|

|

|

|

|||||

|

|

|

MercadoLibre’s MELI lending arm has become a powerful driver of engagement inside Mercado Pago and its rapid expansion is shaping the company’s operating profile. The credit portfolio is scaling across its main markets as more users adopt the credit card and financing tools that tie payments, commerce and financial services together. This deeper integration is strengthening usage, but the speed of expansion brings its own set of margin and risk considerations.

In the third quarter of 2025, the total credit portfolio increased 83% year over year to $11 billion, with growth spread across consumer, merchant and asset-backed segments. Credit cards continue to account for a rising share of originations, shifting the mix toward longer-duration products. Net Interest Margin After Losses stood at 21%, easing sequentially as funding costs climbed sharply in Argentina, while asset quality remained broadly stable with 6.8% of loans between 15 and 90 days past due and 17.6% more than 90 days past due.

Fintech revenues continue to reflect this momentum. The Zacks Consensus Estimate for fourth-quarter 2025 fintech revenues is pegged at $3.63 billion, indicating a 45% year-over-year increase, suggesting that credit-driven revenue growth will remain robust even as the company absorbs higher provisioning and funding requirements associated with a larger book.

However, as the mix leans further into credit cards, new cohorts will take time to reach breakeven, keeping returns under pressure during issuance-heavy periods. The pace of loan expansion suggests that MELI’s growing credit book could introduce periods of margin strain even as engagement improves. The combination of longer-duration credit cards, rising funding costs and slower cohort maturity means lending may support revenue growth while still limiting profitability in the near term. Whether this expansion becomes a sustained advantage or a mounting risk will hinge on the company’s ability to keep spreads stable and asset quality intact.

Competition is tightening for MELI as Sea Limited SE and Nu Holdings NU deepen their push into digital lending across Latin America. Sea Limited is scaling personal loans and payment products in Brazil and Mexico, competing directly in segments where MercadoLibre is growing its credit exposure. Nu Holdings is also accelerating credit card issuance and consumer lending, leveraging a large active user base and increasingly sophisticated underwriting models. As Sea Limited and Nu Holdings expand their fintech footprint and compete more aggressively for the same borrowers, MercadoLibre may face added pressure on credit pricing, acquisition costs and lending margins.

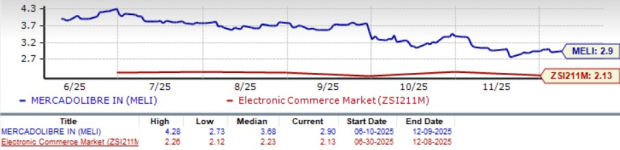

MELI shares have declined 13.1% in the past six months, underperforming the Zacks Internet-Commerce industry and the Zacks Retail-Wholesale sector’s increase of 6.3% and 5.1%, respectively.

From a valuation standpoint, MELI stock is currently trading at a forward 12-month Price/Sales ratio of 2.9X compared with the industry’s 2.13X. MELI has a Value Score of C.

The Zacks Consensus Estimate for MELI’s fourth-quarter 2025 earnings is pegged at $11.85 per share, unchanged over the past 30 days, indicating a 6.03% year-over-year decline.

MercadoLibre, Inc. price-consensus-chart | MercadoLibre, Inc. Quote

MercadoLibre currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 6 hours | |

| 6 hours | |

| 7 hours | |

| 7 hours | |

| 13 hours | |

| Jul-31 | |

| Jul-30 | |

| Jul-29 | |

| Jul-28 | |

| Jul-24 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite