|

|

|

|

|||||

|

|

|

Applied Materials’ AMAT latest wafer fabrication equipment (WFE) is experiencing increased demand due to rising usage of semiconductors in artificial intelligence and high performance computing (HPC). AMAT reported that its leading-edge foundry/logic, DRAM and advanced packaging will be the fastest-growing areas of the WFE market.

AMAT specializes in Gate-All-Around (GAA) transistors at 2nm and below, Backside power delivery, Advanced wiring and interconnect, HBM stacking and hybrid bonding and 3D device metrology, which are indispensable for manufacturing next-generation semiconductor chips. Recent launches like Xtera epi, Kinex hybrid bonding, PROVision 10 eBeam will add to AMAT’s growth story.

AMAT expects next-generation technologies to be produced in large volume, which means that the company’s customers will be ramping up their foundries, naturally benefiting AMAT’s business. In 2025, AMAT strengthened its leadership in DRAM, growing revenues from leading-edge customers by more than 50%. This trend is likely to continue in the future.

However, in fiscal 2025, AMAT’s growth was constrained by increased trade restrictions and an unfavorable market mix. China’s share of total systems and services revenues declined to 28% for the year and 25% in the fourth quarter of fiscal 2025. AMAT expects that wafer fab equipment spending in China is expected to be lower in 2026, with no major easing in restrictions.

Companies like Lam Research LRCX and ASML Holdings ASML are leading WFE players in the DRAM, Logic and etching space. Lam Research’s Dynamic Random Access Memory and Non-Volatile Memory products are gaining traction on the back of AI. Lam Research is also winning multiple clients as DRAM manufacturers are using its latest conductor etch tool, Akara.

ASML Holdings’ top line is driven by its DRAM and logic customers, who are ramping leading-edge nodes using ASML’s NXE:3800E EUV systems. The company also delivers deposition and etching tools. However, ASML expects its gross margin to contract due to the revenue recognition from low-margin High Numerical Aperture EUV tools and lower upgrade revenues.

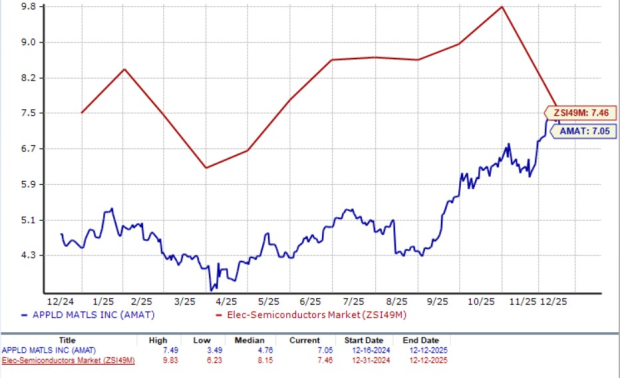

Shares of Applied Materials have gained 53% in the past year compared with the Electronics - Semiconductors industry’s growth of 32.3%.

From a valuation standpoint, Applied Materials trades at a forward price-to-sales ratio of 7.05X, lower than the industry’s average of 7.46X.

The Zacks Consensus Estimate for Applied Materials’ fiscal 2026 and 2027 earnings implies year-over-year growth of 1.27% and 17.20%, respectively. The estimates for fiscal 2026 and 2027 have been revised upward in the past 30 days.

Applied Materials currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| 3 hours | |

| 5 hours | |

| 10 hours | |

| 10 hours | |

| 12 hours | |

| 12 hours | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-08 | |

| Aug-08 | |

| Aug-08 | |

| Aug-07 | |

| Aug-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite