|

|

|

|

|||||

|

|

|

OGE Energy Corp.’s OGE ongoing capital investments, focused carbon-reduction initiatives and a robust renewable generation portfolio collectively position it for stronger long-term performance. These efforts are expected to enhance grid reliability, support cleaner operations and drive sustainable growth across its service territory.

However, this Zacks Rank #3 (Hold) company faces risks related to supply-chain disruption.

OGE Energy continues to expand its renewable portfolio to capture incentives tied to large clean-energy investments. The company currently operates several wind farms totaling nearly 450 MW and multiple solar sites with 32.2 MW of capacity (as of Dec. 31, 2024). It also offers voluntary renewable programs for Oklahoma retail customers and plans to keep adding zero-emission resources to strengthen its clean-energy footprint.

OGE Energy is pursuing an aggressive investment strategy to upgrade its infrastructure and provide seamless services to its customers. The company plans to spend $6.50 billion between 2025 and 2029. The figure rose 4% from its prior five-year capital expenditure plan of $6.25 billion. With these capital investments, the company aims to maintain and improve the safety, resiliency and reliability of its distribution and transmission grid and generation fleet.

Backed by such a solid investment strategy, the company expects long-term earnings growth of 5-7%. Apart from bolstering customer growth, valuable returns from such investment strategies should also enable OGE Energy to continue to reward its shareholders through steady dividend hikes.

In recent times, factors like raw material inflation, logistical challenges and certain component shortages have resulted in supply-chain disruption within the utility market. These have also resulted in supply-chain disruption and may continue to cause delays in construction activities and equipment deliveries related to OGE Energy’s capital projects.

Moreover, rising electricity production costs due to increased fuel prices, inflation and shortage of components also pose a risk for electricity manufacturers like OGE Energy. The company’s fuel, purchased power and transmission expenses surged 11% year over year in the third quarter of 2025.

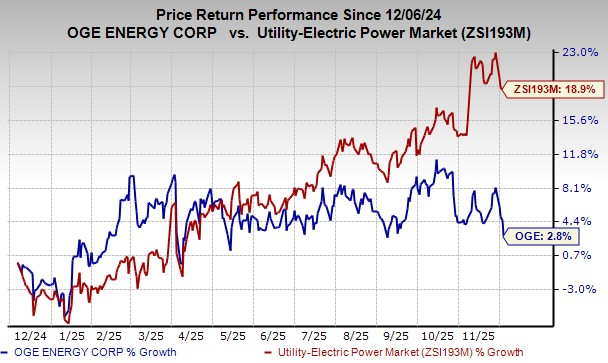

In the past year, shares of the company have risen 2.8% compared with the industry’s 18.9% growth.

Some better-ranked stocks from the same industry are Ameren AEE, CenterPoint Energy CNP and Portland General Electric POR, each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Ameren’s long-term (three to five years) earnings growth rate is 8.52%. The Zacks Consensus Estimate for AEE’s 2025 EPS implies an improvement of 8% from that recorded in 2024.

CNP’s long-term earnings growth rate is 8.86%. The Zacks Consensus Estimate for CNP’s 2025 EPS implies an improvement of 9.3% from that recorded in 2024.

POR’s long-term earnings growth rate is 3.39%. The Zacks Consensus Estimate for POR’s 2025 EPS implies an improvement of 2.6% from that recorded in 2024.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite