|

|

|

|

|||||

|

|

|

CF Industries Holdings, Inc. CF gains on healthy nitrogen fertilizer demand in major markets and higher nitrogen prices amid headwinds from higher natural gas costs.

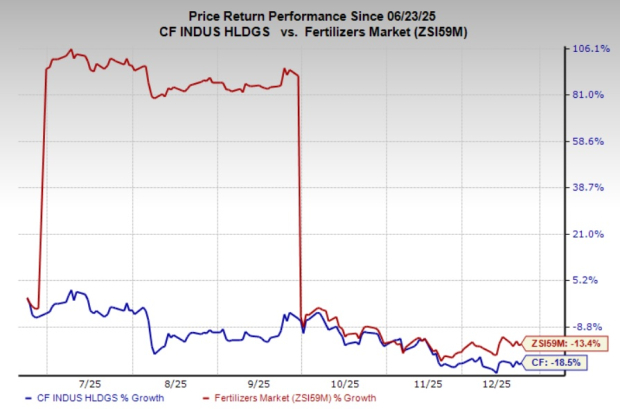

The CF stock has lost 18.5% in the past six months compared with the Zacks Fertilizers industry’s 13.4% decline.

Let’s find out why CF stock is worth retaining at the moment.

CF Industries is capitalizing on the growing global demand for nitrogen fertilizers, fueled by strong agricultural activity. After pandemic-related challenges, industrial demand for nitrogen has recovered.

Global nitrogen requirement is expected to remain strong in the near future due to recovering industrial demand and farmer economics. High levels of corn-planted acres in the United States should drive the demand for nitrogen this year. Demand in North America is expected to be fueled by favorable farm economics. CF Industries also sees strong demand for urea from Brazil and India. Demand for urea is likely to remain strong in Brazil on higher corn plantings and in India, driven by low inventory levels.

The global nitrogen outlook remains positive through 2025 and beyond, supported by strong demand and tight supply, per CF Industries. India, Brazil, and North America are driving robust fertilizer consumption, while inventories remain below average despite resumed Chinese exports. Supply constraints from high energy costs and limited gas availability continue to pressure producers in Europe and Asia. Growing demand for low-carbon ammonia further strengthens the market. With energy cost advantages favoring North American producers and limited new capacity additions, the global nitrogen balance is expected to tighten, supporting firm pricing and margins in the years ahead.

Higher nitrogen prices have also contributed to a boost in CF Industries’ revenues. In the third quarter, net sales rose roughly 21% year over year to roughly $1.66 billion. Average selling prices increased year over year, driven by strong global nitrogen demand, supply disruptions due to geopolitical issues, and higher global energy costs. Looking ahead, CF should continue to benefit from favorable pricing trends.

CF Industries continues to focus on enhancing shareholder value by utilizing its strong cash flow. Net cash provided by operating activities was $1.06 billion in the third quarter, up around 14% year over year. CF returned $445 million to shareholders in the third quarter and around $1.3 billion in the first nine months of 2025. The company completed the $3 billion share repurchase program in October 2025. It started a new $2 billion share repurchase program effective through 2029.

The company faces headwinds from higher natural gas prices, a key feedstock for nitrogen fertilizer. It has seen a notable rise in natural gas costs during the first nine months of 2025. The average cost of natural gas increased to $2.96 per MMBtu (million metric British thermal unit) in the third quarter from $2.10 per MMBtu a year ago. The same for the first nine months increased to $3.34 per MMBtu from $2.38 per MMBtu in the year-ago period. Natural gas prices have shot up in Europe and Asia due to constrained supply availability. Higher gas costs are expected to weigh on CF’s margins in 2025.

CF currently carries a Zacks Rank #3 (Hold).

Some better-ranked stocks in the Basic Materials space are Kinross Gold Corporation KGC, Fortuna Mining Corp. FSM and Equinox Gold Corp. EQX.

At present, KGC sports a Zacks Rank #1 (Strong Buy), while FSM and EQX carry a Zacks Rank #2 (Buy) each. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for KGC’s current-year earnings is pegged at $1.68 per share, indicating a year-over-year rise of 147%. Its earnings beat the Zacks Consensus Estimate in three of the trailing four quarters while missing once, with an average surprise of 17.4%. KGC shares have gained 82.1% over the past six months.

The Zacks Consensus Estimate for FSM’s current fiscal-year earnings is pinned at 76 cents per share, indicating a 65.2% year-over-year increase. Its shares have surged 49% over the past six months.

The Zacks Consensus Estimate for EQX’s current-year earnings stands at 54 cents per share, reflecting a 170% year-over-year increase. Its earnings beat the Zacks Consensus Estimates in two of the trailing four quarters and missed twice, with the average earnings surprise of 87%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-01 | |

| Jul-31 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-27 | |

| Jul-23 | |

| Jul-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite