|

|

|

|

|||||

|

|

|

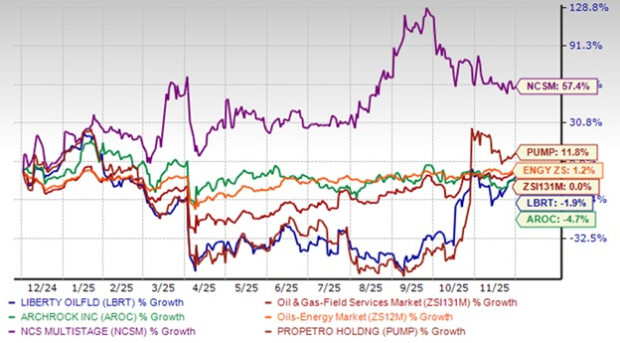

Liberty Energy Inc. LBRT has lagged behind its peers, with shares down 1.9%, clearly underperforming relative to broader benchmarks. The Oil & Gas-Field Services sub-industry (ZSI131M) remained flat, while the broader Oil-Energy sector posted a modest 1.2% gain. Among competitors, Archrock Inc. AROC recorded a 4.7% decline. ProPetro Holding Corp. PUMP delivered a positive return of 11.8%, demonstrating stronger momentum. NCS Multistage Holdings, Inc. NCSM significantly outperformed the entire group, surging 57.4% over the same period. Overall, LBRT’s negative performance stands out as notably weaker than both industry indicators and key competitors.

12- Month Performance Snapshot

The share price performance above highlights that Liberty Energy is struggling to maintain its market position, likely due to a mix of operational challenges, market volatility and potentially flawed business strategies. Let us take a closer look at the key factors affecting LBRT stock’s performance.

Significant Near-Term Margin Compression in Core Business: Denver, CO-basedoil and gas equipment and services company is facing substantial profitability headwinds, with third-quarter 2025 adjusted EBITDA falling 29% sequentially and 48% year over year. This sharp decline, caused by pricing pressure and lower industry activity, highlights the cyclical vulnerability of its primary oilfield services revenue stream, which may persist in the near term.

Similar challenges can be observed at Archrock, where its exposure to fluctuating demand for natural gas compression services can lead to sharp profitability declines in market downturns. In comparison, ProPetro Holding faces similar headwinds in the pressure pumping sector, where oversupply and pricing pressure can impact margins. NCS Multistage Holdings may also be affected by these cyclical fluctuations, particularly given its focus on completion technologies and services in the oil and gas space.

Heavy Capital Expenditures Amid Cyclical Trough: The company forecasts 2025 capital expenditures between $525 million and $550 million, a significant outlay during a market downturn. With net debt increasing $99 million in the quarter and a shift of future capital toward power, there is a risk of straining liquidity and returns if the core business recovery is delayed.

Uncertain Timing and Conversion of Power Contracts: While the power pipeline is large, the chief executive officer of the company acknowledged that converting opportunities into firm, announced contracts takes longer than in the oilfield services business. This execution risk and lack of near-term revenue visibility from the power segment create uncertainty for investors expecting immediate payoff from the growth strategy.

Execution and Integration Risks in a New Business Line: Building a multi-gigawatt power generation business is a complex endeavor involving new technologies, long-duration contracts and project financing. Any missteps in execution, project delays or failure to achieve projected returns could negatively impact Liberty Energy's financial performance and reputation.

Persistent Macroeconomic and Industry Headwinds: The company's outlook points to ongoing macroeconomic uncertainty and oil producer discipline, which are expected to keep industry completions activity subdued in the near term. These external factors are largely outside of LBRT's control and continue to pressure its traditional revenue base.

Increasing Financial Leverage and Liquidity Pressure: LBRT ended the third quarter with $13 million in cash and $253 million in debt, drawing on its credit facility. Total liquidity of $146 million may be pressured by ongoing capital expenditures and dividends, potentially necessitating further borrowing or external financing sooner than anticipated.

Potential for Customer Concentration in Power Segment: The power business is expected to be heavily concentrated with a handful of large data center customers. While these may be creditworthy, high reliance on a small number of clients introduces counterparty risk and reduces diversification, making the company more susceptible to delays or cancellations from any single major customer.

Archrock faces similar risks, especially in its power generation segment, which could be reliant on a small number of large energy customers or projects. While ProPetro Holding is more diversified within the oilfield services sector, there is still exposure to key customers who drive a large portion of revenues. NCS Multistage, while smaller in scale, could similarly face challenges with customer concentration, particularly in a market with fewer large operators.

Dilution of Strategic Focus and Management Attention: The aggressive push into the complex power generation business risks diverting critical management focus and corporate resources away from Liberty Energy's core completions franchise. Navigating a new industry with different customer dynamics, regulatory hurdles and project finance structures could lead to operational missteps in either the new venture or the legacy business if management bandwidth becomes stretched too thin.

Project Finance Complexity and Off-Balance-Sheet Risk: While using project-specific, non-recourse debt is prudent, it adds significant financial and operational complexity. Managing numerous special-purpose entities, each with its own financing and performance guarantees, increases administrative burden and creates potential for hidden liabilities or performance disputes that could eventually impact the parent company's reputation or financials, even without formal recourse.

Vulnerability to Natural Gas Price Volatility: LBRT's power business model, heavily reliant on natural gas-fueled reciprocating engines, directly ties its future profitability and value proposition to customers to the long-term price of natural gas. While management believes that it can provide price certainty, a sustained, significant increase in North American natural gas prices could erode the competitive "grid parity" advantage. The company is currently selling, making its solutions less attractive.

This Zacks Rank #4 (Sell) company is facing significant challenges, including near-term margin compression in its core oilfield services business, which has seen a sharp decline in profitability due to pricing pressure and lower industry activity. The company is also heavily investing in capital expenditures amid a cyclical downturn, raising concerns about liquidity and the ability to recover. While the company is diversifying into power generation, the uncertain timing and conversion of power contracts, along with execution risks, add to the uncertainty.

Additionally, financial leverage is increasing and the company faces macroeconomic pressures, potential customer concentration risks, and operational distractions from its push into the power sector. Unless the company shows improved financial results and greater operational stability, investors may be better off exploring other opportunities in the oil and gas sector.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite