|

|

|

|

|||||

|

|

|

Over the past six months, Waste Connections’s shares (currently trading at $171.55) have posted a disappointing 10.4% loss, well below the S&P 500’s 13.9% gain. This may have investors wondering how to approach the situation.

Following the pullback, is this a buying opportunity for WCN? Find out in our full research report, it’s free for active Edge members.

Operating a network of municipal solid waste landfills in the U.S. and Canada, Waste Connections (NYSE:WCN) is North America's third-largest waste management company providing collection, disposal, and recycling services.

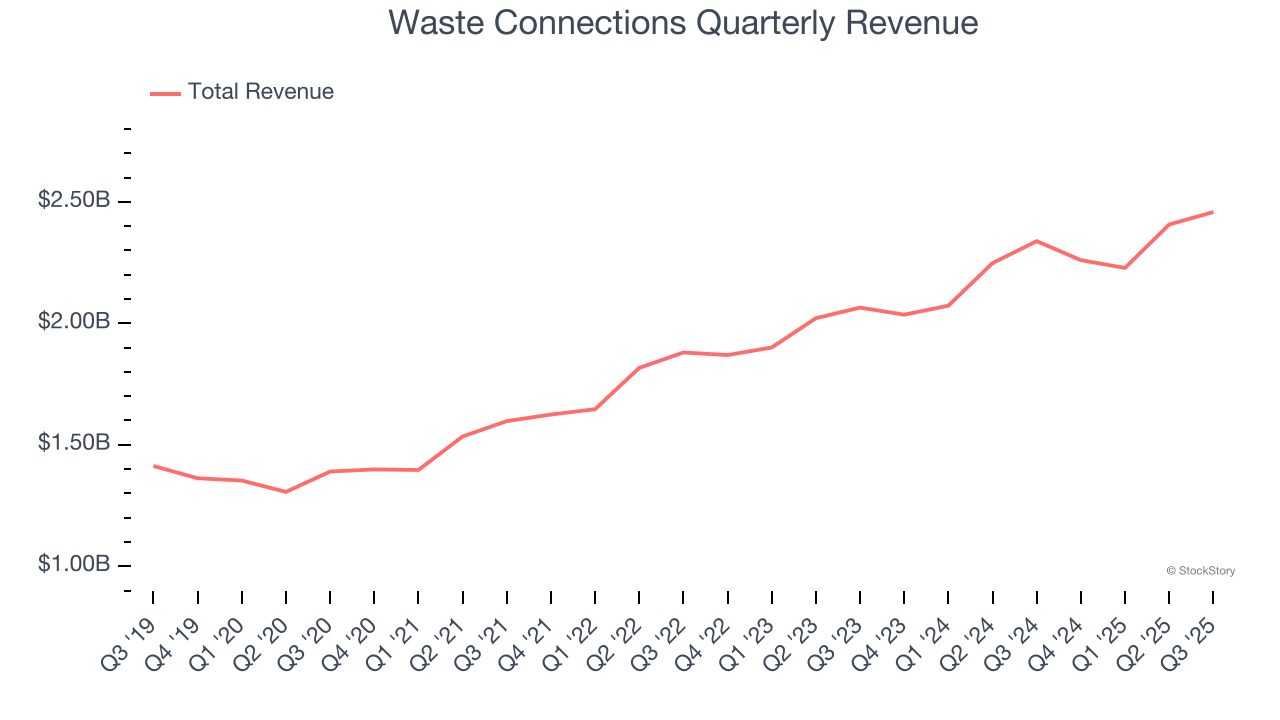

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Waste Connections’s 11.6% annualized revenue growth over the last five years was impressive. Its growth surpassed the average industrials company and shows its offerings resonate with customers.

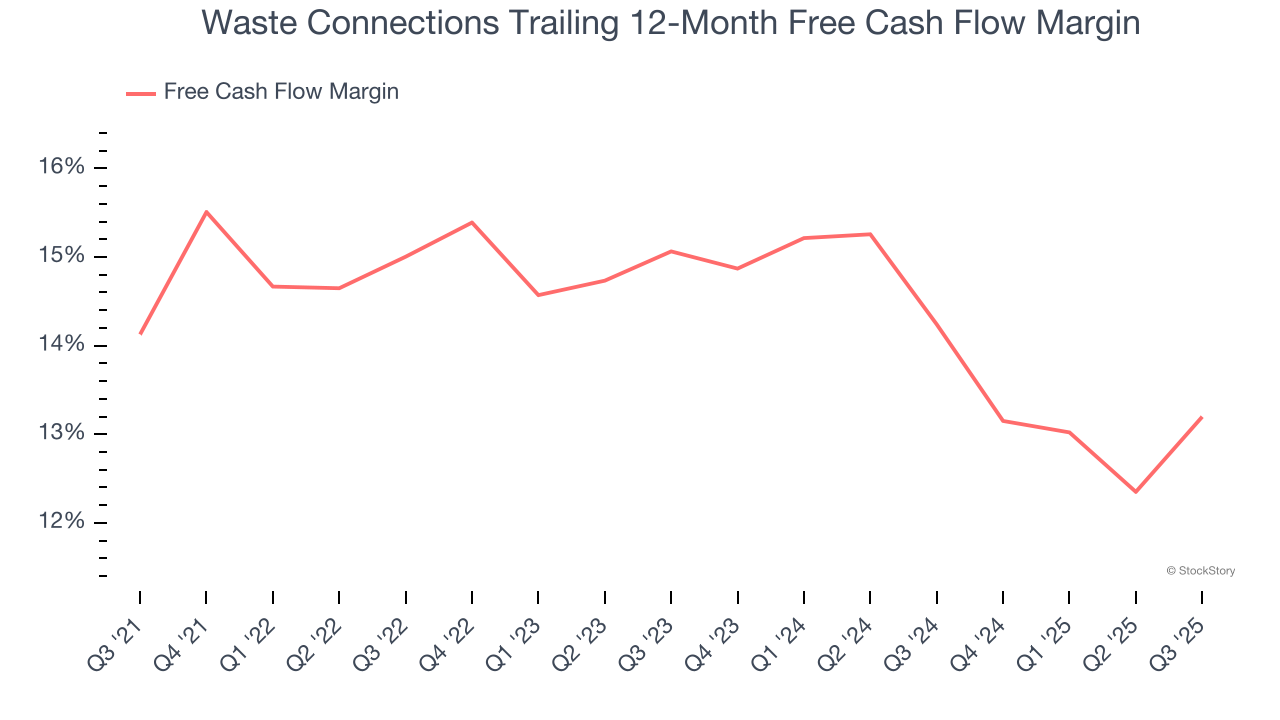

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Waste Connections has shown terrific cash profitability, putting it in an advantageous position to invest in new products, return capital to investors, and consolidate the market during industry downturns. The company’s free cash flow margin was among the best in the industrials sector, averaging 14.3% over the last five years.

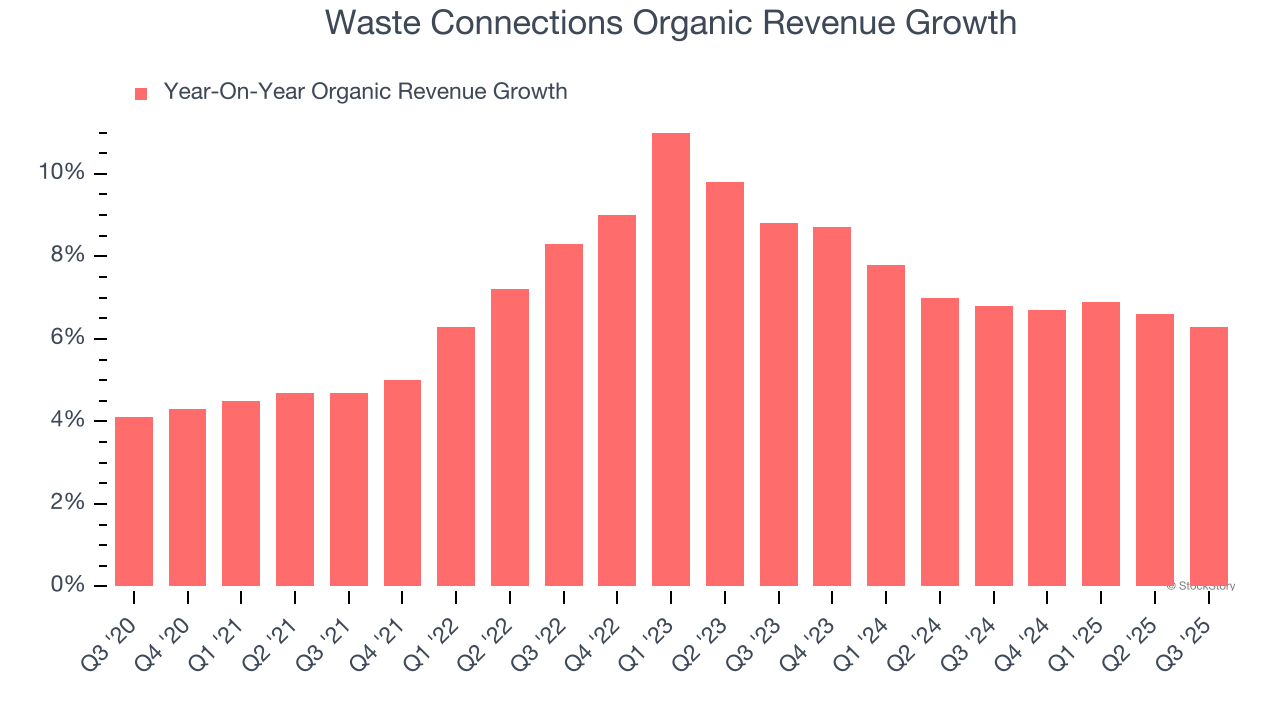

We can better understand Waste Management companies by analyzing their organic revenue. This metric gives visibility into Waste Connections’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Waste Connections’s organic revenue averaged 7.1% year-on-year growth. This performance slightly lagged the sector and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

Waste Connections’s merits more than compensate for its flaws. With the recent decline, the stock trades at 30.4× forward P/E (or $171.55 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free for active Edge members.

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Jul-27 | |

| Jul-27 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-07 | |

| Jun-23 | |

| Jun-16 | |

| May-15 | |

| May-12 | |

| Apr-23 | |

| Apr-23 | |

| Apr-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite