|

|

|

|

|||||

|

|

|

Taylor Morrison Home Corporation TMHC is a national land developer and homebuilder giant that’s seen its earnings revisions tumble over the last year based on a multitude of headwinds.

TMHC’s recent negative earnings per share (EPS) revisions earn the homebuilder a Zacks Rank #5 (Strong Sell). The company’s near-term outlook remains strained, given the industry and economy-wide setbacks it is facing.

Taylor Morrison is one of the largest U.S. homebuilders. The Scottsdale, Arizona-headquartered firm designs, builds, and sells single-family homes, ranging from first-time/entry-level to move-up and luxury/resort-style. TMHC posted booming revenue growth between 2013 and 2022, highlighted by 29% expansion in 2020 and 22% growth in 2021.

The wild Covid-driven housing boom created a massive pull forward across the home-buying market. The market also benefited from a buyer-friendly low mortgage rate environment.

The housing market has cooled significantly since then as home prices and mortgage rates soared.

Taylor Morrison is projected to see its revenue fall 2.4% in 2025 and then fade 6.5% next year. Its adjusted earnings are expected to drop 5.5% and 12.5%, respectively.

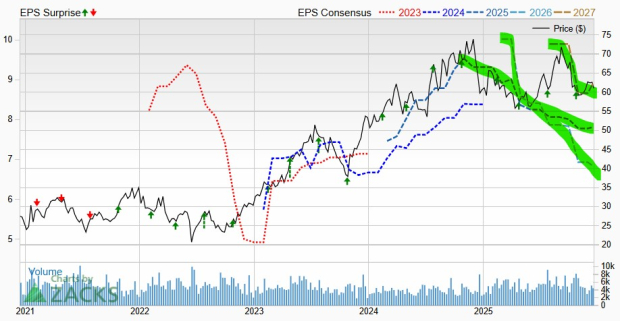

Image Source: Zacks Investment Research

The company’s earnings estimate has dropped 21% for Q4 since its last report and 13% for 2026. TMHC’s downbeat earnings revisions earn it a Zacks Rank #5 (Strong Sell) and extend its downward run that began in late 2024.

That said, the homebuilder’s long-term outlook likely remains firmly intact given the dire need for more housing inventory in the U.S. “Encouragingly, net absorption paces improved each month during the quarter, in contrast to typical seasonal slowing into the end of summer as the improvement in mortgage interest rates helped spur activity,” CEO Sheryl Palmer said in prepared Q3 remarks in October.

“Going forward, we believe strengthened consumer confidence is critical to further stabilizing demand, especially for discretionary home purchase decisions in our move-up and resort lifestyle communities.”

In the near term, persistently high mortgage rates could continue to suppress demand, leading to slower home sales, increased cancellations, and pressure on margins if TMHC is forced to rely more on incentives to move inventory.

Taylor Morrison doesn’t pay a dividend, and its Building Products - Home Builders industry is in the bottom 10% of 240 Zacks industries. This is worth stressing since studies have shown that roughly half of a stock's price movement can be attributed to a stock's industry group.

Investors might want to stay away from Taylor Morrison for now since the housing market remains under stress.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-16 | |

| Jul-14 | |

| Jul-13 | |

| Jul-06 | |

| Jun-25 | |

| Jun-12 | |

| Jun-10 | |

| Jun-09 | |

| Jun-06 | |

| Jun-04 | |

| Jun-03 | |

| Jun-02 | |

| Jun-02 | |

| Jun-02 |

Berkshire Is Convinced the American Dream of Homeownership Will Stay Alive

TMHC

The Wall Street Journal

|

| Jun-01 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite