|

|

|

|

|||||

|

|

|

The Trade Desk TTD is entering its next phase of expansion with a financial profile that underscores capacity for long-term investment.

TTD had a strong balance sheet at the end of the third quarter, having cash, cash equivalents and short-term investments of $1.4 billion with no debt. Moreover, the company continues to generate healthy profitability and cash flow. It delivered $739 million in revenues, which grew 18% year over year. Adjusted EBITDA reached $317 million, while free cash flow totaled $155 million. The company’s consistent cash generation and a 43% adjusted EBITDA margin highlight its operational efficiency.

The financial firepower gives TTD significant room to maneuver as it accelerates innovation, scales AI-driven capabilities and deepens its presence across global markets.

TTD is deploying resources to boost AI-driven platforms like Kokai and data transparency tools like OpenPath and Sincera. Among its clients, 85% use Kokai as their default experience. This strengthens its competitive moat. TTD highlighted that Kokai delivered (on average) 26% lower cost per acquisition, 58% lower cost per unique reach and a 94% higher click-through rate compared with Solimar. Embedding AI to enhance Kokai bodes well.

Management estimates that about 60% of its total addressable market lies outside the United States. International business currently represents roughly 13% of total revenues, a clear opportunity for long-term growth.

As digital advertising shifts toward AI-driven, outcome-based campaigns, TTD’s cash strength offers a buffer against macro volatility. In a market increasingly defined by capital discipline and platform efficiency, its liquidity and free cash flow generation may prove to be one of its most durable advantages.

The company’s commitment to boost shareholder value through stock repurchases is noteworthy. TTD repurchased $310 million worth of stock in the third quarter, and approving a new $500 million buyback plan. This approach not only offsets dilution but signals confidence in long-term cash generation.

However, TTD needs to remain cautious amid macroeconomic uncertainty and rising expenses. Competition in the ad-tech space is also a cause of concern.

Amazon AMZN is ramping up investment in DSP and CTV businesses, putting it in direct competition with TTD. It remains upbeat about its DSP platform, which allows advertisers to plan, activate and measure full-funnel campaigns. Partnerships with Roku and Netflix and integrations with Spotify and SiriusXM bode well.

In the last reported quarter, AMZN’s ad business delivered $17.6 billion in revenues, up 22% year over year. Ads are still a relatively small share of Amazon’s total revenue base compared with retail and AWS, meaning there is ample room to scale. Investors should note that AMZN’s business diversification, especially retail, cloud and AI, with stupendous financial resources, gives it an edge over rivals. As of Sept. 30, 2025, cash and cash equivalents were $66.9 billion, while the long-term debt was $50.7 billion.

PubMatic PUBM ended the third quarter with $136.5 million in cash and zero debt. This gives it a high level of flexibility as it accelerates diversification of its DSP mix, expands investment on the buy side, boosts its CTV and emerging revenue streams and integrates AI across operations and product portfolio.

It generated $32.4 million in net operating cash flow and $22.8 million in free cash flow. At the same time, PUBM is committed to returning capital to shareholders, having brought back 12.4 million shares for $180.6 million since 2023, with $94.4 million remaining authorized through 2026.

Shares of TTD have lost 10.4% in the past month against the Internet – Services industry’s gain of 10.1%.

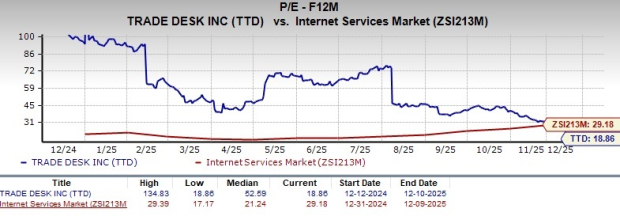

In terms of forward price/earnings, TTD’s shares are trading at 18.86X compared with the Internet Services industry’s ratio of 29.18X.

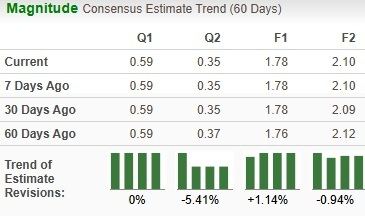

The Zacks Consensus Estimate for TTD’s earnings for 2025 has been marginally revised upwards over the past 60 days.

TTD currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 4 hours | |

| 7 hours | |

| Jul-19 | |

| Jul-19 | |

| Jul-19 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite