|

|

|

|

|||||

|

|

|

Pfizer has at least two key candidates in the pipeline that look like future winners.

Merck has launched several products in preparation for a massive upcoming patent cliff.

One of these drugmakers has made more headway towards addressing its challenges.

Pfizer (NYSE: PFE) and Merck (NYSE: MRK) are two pharmaceutical giants that have lagged broader equities this year. Both have delivered unimpressive financial results recently, and are facing a somewhat uncertain medium-term outlook as they seek ways to navigate upcoming patent cliffs.

Both could make significant progress toward that goal in 2026, but which one is the better option for investors heading into the new year? Let's find out.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Image source: Getty Images.

Pfizer's Eliquis, a blood thinner and one of its best-selling therapies, will lose patent exclusivity within the next few years. In the meantime, the company's performance leaves a lot to be desired. Revenue and earnings growth have been slow (at best) in recent years -- so the patent cliff will only worsen things.

Thankfully, the drugmaker has taken steps to address its issues. Pfizer has significantly expanded its pipeline thanks to internal efforts, acquisitions, and licensing deals. These initiatives helped it launch brand-new products. Most of these aren't yet making a significant impact on its financial results, but more are on the way. Two in particular are worth mentioning.

The first is MET-097i, an investigational GLP-1 weight loss asset. This medicine performed well in phase 2 studies. Not only did MET-097i induce substantial weight loss, but it also did so with fewer side effects than many other GLP-1 candidates -- all with a long-acting dosing schedule that could prove a significant advantage in the fast-growing anti-obesity market. There is still work to be done before Pfizer can launch MET-097i, but the medicine appears promising.

Then there's PF-4404, an investigational cancer therapy. Management believes PF-4404 has the profile of a pipeline drug, meaning it could earn many indications and become a standard of care for certain cancers, potentially generating blockbuster sales in the process. Pfizer has already initiated phase 3 studies for PF-4404, with additional studies to follow.

Besides Pfizer's efforts to boost sales and circumvent patent cliffs, the company has also worked to improve its margins and bottom line. Its cost-cutting initiatives are helping in that regard. And thanks to a deal with the White House, it will be exempt from tariffs for three years in exchange for selling some medicines at reduced prices to U.S. patients. Pfizer is slowly building for the future, and its efforts could pay off for patient investors in the long run.

Merck's sales from Gardasil and Gardasil 9, its HPV vaccines that are among its biggest growth drivers, have dropped this year due to lower sales in China. And in even worse news, its Keytruda, the best-selling cancer medicine in the world, will experience a patent cliff by 2028. But the company has shown signs that it can overcome these challenges.

Merck has already earned approval for a new, subcutaneous version of Keytruda. The SC formulation can be administered in a couple of minutes, whereas the old version takes at least half an hour. In other words, it's a much shorter trip for patients, physicians can see more patients, and it's far more convenient for everyone involved. This is especially true since SC Keytruda demonstrated similar safety and efficacy in clinical trials. It will inherit many of the old version's indications, and help smooth out sales losses once biosimilars enter the market.

Meanwhile, the pipeline has produced gems in recent years and should continue doing so. Last year Merck earned approval for Winrevair, a medicine for pulmonary arterial hypertension with a new mechanism of action. And based on recent clinical trial data, Winrevair -- whose revenue run rate already exceeds $1 billion -- could earn important label expansions. The company also launched Capvaxive, a pneumonia vaccine, last year; it has generated strong sales so far.

Lastly, the drugmaker could make waves in the influenza market thanks to an acquisition that will add a product called CD388 to its pipeline. CD388 could address the shortcomings of current flu vaccines and revolutionize that market. In short, Merck has excellent approved products, and pipeline candidates ready to take over once the Keytruda patent cliff arrives.

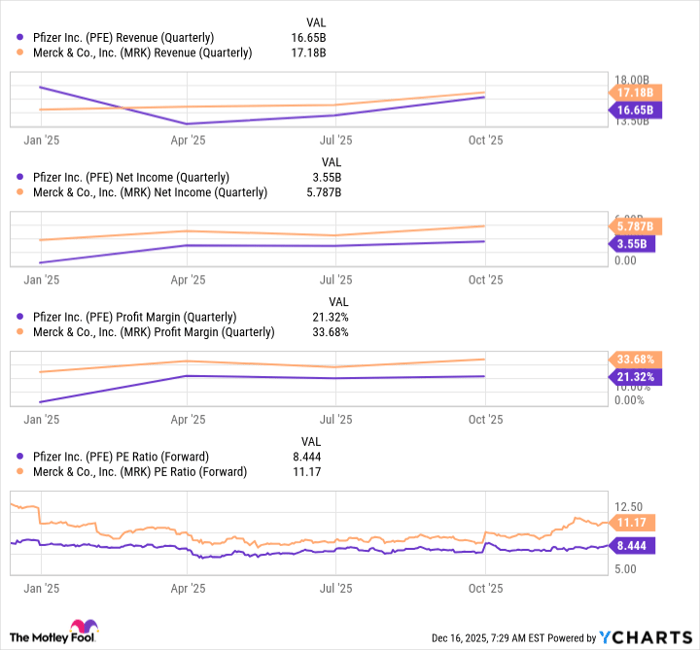

While both companies are good options for long-term investors, Merck appears to be the better choice right now. Its financial results, including profit margins, look stronger overall:

PFE Revenue (Quarterly) data by YCharts.

Furthermore, Merck's plan to address its challenges already appears well-formed, or at least much more so than Pfizer's. True, the latter stock seems somewhat cheaper, but both are pretty attractive at current levels, given the healthcare sector's average forward price-to-earnings (P/E) ratio of 17.8. And Merck's higher forward P/E is fully justified given its stronger fundamentals and better medium-term prospects.

Despite Pfizer's higher forward dividend yield of 6.5% (Merck's is 3.4%), Merck has grown its dividends much faster over the past decade and currently has a much higher dividend per share than its peer. That means it may also be the better option for dividend seekers.

Before you buy stock in Pfizer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Pfizer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $506,935!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,067,514!*

Now, it’s worth noting Stock Advisor’s total average return is 958% — a market-crushing outperformance compared to 192% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of December 19, 2025.

Prosper Junior Bakiny has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Merck and Pfizer. The Motley Fool has a disclosure policy.

| Apr-03 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Mar-31 | |

| Mar-31 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite