|

|

|

|

|||||

|

|

|

Pembina Pipeline Corporation PBA is a leading energy transportation and midstream service provider of North America, primarily focused on the transportation, storage and processing of oil, natural gas and natural gas liquids. Founded in 1954 and headquartered in Calgary, Alberta, Pembina operates a vast network of pipelines and facilities across Canada and the United States. Its infrastructure includes an extensive array of pipelines, processing plants and storage terminals that facilitate the safe and efficient movement of energy products.

PBA plays a crucial role in the energy sector by providing essential infrastructure that enables the movement of raw and refined energy products from production sites to refineries, markets and export terminals. As a key player in the midstream segment, PBA is integral to the entire supply chain, ensuring the timely delivery of vital energy resources. The company's strategic investments and ability to adapt to the changing energy landscape make it a linchpin for energy producers, consumers and stakeholders.

Moreover, its consistent focus on innovation and operational excellence allows Pembina to contribute significantly to Canada's energy security while driving economic growth and job creation in the region.

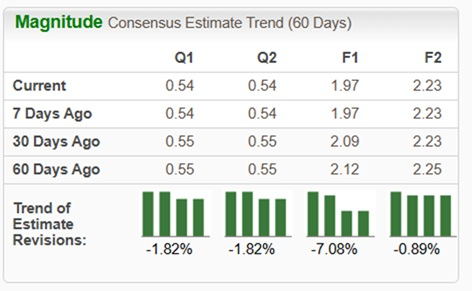

Over the past 60 days, the Zacks Consensus Estimate for PBA’s earnings per share has remained unchanged for both the first quarter and the second quarter, while the estimates for the next and the following fiscal year (F1 & F2) have decreased 7.08% and 0.89%, respectively.

Strong and Stable Financial Performance With Increased Guidance Precision: PBA reported a solid fiscal third quarter with adjusted EBITDA of C$1034 million, a 1% year-over-year increase, demonstrating resilience in its core operations. The company has effectively narrowed its full-year 2025 adjusted EBITDA guidance to a more precise range of C$4.25-C$4.35 billion, indicating management's confidence in predictable cash flows despite market volatility. This financial stability is underpinned by a predominantly fee-based, long-term contracted revenue model, providing reliable visibility for investors.

Significant Long-Term Contracting Successes Strengthening the Core Business: The company has successfully reconstructed all volumes

substantially up for renewal in 2025 and 2026, including a recent 50,000-barrel-per-day agreement on the Peace Pipeline system with a weighted average term of approximately 10 years. Furthermore, shippers on the critical Alliance Pipeline have elected 10-year tolls on approximately 96% of its firm capacity. These achievements lock in long-term, take-or-pay revenue streams, de-risking the base business and ensuring high utilization rates for years to come.

Strategic Growth in LNG With Cedar LNG Partnership Validates Export Strategy: PBA has signed a pivotal 20-year agreement with global LNG leader PETRONAS for 1 million tons per annum of capacity at the Cedar LNG facility. This deal not only secures a long-term revenue stream for a major growth project but also validates the competitiveness and strategic value of Pembina's LNG export ambitions. The project remains on time and on budget for a late-2028 in-service date, with the potential to capture market upside through the agreement's synthetic tolling structure.

Diversification Into Power Generation With the Greenlight Electricity Center: The Greenlight project, a proposed 1.8-gigawatt natural gas-fired power generation facility, represents a strategic extension of Pembina's value chain into contracted energy infrastructure. With a grid allocation secured and assigned to a customer for potential 2027 use, and a final investment decision targeted for the first half of 2026, this initiative diversifies Pembina's customer base and creates incremental demand for its natural gas and liquids handling services, leveraging assets like the nearby Alliance Pipeline.

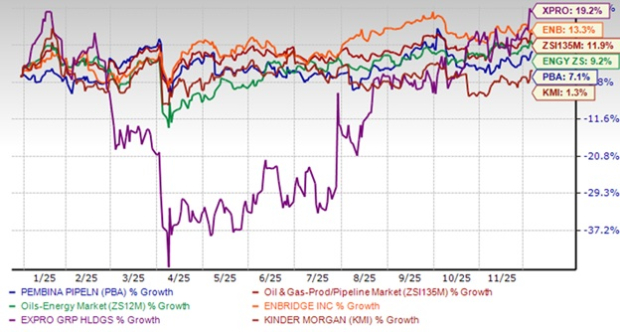

Underperformance of PBA in the Current Market: PBA has significantly underperformed in the year-to-date (“YTD”) period. With an increase of just 7.1%, PBA lagged behind the Oil & Gas Production and Pipelines sub-industry (ZSI135M), which saw growth of 11.9% and the broader Oil-Energy sector (ZS12M), which rose 9.2%. Additionally, PBA trailed key competitors such as Enbridge Inc. ENB, with a rise of 13.3%, and Expro Group Holdings XPRO, which surged 19.2%.

Another peer, Kinder Morgan KMI, was a modest performer with growth of 1.3%. This data highlights that PBA has underperformed compared with both its sector and some of industry peers in the YTD period.

Guidance Midpoint Revision Reflects Reduced Near-Term Optionality: While the full-year 2025 adjusted EBITDA guidance was narrowed, the midpoint was slightly reduced. Management acknowledged this was due to expecting "a little less optionality" in the marketing business than previously anticipated for the latter half of the year. This indicates that even the company's resilient model is not entirely immune to weaker-than-expected commodity market conditions affecting its more volatile segments.

Limited Near-Term Cash Flow From Major Growth Initiatives: Capital-intensive projects like Cedar LNG and Greenlight require significant upfront investment years before generating cash flow. Cedar LNG is not expected to be in service until late 2028, and Greenlight's first phase cash flows are anticipated in 2030. This long gestation period ties up capital that could otherwise be used for dividends, debt reduction or other immediate-return opportunities.

Execution and Macro Risks for Large Growth Projects: Major growth projects like Cedar LNG and the Greenlight Electricity Centre carry inherent execution risks related to cost overruns, timing delays and final investment decisions. Furthermore, Cedar LNG's economics are tied to global LNG arbitrage dynamics, while Greenlight's timeline is partially dependent on a customer's data center build-out and regulatory processes, introducing elements beyond Pembina's full control.

The risks associated with large-scale projects, such as cost overruns or delays, are not unique to Pembina. Enbridge has faced similar challenges with the multi-billion-dollar pipeline expansions, while Expro Group Holdings has managed risks by diversifying its project portfolio. Kinder Morgan has also faced execution hurdles but has been relatively more conservative in project rollouts, providing a cautionary tale for PBA as it moves forward with growth initiatives.

PBA has demonstrated strong financial performance with solid third-quarter results and increased guidance precision, driven by a fee-based revenue model and successful long-term contracting, such as a key agreement with PETRONAS for the Cedar LNG project. Additionally, its foray into power generation through the Greenlight project offers further diversification and growth potential.

However, the stock has underperformed in the market, lagging behind industry peers and its reduced EBITDA guidance reflects weaker-than-expected performance in certain segments. Large capital-intensive projects, like Cedar LNG and Greenlight, involve long gestation periods and execution risks, limiting near-term cash flow.

Given this mix of strengths and potential challenges, investors should wait for a more opportune entry point instead of adding this Zacks Rank #3 (Hold) stock to their portfolios.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 |

Enbridge begins construction on $2.8bn British Columbia pipeline expansion

ENB

World Construction Network

|

| Jul-16 | |

| Jul-15 | |

| Jul-14 | |

| Jul-09 | |

| Jul-08 | |

| Jul-03 | |

| Jul-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite