|

|

|

|

|||||

|

|

|

Zacks Rank #5 (Strong Sell) stock RH (RH), formerly Restoration Hardware, is a high-end home furnishings company based in California. RH is a staple in many malls and shopping centers across the United States and offers a plethora of upscale home goods via its 70 galleries, outlets, catalogs, and websites. Selling products through its sizable galleries, RH’s product line includes home décor, furniture (including outdoor), bathroom products and bathware, and lighting. While RH’s primary focus is upscale interior products, the company expanded into the hospitality business in 2015, offering a handful of RH branded cafés restaurants, and hotels. RH’s core business is in the US, though it has expanded to Europe and Canada.

The story of Wall Street and the 2025 market thus far is the Trump Administration’s aggressive tariff policy aimed at bringing manufacturing back to the United States, improving trade imbalances, and seeking to achieve better trade deals with other countries. Unfortunately, as of 2024, RH sources ~72% of its products from Asia (including 35% from Vietnam, 23% from China, and the rest from Indonesia and India).

RH addressed supply chain issues earlier this month, saying, “The company has been operating with 25% tariffs from China since the last Trump administration and has successfully resourced the majority of its China production to Vietnam at significantly better than pre-tariff landed China pricing. In addition, the company has successfully resourced a meaningful amount of its China production to its own factory in North Carolina.”

While it’s encouraging to see the company adapt, investor concerns remain. RH is still reliant on China, and moving its supply chain to Vietnam will take time and money. In addition, there is little clarity on trade deals with Indonesia and India at the time of this writing.

Though RH margins are being squeezed due to tariffs, that is not the only concern the company faces. Consumer confidence has been falling recently and RH’s deep-pocketed customer base may temper spending as it waits for a clearer macroeconomic picture to emerge. Gross margins have sunk from more than 50% to 44.8% since 2022.

Maintaining luxury showrooms, paying rent, and upending its supply chain have led to rampant spending of more than $1 billion last year. To make matters worse, the company’s debt is soaring and there is no end to the spending in sight.

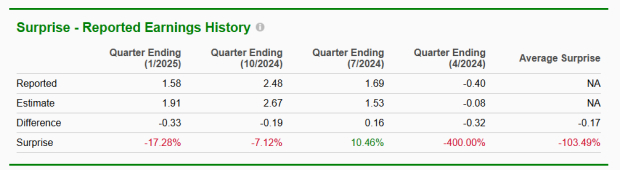

RH’s earnings trajectory is moving in the wrong direction for bulls, missing Zacks Consensus Estimates by an average of 103.49% over the past four quarters.

RH shares plunged more than 40% as volume swelled to more than 10x the norm following the company’s latest earnings announcement. Such ugly price and volume action are symbolic of heavy distribution. In addition, RH is carving out a bearish flag pattern.

Bottom Line

Luxury home furnishing retailer RH faces several bearish headwinds, including tariff policy, ballooning debt, and margin pressures. A worst-possible Zacks Rank and a bearish chart pattern add to the concern.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| Feb-10 | |

| Feb-09 | |

| Feb-02 | |

| Feb-01 | |

| Jan-23 | |

| Jan-22 | |

| Jan-18 | |

| Jan-16 | |

| Jan-14 | |

| Jan-12 | |

| Jan-12 | |

| Jan-06 | |

| Jan-06 | |

| Jan-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite