|

|

|

|

|||||

|

|

|

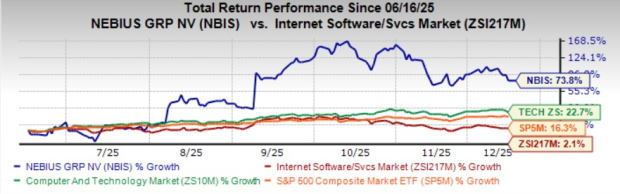

Nebius Group N.V. NBIS stock has gained 73.8% in the past six months, outperforming the Zacks Computer & Technology sector and the Zacks Internet Software Services industry’s growth of 22.7% and 2.1%, respectively. The S&P 500 composite is up 16.3% over the same time frame. The company’s shares have gained just 2% in the past month.

Let’s unpack the company’s fundamentals and challenges to ascertain the best course of action.

NBIS is navigating through challenges such as macroeconomic uncertainty, rising operating costs and substantial capital outlays. In the third quarter of 2025, sales, general and administrative expenses surged 87% year over year, reflecting the cost burden of rapid expansion. For full-year 2025, Nebius has also increased its capital expenditure guidance sharply, from around $2 billion to approximately $5 billion.

Elevated capital expenditure levels pose a risk if revenue growth fails to keep pace with the company’s capital intensity, particularly in an environment where AI demand may fluctuate amid competitive pricing pressures and evolving regulatory frameworks.

Also, the company has tightened full-year revenue guidance to $500–$550 million, expecting results to land near the midpoint due to timing delays in bringing capacity online. While adjusted EBITDA is expected to turn slightly positive at the group level by year-end 2025, it will remain negative for the full year. Moreover, scaling aggressively (multiple data centers in various regions) involves execution risk.

Apart from this, the company faces stiff competition from other leading players, such as Microsoft Corporation MSFT, Amazon AMZN and CoreWeave, Inc. CRWV. Also, Microsoft's capital spending has reached alarming levels, raising serious concerns about return on investment and financial sustainability. Microsoft expects the fiscal 2026 capital expenditure growth rate to be higher than fiscal 2025.

CRWV is facing increasing supply-chain pressures, where demand for its AI cloud platform greatly exceeds available capacity, limiting its ability to serve customers fully. CoreWeave now expects revenues of $5.05–$5.15 billion, down from $5.15–$5.35 billion. On the other hand, Amazon’s heavy spending on AI and data center expansion is pressuring its finances. AMZN expects its capital expenditure to reach around $125 billion in 2025, with further increases planned for 2026.

Valuation-wise, Nebius seems overvalued, as suggested by the Value Score of F.

In terms of Price/Book, NBIS shares are trading at 4.59X, higher than the Internet Software Services industry’s 3.84X.

Nebius operates in a supply-constrained AI infrastructure market, where demand for GPU capacity significantly outstrips available power and data-center readiness. To capitalize on this imbalance, the company is rapidly scaling its infrastructure, now targeting 2.5 gigawatts of contracted power by 2026, up from its earlier projection of 1 gigawatt. By the end of next year, Nebius expects 800 megawatts-1 gigawatt of fully connected capacity to be operational.

In the last earnings call, management highlighted the securing of two major hyperscale agreements: a $3 billion, five-year contract with Meta and a $17.4–$19.4 billion deal with Microsoft, underscoring strong demand visibility. Alongside capacity expansion, Nebius is strengthening its enterprise offering with the launch of the Aether 3.0 cloud platform and Nebius Token Factory, an inference solution designed to run open-source models at scale.

In 2026, Nebius plans to further expand its existing data centers in the UK, Israel and New Jersey, while bringing new facilities online across the US and Europe in the first half of the year. Nebius is also securing multiple large-scale sites, each capable of delivering hundreds of megawatts, with several expected to become operational before the end of 2026. The company is targeting $7–$9 billion in ARR by 2026 and remains on track to generate $900 million-$1.1 billion in ARR by the end of 2025.

Nebius Group N.V. price-consensus-chart | Nebius Group N.V. Quote

Despite strong long-term tailwinds, such as multi-billion-dollar contracts and rapid data-center expansion, near-term risks remain a concern. These include a stretched valuation, execution and scaling challenges, rising cost pressures and intensifying competition, all of which could weigh on performance in the shorter term.

Given this risk–reward imbalance, existing investors may consider exiting their positions to limit potential downside, while prospective investors may remain on the sidelines.

At present, NBIS carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 25 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite