|

|

|

|

|||||

|

|

|

Johnson & Johnson JNJ is one of the key pharmaceutical players in the oncology segment with significant expertise in blood cancers and solid tumors.

Its Oncology segment, at present, comprises around 27% of its total revenues. Its oncology sales rose 20.6% on an operational basis in the first nine months to $18.52 billion, driven by strong market growth and share gains of key products such as multiple myeloma treatment Darzalex and prostate cancer drug, Erleada. New cancer drugs, such as Carvykti, Tecvayli, Talvey and Rybrevant, plus Lazcluze, contributed significantly to growth as they witnessed strong launches.

However, J&J has set itself quite bullish targets for the next five years. J&J expects its oncology sales to reach $50 billion by the end of the decade.

J&J seems quite confident of the target, citing strong growth in its marketed cancer drugs and new launches like Inlexzoh/TAR-200 in high-risk non-muscle invasive bladder cancer and the subcutaneous formulation of Rybrevant plus Lazcluze for advanced EGFR-mutated non-small cell lung cancer.

Inlexzoh was approved by the FDA in September this year. It is the first-of-its-kind drug-releasing system to provide sustained local delivery of a cancer treatment directly into the bladder. The subcutaneous formulation of Rybrevant plus Lazcluze was approved in the EU in April 2025, while it is under review in the United States.

Meanwhile, J&J’s oncology pipeline has gained strong momentum in the last couple of years with promising developments in colorectal and head and neck cancers. In this period, J&J had eight proof-of-concept readouts, which led the candidates to move to late-stage pivotal studies across the portfolio. If these pipeline drugs are eventually approved, they can also boost JNJ’s oncology sales.

J&J is also building its oncology pipeline through M&A deals. Earlier this month, it announced a definitive agreement to acquire Halda Therapeutics, a clinical-stage biotech developing targeted oral cancer medicines, for $3.05 billion in cash. The deal will strengthen J&J’s broader oncology pipeline, mainly in prostate cancer, where it already has a strong presence with drugs like Zytiga, Erleada and Akeega.

In the five years from 2019 to 2024, J&J’s oncology sales doubled from $10.7 billion to $20.8 billion. To achieve the $50 billion target in the next 5-6 years, the company needs to more than double its sales from 2024 levels. Though quite optimistic, the target is not unachievable.

Other large players in the oncology space are Pfizer PFE, AstraZeneca AZN, Merck MRK and Bristol-Myers.

Pfizer boasts a strong portfolio of approved cancer medicines like Xtandi, Lorbrena and the Braftovi-Mektovi combination. The addition of Seagen in 2023 also strengthened its position in oncology by adding four antibody-drug conjugates (ADCs) — Adcetris, Padcev, Tukysa and Tivdak. Pfizer also has a robust pipeline of cancer candidates with a focus on multiple modalities, including small molecules, ADCs and immuno-oncology biologics.

For AstraZeneca, oncology sales now comprise around 43% of total revenues and rose 16% in the first nine months of 2025. AstraZeneca’s strong oncology sales growth is being driven by medicines such as Tagrisso, Lynparza, Imfinzi, Calquence and Enhertu (in partnership with Daiichi Sankyo). AstraZeneca is working on strengthening its oncology product portfolio through label expansions of existing products and progressing oncology pipeline candidates.

Merck’s key oncology medicines are PD-L1 inhibitor, Keytruda and PARP inhibitor, Lynparza, which it markets in partnership with AstraZeneca. Oncology drives more than 60% of Merck’s total revenues, with its blockbuster cancer drug Keytruda, approved for several types of cancer, contributing more than 50% of the company’s pharmaceutical sales.

Bristol-Myers’ key cancer drug is PD-L1 inhibitor, Opdivo, which accounts for around 20% of its total revenues.

J&J’s shares have outperformed the industry year to date. The stock has risen 43.5% in the year-to-date period compared with an increase of 18.8% for the industry.

From a valuation standpoint, J&J is reasonably priced. Going by the price/earnings ratio, the company’s shares currently trade at 18.17 forward earnings, higher than 17.43 for the industry. The stock is also trading below its five-year mean of 15.65.

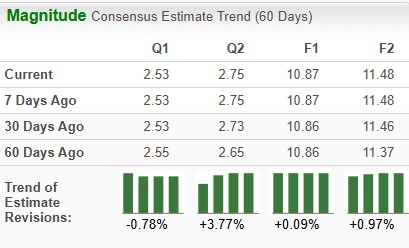

The Zacks Consensus Estimate for 2025 earnings has risen from $10.86 per share to $10.87 over the past 60 days, while that for 2026 has risen from $11.37 to $11.48 over the same timeframe.

J&J has a Zacks Rank #3 (Hold) currently. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 17 min | |

| 47 min | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 |

MSD wins FDA approval for cholesterol pill to help plug Keytruda void

AZN MRK

Pharmaceutical Technology

|

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite