|

|

|

|

|||||

|

|

|

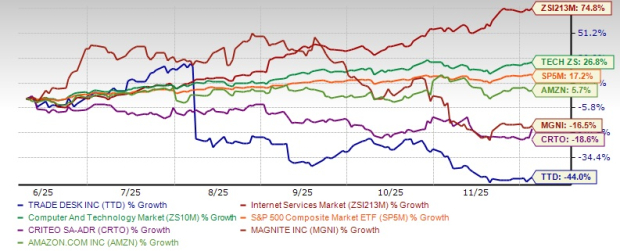

The Trade Desk TTD stock has seen a sharp 44% slide over the past six months, an uncomfortable drawdown for a company viewed as one of ad tech’s leading players.

TTD’s decline stands in sharp contrast to the Zacks Internet Services industry’s growth of 74.8% over the same time frame, while the Zacks Computer & Technology sector and the S&P 500 composite have gained 26.8% and 17.2%, respectively.

The company substantially lags other ad tech players like Amazon AMZN, Magnite MGNI and Criteo CRTO. AMZN has gained 5.7% while both MGNI and CRTO are down 16.5% and 18.6%, respectively.

TTD’s sharp decline appears to be caused more by company-specific challenges than broader market trends. For many investors, the selloff raises a pressing question: Is this an opportunity to accumulate shares amid temporary turbulence or a warning sign of deeper troubles?

Let’s unpack the issues behind the recent price slump and evaluate whether holding onto the stock is a smart move.

Even with the recent share-price pressure, there are several tailwinds that continue to support The Trade Desk’s long-term narrative. These include CTV, retail media, Kokai, international growth and supply-chain modernization efforts, including OpenPath.

Increasing digital spending in CTV remains amid the transition from linear TV, which is a key growth driver. On the last earnings call, management noted that the transition toward biddable CTV is gaining rapid momentum and it expects decision CTV to become the default buying model in the future. The benefits of decision-based buying (like greater flexibility, control and performance) compared with traditional programmatic guaranteed or insertion-order models, are rendering it the logical choice for advertisers.

The rapid rise of retail media networks bodes well. Retail media’s acceleration is fueled by rising demand for measurable, lower-funnel outcomes. Retailers are embracing Trade Desk as a partner because the platform seamlessly integrates retail data with identity solutions like UID2, enabling precise targeting and attribution across the open Internet.

Kokai, TTD’s next-generation AI-powered DSP experience, remains central to its strategy. 85% clients use Kokai as their default experience, and this is strengthening its competitive moat. TTD highlighted that Kokai delivered (on average) 26% better cost per acquisition, 58% better cost per unique reach and a 94% better click-through rate compared with Solimar. Embedding AI to enhance Kokai bodes well.

The Trade Desk price-consensus-eps-surprise-chart | The Trade Desk Quote

TTD’s OpenPath, Deal Desk, Pubdesk and OpenAds initiatives further strengthen its ecosystem by connecting advertisers directly to publishers, improving transparency and supply-chain efficiency.

The Trade Desk’s strategy revolves around the open Internet, which is where price discovery and competition exist. Management noted that average consumers spend about two-thirds of their online time on the open Internet, but advertisers allocate far less than that proportion of their budgets.

Management estimates that about 60% of its total addressable market lies outside the United States. International business currently represents roughly 13% of total revenues, a clear opportunity for long-term growth.

TTD boasts a strong balance sheet with a cash position (cash, cash equivalents and short-term investments) of $1.4 billion at the end of the third quarter, with no debt. As digital advertising shifts toward AI-driven, outcome-based campaigns, The Trade Desk’s cash strength offers a buffer against macro volatility. In a market increasingly defined by capital discipline and platform efficiency, The Trade Desk’s liquidity and free cash flow generation may prove to be one of its most durable advantages.

The company repurchased $310 million worth of stock in the third quarter and approved a new buyback plan of $500 million. For the fourth quarter of 2025, the company anticipates revenues of at least $840 million.

Analysts have marginally revised earnings estimates upwards for 2025.

TTD is focused on embedding AI across the portfolio, which will further raise capex and operational costs. Rising expenses coupled with investments could compress margins if revenue growth slows. In the last reported quarter, total operating costs (excluding stock-based compensation) surged 17% year over year to $457 million. Expenses soared on account of continued investments in boosting platform capabilities, particularly platform operations.

Moreover, macro volatility is immensely concerning for The Trade Desk. If macro headwinds worsen, revenue growth may face pressure due to reduced programmatic demand.

While The Trade Desk remains a leading independent DSP, the competitive environment is intensifying. Walled gardens like Meta Platforms, Apple, Google and Amazon dominate this space as they control their inventory and first-party user data, allowing for highly targeted ad campaigns. While CTV remains a strong revenue driver, this market is also increasingly becoming competitive. AMZN’s expanding DSP business is giving tough competition to TTD, especially in this space.

Though TTD is focusing on geographic expansion, executing well across disparate markets can be complex and risky. Regulatory and privacy-related changes like the deprecation of cookies and tightening data-privacy laws like Europe’s GDPR also pose ongoing challenges.

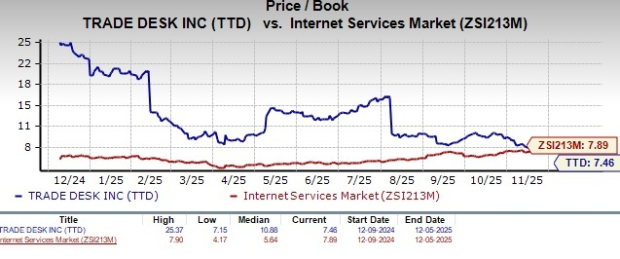

TTD stock is not so cheap, as its Value Style Score of D suggests a stretched valuation at this moment. The stock is trading at a price/book multiple of 7.46X compared with the industry’s 7.89X.

AMZN, MGNI and CRTO trade at 6.64X, 2.58X and 0.94X, respectively.

Though TTD has several long-term catalysts, such as the rise of CTV, expanding retail media networks and the growing adoption of Kokai, the near-term picture remains muddled by macro uncertainty, rising expenses and intensifying competitive pressure from both walled gardens and independent ad-tech peers

Given the mix of solid fundamentals and near-term headwinds, investors holding TTD stock can retain it in their portfolios for now, but new investors would be better off waiting for a favorable entry point.

At present, TTD carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 4 hours | |

| 7 hours | |

| Jul-19 | |

| Jul-19 | |

| Jul-19 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite