|

|

|

|

|||||

|

|

|

Over the last six months, Lindsay’s shares have sunk to $118.79, producing a disappointing 13.4% loss - a stark contrast to the S&P 500’s 14.1% gain. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in Lindsay, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free for active Edge members.

Despite the more favorable entry price, we don't have much confidence in Lindsay. Here are three reasons there are better opportunities than LNN and a stock we'd rather own.

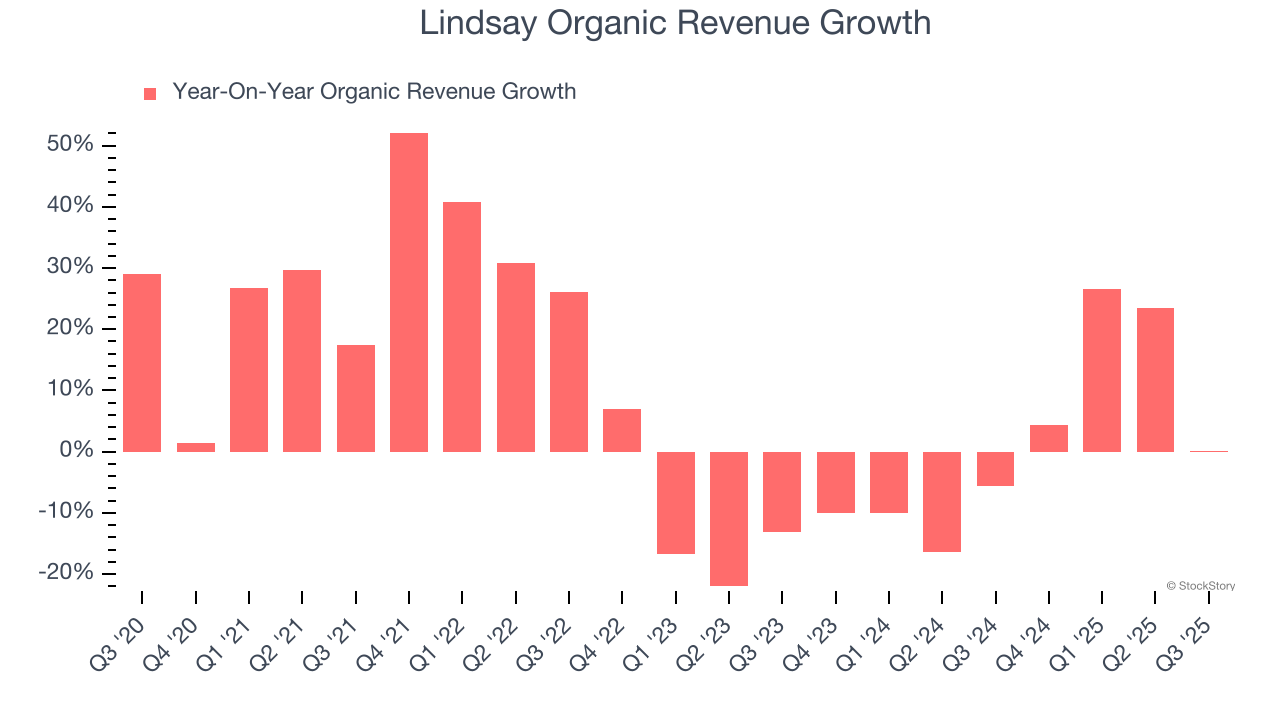

Investors interested in Agricultural Machinery companies should track organic revenue in addition to reported revenue. This metric gives visibility into Lindsay’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Lindsay’s organic revenue averaged 1.6% year-on-year growth. This performance was underwhelming and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Lindsay’s revenue to stall, close to its 7.3% annualized growth for the past five years. This projection is underwhelming and suggests its newer products and services will not lead to better top-line performance yet.

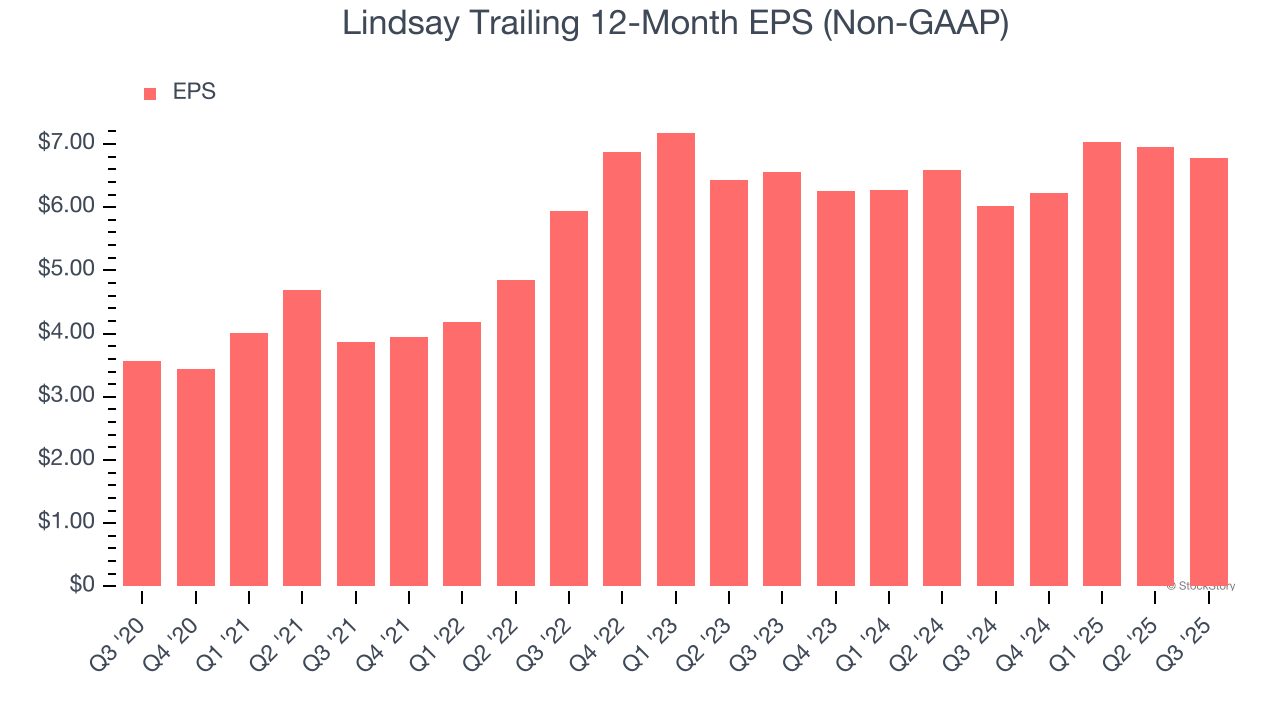

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Lindsay’s weak 1.7% annual EPS growth over the last two years aligns with its revenue trend. This tells us it maintained its per-share profitability as it expanded.

Lindsay isn’t a terrible business, but it isn’t one of our picks. Following the recent decline, the stock trades at 19.5× forward P/E (or $118.79 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're pretty confident there are superior stocks to buy right now. We’d suggest looking at one of Charlie Munger’s all-time favorite businesses.

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Jul-06 | |

| Jul-02 | |

| Jul-02 | |

| Jul-02 | |

| Jul-02 | |

| Jul-02 | |

| Jun-18 | |

| Apr-03 | |

| Apr-03 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Mar-19 | |

| Mar-06 | |

| Mar-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite