|

|

|

|

|||||

|

|

|

Investors should note that 2026 is shaping up as a pivotal year for Chevron Corporation (CVX) and Suncor Energy (SU). Both companies have outlined detailed operational plans and capital priorities that will define their financial and strategic trajectories. For investors weighing these two integrated Oil/Energy names, the matchup comes down to growth momentum, cash-flow predictability, capital efficiency and exposure to commodity-price swings.

Below is a comparison designed to help investors navigate these differences.

Chevron’s 2026 plan is anchored by a series of major upstream catalysts. The Tengizchevroil (TCO) expansion is expected to operate at full production rates, contributing meaningful volumes and cash flow. Gulf of America deepwater projects continue to ramp up, and management has highlighted that the Permian Basin is on track to reach 1 million barrels of oil equivalent per day, marking a key milestone for the portfolio. The completed Hess integration adds scale and improves long-term cash-generation potential, supported by roughly $1.5 billion in targeted synergies.

These catalysts feed directly into Chevron’s outlook for strong free-cash-flow growth. The company expects about $12.5 billion of additional annual free cash flow by 2026, supported by disciplined capital spending and a resilient asset base.

Chevron is targeting $3 to $4 billion in structural cost reductions, with more than 60% expected from efficiency gains. The Hess transaction also drives meaningful operating-cost improvements. Together, these initiatives enhance unit economics across Chevron’s global portfolio.

Chevron maintains one of the most consistent shareholder-return frameworks in the sector, prioritizing steady dividend growth and flexible buybacks. Management plans to repurchase $10 to $20 billion in shares annually, adjusted for commodity prices.

Chevron’s diversified asset base across North America, Asia and Africa reduces exposure to any single market or commodity stream. Low-breakeven barrels and a strong balance sheet support durability in downcycles.

Suncor’s structural advantage lies in its very low corporate decline rate and the stability of its long-life oil sands assets. Mining and upgrading operations show near-zero decline, and the company has combined this with record reliability across the upstream and downstream network. In 2024, utilization hit record highs across multiple assets, and refinery utilization has recently averaged 101% to 102%, underscoring sustained operational execution.

Suncor’s business model supports predictable free-funds-flow generation even in mid-$60 WTI environments. Its 2026 plan maintains this stability by combining disciplined sustaining capital with targeted economic investments, including in situ well pads, Fort Hills development and downstream optimization.

Suncor approaches efficiency from a different angle, emphasizing operational turnaround performance and breakeven reductions. Management has executed best-ever turnaround durations at multiple assets, lowered its WTI breakeven by $7 per barrel in 2024, and now operates at cost levels that are better than many peers. Its 2026 plan continues this momentum with targeted investments to improve flexibility and durability across the oil sands network.

Suncor’s capital-return strategy is more assertive. With net debt already at its C$8 billion target, the company has shifted to returning at or near 100% of excess funds to its shareholders. This includes both buybacks and a dividend targeted to grow 3-5% annually. Suncor’s track record of high retail and downstream margins helps reinforce the reliability of these returns.

Suncor is more concentrated in oil sands, which ties performance more tightly to heavy-oil differentials and refining-market strength. However, its cash flow sensitivities remain manageable, and its integrated network of mining, in situ, and downstream assets helps cushion price volatility.

Year-to-date price action favors Suncor, with SU shares up 24.2%, significantly outperforming Chevron’s 4.1% gain. This divergence reflects improving sentiment around Suncor’s operational execution and capital-return profile, while Chevron’s performance has been tempered by recent estimate revisions and a more measured production ramp. For momentum-focused investors, Suncor currently holds the edge.

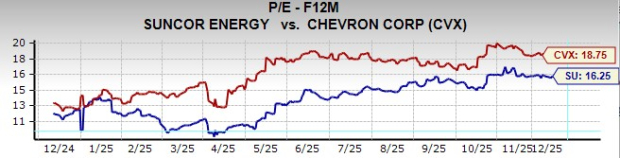

From a valuation standpoint, Suncor also screens more attractively. On a forward 12-month price-to-earnings basis, Chevron trades at roughly 19X, while Suncor trades just above 16X. For value-oriented investors, this multiple gap makes Suncor comparatively appealing.

Earnings estimate momentum provides another differentiator. On this front as well, Suncor currently holds a relative advantage.

Over the past week, the Zacks Consensus Estimates for Chevron’s 2025 and 2026 EPS have moved lower, reflecting near-term uncertainties around integration timing, capital spend and commodity sensitivities.

On the other hand, Suncor’s EPS estimates have remained unchanged, highlighting greater stability in expected results as the company enters 2026 with improving reliability and a low-decline production base.

While both Chevron and Suncor maintain a Zacks Rank #3 (Hold), the near-term setup tilts in Suncor’s favor. The company’s stronger YTD stock performance, more attractive valuation and steadier earnings estimates complement its structural advantages, namely low decline rates, record reliability and robust free-funds-flow durability heading into 2026.

Chevron still offers compelling long-term attributes, including global diversification, major project catalysts and consistent shareholder returns. However, recent estimate revisions and a premium valuation temper its relative appeal in the current environment.

Investors seeking value, operational stability and higher capital returns may find Suncor better positioned at this stage of the cycle, while Chevron remains a dependable choice for those prioritizing diversification and long-duration growth drivers.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-08 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite