|

|

|

|

|||||

|

|

|

Looking back on environmental and facilities services stocks’ Q3 earnings, we examine this quarter’s best and worst performers, including Rollins (NYSE:ROL) and its peers.

Many environmental and facility services are non-discretionary (sports stadiums need to be cleaned after events), recurring, and performed through longer-term contracts. This makes for more predictable and stickier revenue streams. Additionally, there has been an increasing focus on emissions and water conservation over the last decade, driving innovation in the sector and demand for new services. Despite these tailwinds, environmental and facility services companies are still at the whim of economic cycles. Interest rates, for example, can greatly impact commercial construction projects that drive incremental demand for these services.

The 12 environmental and facilities services stocks we track reported a mixed Q3. As a group, revenues beat analysts’ consensus estimates by 1.8% while next quarter’s revenue guidance was 1.7% below.

Luckily, environmental and facilities services stocks have performed well with share prices up 12.2% on average since the latest earnings results.

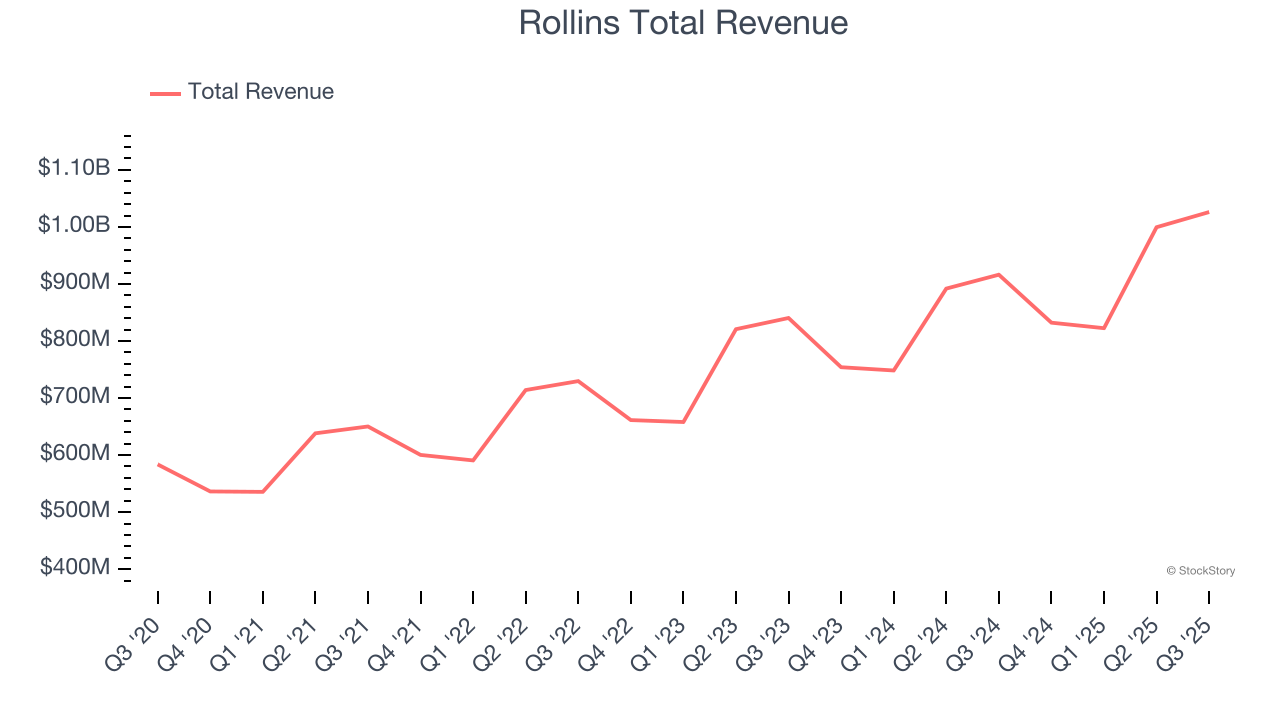

Operating under multiple brands like Orkin and HomeTeam Pest Defense, Rollins (NYSE:ROL) provides pest and wildlife control services to residential and commercial customers.

Rollins reported revenues of $1.03 billion, up 12% year on year. This print was in line with analysts’ expectations, and overall, it was a strong quarter for the company with an impressive beat of analysts’ adjusted operating income estimates and a solid beat of analysts’ EBITDA estimates.

"We delivered a strong third quarter with record revenue and an improving margin profile, a reflection of an ongoing commitment to execution by our teammates," said Jerry Gahlhoff, Jr., President and CEO.

Interestingly, the stock is up 13.9% since reporting and currently trades at $61.34.

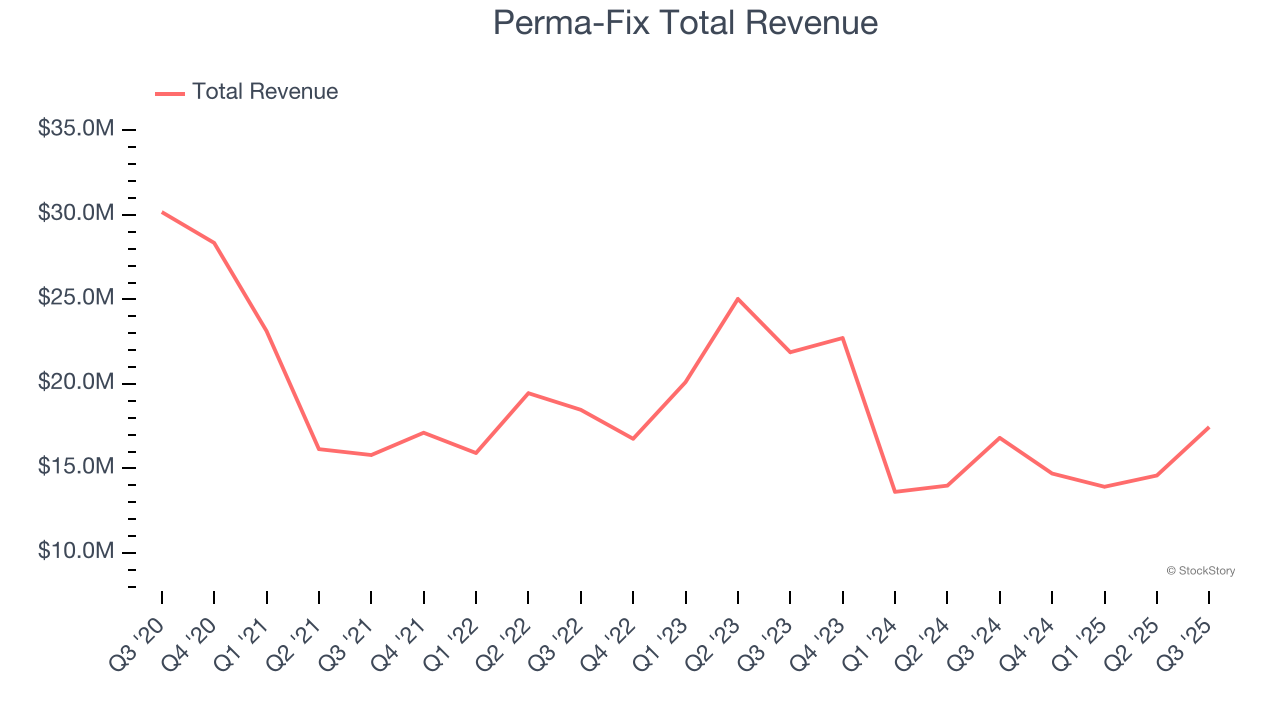

Tackling hazardous waste challenges since 1990, Perma-Fix (NASDAQ:PESI) provides environmental waste treatment services.

Perma-Fix reported revenues of $17.45 million, up 3.8% year on year, outperforming analysts’ expectations by 7.1%. The business had a stunning quarter with a solid beat of analysts’ EBITDA estimates and an impressive beat of analysts’ revenue estimates.

The market seems happy with the results as the stock is up 9.1% since reporting. It currently trades at $14.04.

Is now the time to buy Perma-Fix? Access our full analysis of the earnings results here, it’s free for active Edge members.

Established in 1980, Clean Harbors (NYSE:CLH) provides environmental and industrial services like hazardous and non-hazardous waste disposal and emergency spill cleanups.

Clean Harbors reported revenues of $1.55 billion, up 1.3% year on year, falling short of analysts’ expectations by 1.6%. It was a disappointing quarter as it posted a significant miss of analysts’ adjusted operating income estimates and a significant miss of analysts’ EPS estimates.

As expected, the stock is down 3.6% since the results and currently trades at $237.21.

Read our full analysis of Clean Harbors’s results here.

An official field consultant for Major League Baseball, BrightView (NYSE:BV) offers landscaping design, development, and maintenance.

BrightView reported revenues of $702.8 million, down 3.6% year on year. This print came in 2.8% below analysts' expectations. Overall, it was a softer quarter as it also recorded a significant miss of analysts’ revenue estimates and a significant miss of analysts’ adjusted operating income estimates.

BrightView achieved the highest full-year guidance raise but had the weakest performance against analyst estimates among its peers. The stock is up 5.8% since reporting and currently trades at $12.54.

Read our full, actionable report on BrightView here, it’s free for active Edge members.

Spun off from Danaher in 2023, Veralto (NYSE:VLTO) provides water analytics and treatment solutions.

Veralto reported revenues of $1.40 billion, up 6.8% year on year. This number was in line with analysts’ expectations. Aside from that, it was a satisfactory quarter as it also produced full-year EPS guidance slightly topping analysts’ expectations but revenue guidance for next quarter slightly missing analysts’ expectations.

The stock is flat since reporting and currently trades at $102.05.

Read our full, actionable report on Veralto here, it’s free for active Edge members.

As a result of the Fed’s rate hikes in 2022 and 2023, inflation has come down from frothy levels post-pandemic. The general rise in the price of goods and services is trending towards the Fed’s 2% goal as of late, which is good news. The higher rates that fought inflation also didn't slow economic activity enough to catalyze a recession. So far, soft landing. This, combined with recent rate cuts (half a percent in September 2024 and a quarter percent in November 2024) have led to strong stock market performance in 2024. The icing on the cake for 2024 returns was Donald Trump’s victory in the U.S. Presidential Election in early November, sending major indices to all-time highs in the week following the election. Still, debates around the health of the economy and the impact of potential tariffs and corporate tax cuts remain, leaving much uncertainty around 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-08 | |

| Jul-07 | |

| Jun-30 | |

| Jun-16 | |

| Jun-01 | |

| May-31 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite