|

|

|

|

|||||

|

|

|

Orion has had an impressive run over the past six months as its shares have beaten the S&P 500 by 6.5%. The stock now trades at $10.30, marking a 20.6% gain. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in Orion, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free for active Edge members.

Despite the momentum, we don't have much confidence in Orion. Here are three reasons you should be careful with ORN and a stock we'd rather own.

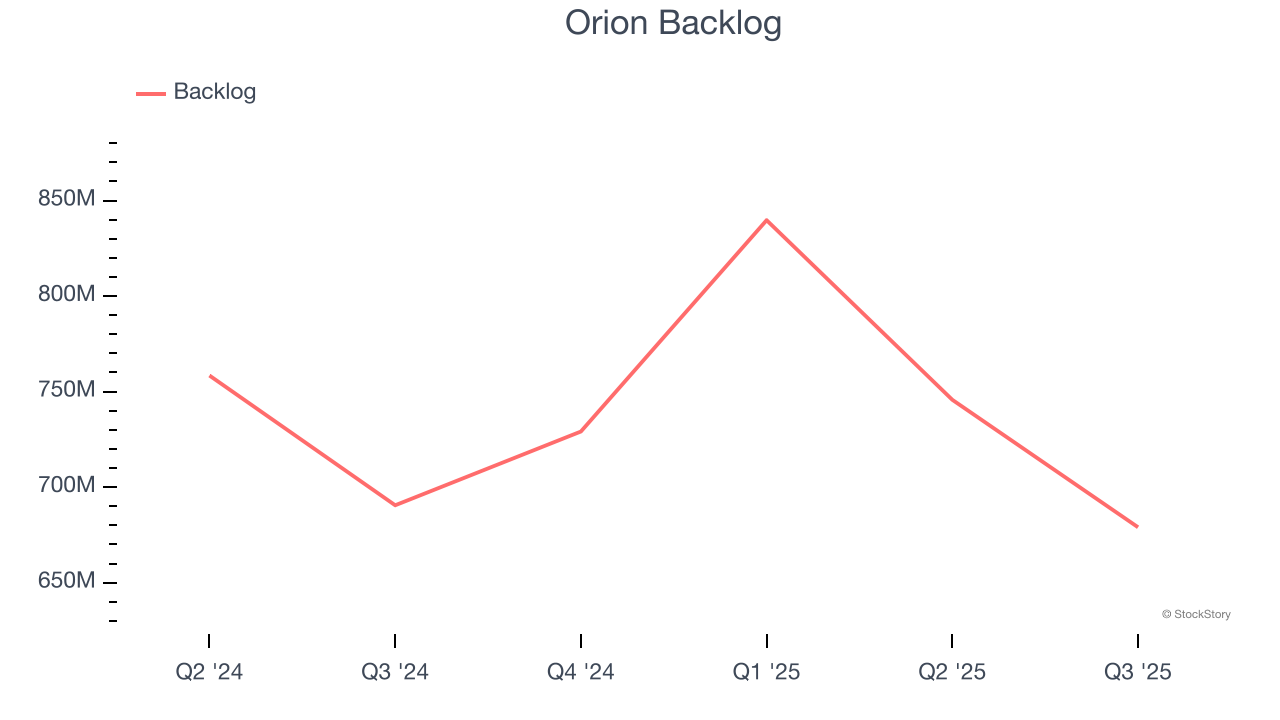

We can better understand Construction and Maintenance Services companies by analyzing their backlog. This metric shows the value of outstanding orders that have not yet been executed or delivered, giving visibility into Orion’s future revenue streams.

Orion’s backlog came in at $679 million in the latest quarter, and it averaged 1.7% year-on-year declines over the last two years. This performance was underwhelming and shows the company is not winning new orders. It also suggests there may be increasing competition or market saturation.

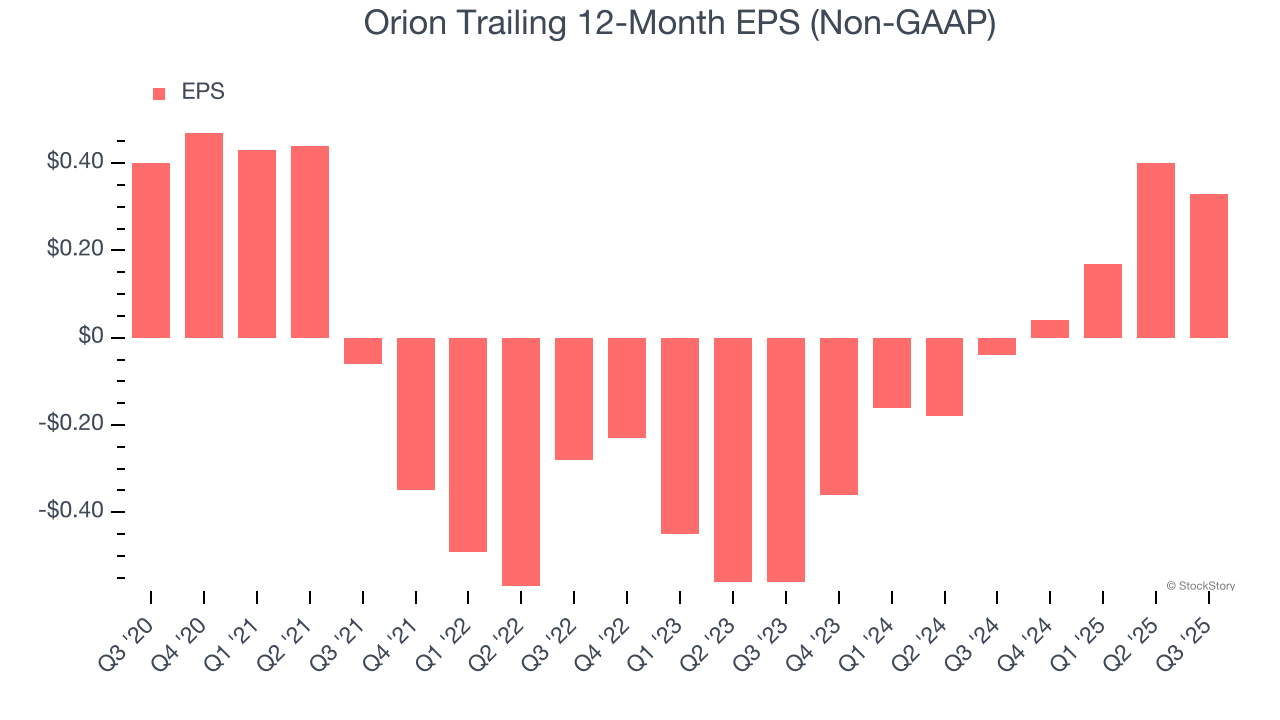

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Orion, its EPS declined by 3.8% annually over the last five years while its revenue grew by 2.5%. This tells us the company became less profitable on a per-share basis as it expanded.

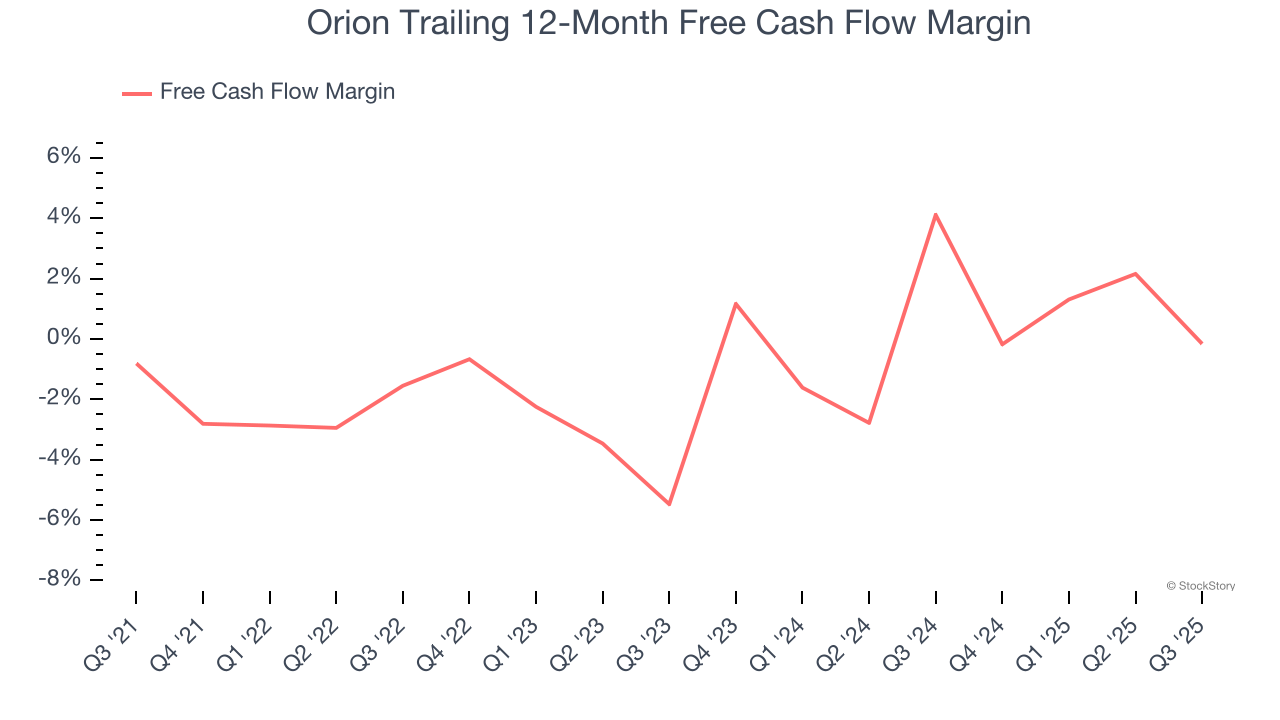

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Orion broke even from a free cash flow perspective over the last five years, giving the company limited opportunities to return capital to shareholders.

Orion doesn’t pass our quality test. With its shares beating the market recently, the stock trades at 39.1× forward P/E (or $10.30 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think other companies feature superior fundamentals at the moment. We’d recommend looking at a dominant Aerospace business that has perfected its M&A strategy.

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-14 | |

| May-18 | |

| Apr-29 | |

| Apr-28 | |

| Apr-08 | |

| Mar-19 | |

| Mar-17 | |

| Mar-06 | |

| Mar-05 | |

| Mar-04 | |

| Mar-04 | |

| Mar-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite