|

|

|

|

|||||

|

|

|

Sterling Infrastructure, Inc. STRL is taking a meaningful step forward with the acquisition of CEC, expanding capabilities across mission-critical end markets and strengthening its position for higher-value opportunities in 2026. By combining site development expertise with a broader electrical services portfolio, the company is better aligned with customer demand for integrated solutions. Early feedback from customers has been notably positive, underscoring the strategic fit of the acquisition and its potential to support margin improvement in the year ahead.

In the third quarter of 2025, the company closed the CEC acquisition and recorded meaningful operational and financial contributions from the business. CEC contributed $41.4 million of revenues in September, with adjusted operating margins in line with expectations. The acquisition also strengthened visibility in the E-Infrastructure segment. The company reported a third-quarter backlog of $2.58 billion, to which CEC added $475 million. When combining signed backlog, unsigned electrical awards and future phase opportunities, the E-Infrastructure pipeline totals approximately $3 billion, demonstrating substantial multi-year demand.

CEC’s contribution extends beyond backlog. The company highlighted strong momentum heading into 2026, supported by robust customer demand, especially in the data center market, where several large projects have recently been booked. Sterling expects to leverage the combined platform to pursue higher-margin work, citing meaningful opportunities for margin expansion across the next couple of years.

For 2025, E-Infrastructure revenues are expected to grow 30% or higher on an organic basis and approach 50% including CEC. Adjusted operating margins for E-Infrastructure are projected at approximately 25% for 2025, up from 23.7% in 2024. Given this trajectory, the CEC acquisition is well-positioned to strengthen Sterling’s margin profile in 2026 as integration benefits compound and mix shifts toward higher-value mission-critical projects.

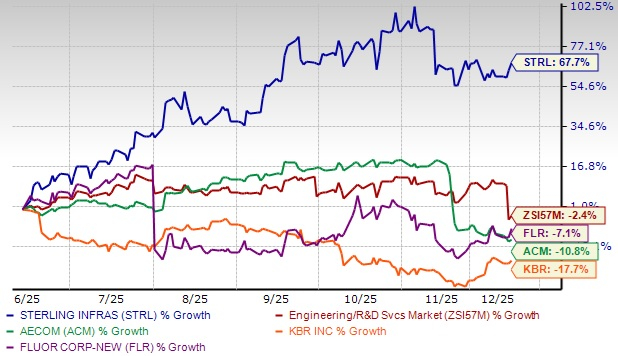

Shares of this Texas-based infrastructure services provider have surged 67.7% in the past six months, outperforming the Zacks Engineering - R and D Services industry’s 2.4% decline. In the same time frame, other industry players like AECOM ACM, Fluor Corporation FLR and KBR, Inc. KBR have declined 10.8%, 7.1% and 17.7%, respectively.

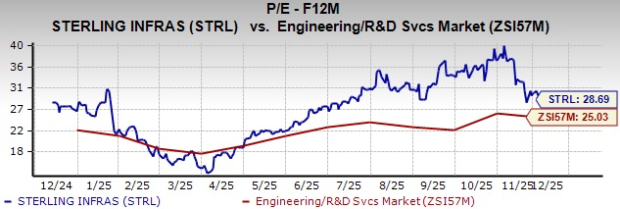

STRL stock is currently trading at a premium compared with its industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 28.69, as shown in the chart below.

Conversely, industry players, such as AECOM, Fluor and KBR, have P/E multiples of 17.42, 20.02 and 10.61, respectively.

For 2025 and 2026, STRL’s earnings estimates have increased in the past 60 days to $10.43 and $11.95 per share, respectively. The revised estimated figures indicate 71% and 14.6% year-over-year growth, respectively.

Conversely, AECOM and KBR’s earnings in the current year are likely to witness year-over-year increases of 8% and 13.8%, respectively, while Fluor’s earnings are expected to decline 7.3%.

The company currently carries a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite