|

|

|

|

|||||

|

|

|

On Nov. 19, Copa Holdings CPA reported its third-quarter 2025 financial results, highlighting strong demand, solid revenue growth and robust operational excellence. The company continued to expand its fleet, maintain best-in-class on-time performance and deliver value to shareholders through healthy profitability and dividends.

Copa Holdings reported third-quarter 2025 earnings per share (EPS) of $4.20, which surpassed the Zacks Consensus Estimate of $4.03 and improved 20% year over year. Revenues of $913.1 million missed the Zacks Consensus Estimate of $915 million, but increased 6.8% year over year.

Net profit rose 18.7% to $173.4 million, with operating and net margins reaching 23.2% and 19.0%, respectively. To meet rising demand, CPA is expanding capacity. CPA ended the quarter with $1.3 billion in liquidity and a low adjusted net debt-to-EBITDA ratio of 0.7x. Fleet expansion continued with new Boeing 737 MAX 8 deliveries, while on-time performance and flight completion remained among the best in the industry. Supported by strong operational metrics, CPA, along with LATAM Airlines Group LTM, Ryanair Holdings RYAAY and Allegiant ALGT, demonstrated resilience in capturing market demand and sustaining profitability in a competitive landscape.

In October, available seat miles (ASM: a measure of capacity) were up 9.6% year over year, and revenue passenger miles (RPM) increased 9.3%. The load factor came in at 87.2%, as traffic growth slightly lagged capacity expansion.

Other carriers also saw strong demand in October. LATAM Airlines Group reported a consolidated load factor of 85.5% and a 7.4% year-over-year increase in capacity. Ryanair Holdings transported 19.2 million passengers in October 2025, reflecting a 5% year-over-year increase, with a load factor of 93%. Allegiant carried 27.6% more passengers than a year ago, achieving a load factor of 81.9%, while system-wide capacity rose 20.2%. LATAM Airlines Group, Ryanair Holdings and Allegiant benefited from the same demand swell that supported CPA’s traffic growth, highlighting the broad strength of the market.

CPA’s management expects consolidated capacity to grow 8% (prior view: up 7-8%) year over year, and the operating margin is expected to be in the range of 22-23% (prior view: 21-23%). The fuel cost is expected to be $2.47 per gallon (prior view: $2.45).

RASM is still expected to be 11.2 cents. The load factor for the current year is expected to be 87%. Non-fuel unit costs are anticipated to be 5.8 cents.

Preliminarily, for 2026, CPA currently anticipates its capacity to grow by almost 11-13% on a year-over-year basis, with unit costs excluding fuel (Ex-Fuel CASM) expected to be in the range of 5.7 to 5.8 cents.

Copa Holdings expects to end 2025 with 124 aircraft (prior view: 125 aircraft) and 2026 with 132 aircraft (prior view: 131 aircraft).

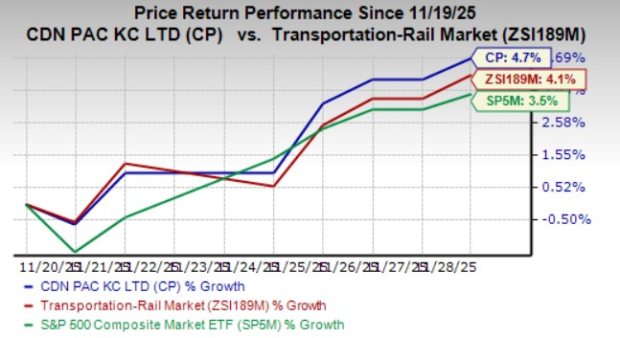

Shares of Copa Holdings have performed handsomely post third-quarter 2025 earnings beat, outperforming the Zacks Transportation - Airline industry and the S&P 500 index.

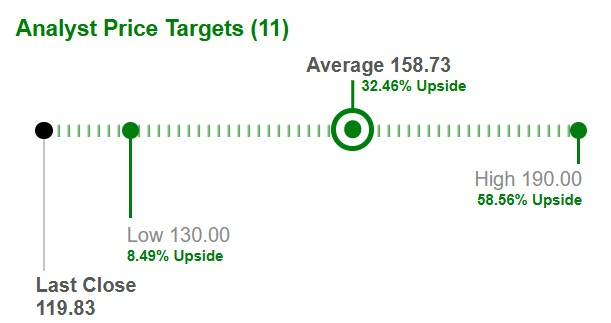

Based on short-term price targets offered by 11 analysts, the Wall Street average price target is at $158.73 per share, suggesting a 32.5% upside from current levels.

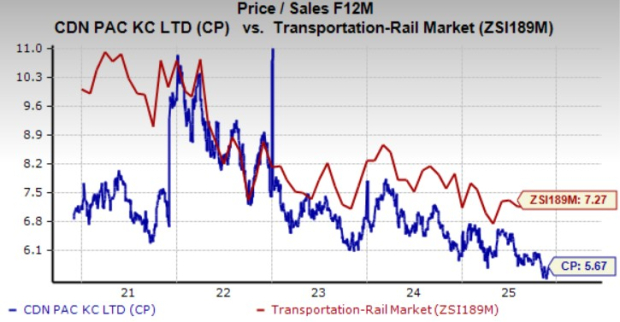

From a valuation perspective, CPA is trading at a discount compared with the industry, going by the forward 12-month price-to-sales ratio. The company has a Value Score of A.

The uptick in total operating expenses—rising 2.9% year over year to $700.84 million in the third quarter of 2025 —despite tailwinds from lower fuel and maintenance costs. It underscores mounting inflationary pressure across the cost base. Labor-related expenses climbed 5.4%, sales and distribution outlays advanced 6.6%, passenger servicing costs increased 4.8%, and airport facilities and handling charges surged 8.8%. These increases highlight the company’s limited operational leverage and the structural rigidity of its expense profile, even as capacity expands.

The uptick across these key cost centers also casts doubt on the company’s margin resilience in the coming quarters. Other operating and administrative expenses rose 3.5% from the third quarter of 2024, further reinforcing the persistent upward cost drift. Although capacity growth may support revenue generation, the disproportionate escalation in personnel, distribution and airport-related costs threatens to compress operating margins without more robust cost-containment measures. Overall, the sustained uptick across essential expense categories creates a challenging cost architecture that could impede future profitability.

For long-term investors, a single quarter’s performance is less critical than the company’s underlying fundamentals. While Copa Holdings delivered impressive third-quarter results, potential investors should exercise caution and avoid rushing to buy, given the challenges the company faces. It is advisable to monitor CPA’s progress and wait for a more favorable entry point. Existing shareholders, however, can consider maintaining their positions, as the stock’s long-term prospects remain solid. The Zacks Rank #3 (Hold) further reinforces this cautious outlook.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 2 hours | |

| 11 hours | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Jul-29 | |

| Jul-28 | |

| Jul-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite