|

|

|

|

|||||

|

|

|

About the Industry

The Internet Software & Services industry is a relatively small industry, primarily involved in enabling platforms, networks, solutions and services for online businesses and facilitating customer interaction and use of Internet based services.

Top Themes Driving the Industry

Zacks Industry Rank Indicates Improving Prospects

The Zacks Internet – Software & Services industry is housed within the broader Zacks Computer and Technology sector. It carries a Zacks Industry Rank #42, which places it in the top 17% of nearly 245 Zacks-classified industries.

The group’s Zacks Industry Rank, which is basically the average of the Zacks Rank of all the member stocks, indicates that the growth prospects are improving. Our research shows that the top 50% of the Zacks-ranked industries outperforms the bottom 50% by a factor of more than 2 to 1.

The aggregate estimate revision trend reflects an improving situation. So although the estimates for fiscal year 2025 have averaged a decline of 3.7%, those for 2026 are up 4.6% over the past year. Estimates for both years have moved around quite a bit, with April, May and September being the weakest months.

Before we present a few stocks that you may want to consider for your portfolio, let’s take a look at the industry’s recent stock-market performance and valuation picture.

Industry's Stock Market Performance Is Strong

The Zacks Internet – Software & Services Industry has traded at a premium to both the broader Zacks Computer and Technology Sector and the S&P 500 since the beginning of 2025.

Overall, the industry returned 33% over the past year compared with the broader sector’s return of 27.6% and the S&P 500’s 16.3%.

One-Year Price Performance

Industry's Valuation Is Attractive

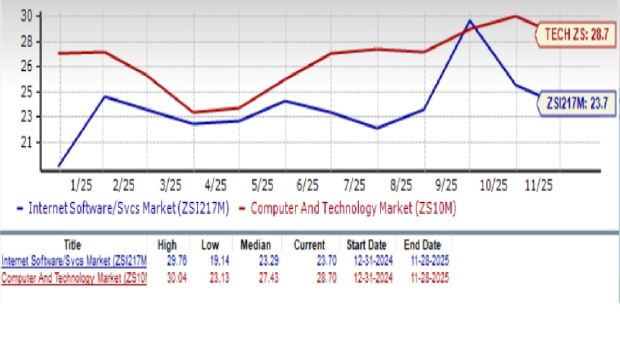

On the basis of forward 12-month price-to-earnings (P/E) ratio, we see that the industry is currently trading at 223.7X, slightly above its median level of 23.29X, which is a 0.4% premium to the S&P 500 and a 17.4% discount to the technology sector. Technology stocks usually trade at a higher multiple because investors pay a higher premium for innovation. Therefore, in this case, indications are that the shares in this industry are not overvalued on average and that there may be some attractive ones to pursue.

The industry has traded in the range of 19.14X to 29.76X over the past year, as the chart below shows.

Forward 12 Month Price-to-Earnings (P/E) Ratio

2 Stocks Worth Considering

Criteo S.A. (CRTO): Paris-based Criteo S.A. provides a commerce media platform delivering marketing and monetization services in North and South America, Europe, the Middle East, Africa, and the Asia-Pacific. Its unified, AI-driven platform directly connects advertisers with retailers and publishers to drive commerce on retailer sites and on the open Internet.

The company’s strategy is to harness AI to expand its reach across audiences, seeking to expand its ecosystem across advertisers, retailers and third-party platforms, using the commerce dataset to feed its AI models.

As advertiser budgets are sensitive to macroeconomic factors like the geopolitical conflicts in Ukraine and the Middle East, as well as things like inflation and interest rates back home, this market hasn’t done exceptionally well in the past year. However, the last quarter was relatively stable with some categories like office supplies, furniture and personal care seeing increased year-over-year back-to-school advertising spend. Its client retention remained close to 90% in the last quarter.

Overall Retail Media ex-TAC contribution growth was 11%, with adoption expanding across 4,100 brands. New retail partners include DoorDash, Sephora, The Fragrance Shop, Zepto, Migros, Interdiscount and Massmart.

The company announced a partnership with Google Search, which will go into effect in the current quarter. The deal makes Criteo the first third-party partner to provide retail media inventory in the Americas. The integration with Google’s platform will allow advertisers to manage campaigns across Criteo’s network through Google Search Ads 360. This opens up an estimated $172 billion in addressable spend, a portion of which will be reflected in its Retail Media performance over time. Data, AI and global reach are what advertisers look for in an ad tech provider, and the company is growing its capability on all fronts.

Performance media ex-TAC contribution growth was a more sedate 5%, helped by growing strength in GO!, its AI-powered commerce solution. GO! automates the campaign creation process, optimizing display ad campaigns for both customer acquisition and for re-engaging existing customers. It is primarily targeted at small and medium sized businesses. Management says that 25% of campaigns from its small clients now run through GO!, compared with 10% in the last quarter. This number is expected to double by year-end.

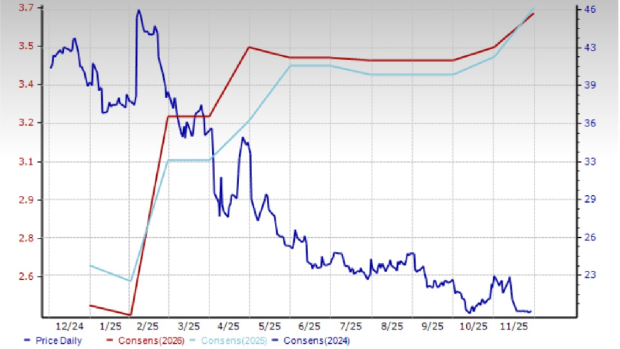

Shares of this Zacks Rank #1 (Strong Buy) company have lost 53.5% over the past year. The Zacks Consensus Estimate for 2025 is up 25 cents (5.6%) in the last 30 days. The 2026 earnings estimate is up 21 cents (4.7%). Analysts expect sales to increase 4.5% this year with earnings growing 2.6%. Earnings are currently expected to grow 0.4% the following year on the back of 2.4% revenue growth.

Price and Consensus: CRTO

NetEase, Inc. (NTES): Hangzhou-based NetEase provides online services based on diverse content, including games, music, other services and education (dictionary, translation and including a range of smart devices) in China. Its products and services are focused on community, communication and commerce, infusing play with culture, and education with technology.

Gaming is its primary growth engine and the largest contributor to revenue by far. NetEase has one of the largest in-house R&D teams in gaming with a very broad focus across mobile, PC and console channels. This is generating tremendous momentum in its business right now.

Some of the popular titles in the last quarter included Fantasy Westward Journey mobile game, Identity V, Eggy Party, Sword of Justice and Where Winds Meet. for instance, its Identity V, Where Winds Meet, Marvel Rivalsit and several other newly launched titles did very well. The strength in gaming, its largest segment by far, offset softness in other segments where the company is pursuing more profitable business.

Fresh content is also driving its international business. New games included Destiny: Rising, ANANTA and Sword of Justice were some of the popular new titles. Sea of Remnants is in the pipeline and expected to launch next year. Management noted “healthy growth in China and rising global appeal.”

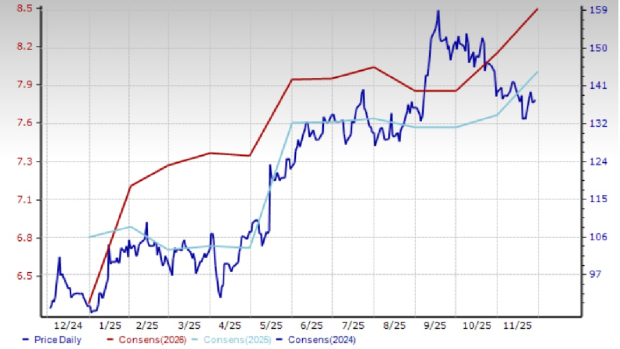

Shares of this Zacks Rank #2 (Buy) company have gained 59% over the past year. NetEase’s earnings for the June quarter were just short of the Zacks Consensus Estimate with revenues missing by around 3%. The Zacks Consensus Estimate for 2025 has increased 6 cents to $8.61 in the last 60 days while that for 2026 has increased 26 cents to $9.30. Analysts currently expect 2025 revenue and earnings to grow a respective 10% and 21.3%. Estimates for the following year are currently expected to grow 7.7% and 8%.

Price and Consensus: NTES

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-22 | |

| Jul-22 | |

| Jul-16 | |

| Jul-16 | |

| Jul-06 | |

| Jul-06 | |

| Jul-06 | |

| Jun-23 | |

| Jun-23 | |

| Jun-22 | |

| Jun-22 | |

| Jun-09 | |

| Jun-03 | |

| May-31 | |

| May-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite