|

|

|||||

|

|

|

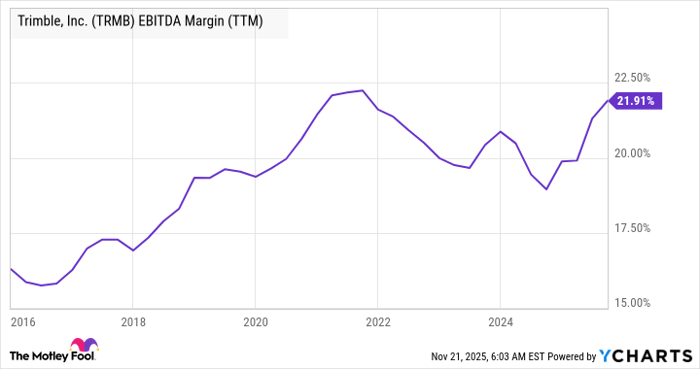

Profit margins are expanding in line with a shift to higher-margin software and services revenue.

This stock is undervalued compared to its strong long-term growth outlook.

Workflow technology company Trimble (NASDAQ: TRMB) is a rare breed. It's a highly cash-generative company growing its key metric at a mid-teens pace, and with ongoing margin expansion and market growth opportunities. Yet, it trades on highly attractive valuation multiples. As such, it's an excellent growth-at-a-reasonable-price (GARP) stock for investors willing to look beyond the headline numbers.

The company's origins lie in hardware and precision technology, helping construction/infrastructure, geospatial, agriculture, and transportation customers with precise positioning. However, its present and future lie in combining those products with software that consolidates the positioning data, analyzes it, and produces actionable insights that improve its customers' daily workflow.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

It's a growth opportunity driven by its customers' increasing adoption of digital technologies. The transition to a more software- and services-based model has steadily increased its profit margins and driven consistent mid-teens annualized recurring revenue (ARR) growth.

Data by YCharts. EBITDA = earnings before interest, taxes, depreciation, and amortization.

As CFO Phil Sawarynski noted at a recent conference, 65% of Trimble's revenue is now recurring, and 80% of its revenue is software and services. As such, the mid-teens growth in ARR is translating into free cash flow (FCF), as recurring subscriptions are relatively easy to collect and model.

The value added by its solutions (think of construction projects tightly managed according to a model, infrastructure projects like pipelines precisely managed, or transportation fleets optimized in real time) means that management expects 13% to 15% organic adjusted ARR growth in 2025.

Additionally, a growth kicker is emerging from the increasing infusion of artificial intelligence (AI) into its analytical capabilities.

Image source: Getty Images.

Wall Street expects Trimble's FCF to grow at a 26.6% annual rate from 2024 to 2027, putting Trimble on 17.6 times FCF in 2027. Management aims to return a third of FCF to investors via buybacks. All told, the valuation is far too cheap for a company with such excellent long-term growth prospects.

Before you buy stock in Trimble, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Trimble wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $562,536!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,096,510!*

Now, it’s worth noting Stock Advisor’s total average return is 981% — a market-crushing outperformance compared to 187% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of November 24, 2025

Lee Samaha has no position in any of the stocks mentioned. The Motley Fool recommends Trimble. The Motley Fool has a disclosure policy.

| Aug-05 | |

| Aug-01 | |

| Jul-30 | |

| Jul-29 | |

| Jul-27 | |

| Jul-24 | |

| Jul-23 | |

| Jul-22 | |

| Jul-16 | |

| Jul-07 | |

| Jun-01 | |

| May-29 | |

| May-12 | |

| May-06 | |

| May-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite