|

|

|

|

|||||

|

|

|

Dry powder is money that is ready when an opportunity shows up, so stability and liquidity matter more than chasing yield.

Ultra-short Treasury bill exposure is designed to behave much closer to cash while still paying serious interest in the current economy.

I love the idea of "dry powder." I love it a little less when I notice my IRA "cash" is earning approximately a shrug.

So I went looking for a smarter parking spot -- something that doesn't swing around in value like your average index fund, is easy to sell when opportunity shows up, and pays more than a sleepy sweep account. I'll admit that I didn't necessarily arrive at these three characteristics in that order, and the results weren't exactly what I expected.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Here's what I considered, what I rejected along the way, and what finally clicked.

Image source: Getty Images.

Step 1: Decide what "dry powder" is supposed to do. This definition isn't as easy or clear-cut as it sounds.

Dry powder has one job: be there when you need it.

When one of my favorite tickers goes on fire sale, I want to have some investable funds ready to take advantage of that opportunity.

And I don't like market timing, but you never know. The stock market is known to take occasional dips, even when the economy looks solid. So it could make sense to hold back some of my S&P 500 (SNPINDEX: ^GSPC) investments in vehicles like the Vanguard S&P 500 ETF (NYSEMKT: VOO) and State Street SPDR Portfolio S&P 500 ETF (NYSEMKT: SPYM) funds. I might be able to buy them at a better price in 2026. I'm never going all-in on that idea, but a modest portfolio adjustment makes sense.

That means the best "cash stand-ins" are the ones least likely to be down on the exact day you want to redeploy. VOO and SPYM don't do this job, since they're directly tied to the broader stock market's real-time price moves.

A dividend stock can still get crushed on bad news, recessions, or sector trouble. That's fine for long-term investing but terrible for "money I might need next week." Solid dividend payers can be helpful in a diversified portfolio, but they don't do the job I'm trying to fill here.

Verdict: Dividend investments add too much single-stock risk for a portfolio component I'm calling a "cash equivalent."

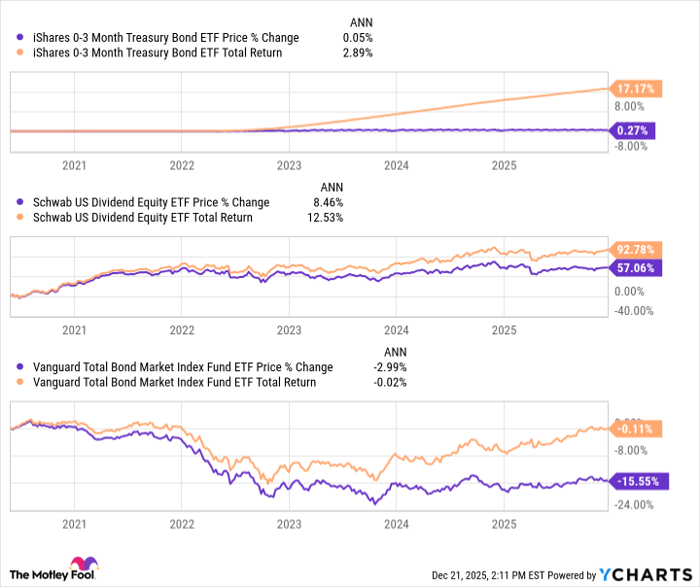

I seriously considered the popular dividend-oriented fund Schwab US Dividend Equity (NYSEMKT: SCHD) for a minute. It's a diversified, shareholder-friendly fund with more than 100 individual holdings, and it pays a real distribution. Current 30-day yield: 3.83%. The expense ratio is a Vanguard-level 0.06%. If you want a long-term equity holding with an income tilt, it can be a solid choice.

But here's the catch: SCHD is still 100% stocks. If the market drops, SCHD can drop too -- sometimes a lot. It posted sharp price cuts in the early COVID-19 shutdown phase, another deep drop in the inflation crisis of 2022, and a third S&P 500-level retreat around the "liberation day" tariff announcements in April 2025. That makes it a shaky "parking spot" for opportunistic buys. Might as well just stick with VOO, honestly.

Verdict: Just like single stocks, dividend funds can be useful as an equity allocation, but not as dry powder.

Next I looked at the classic "safer than stocks" middle ground: Vanguard Total Bond Market Index Fund (NASDAQ: BND) or iShares Core US Aggregate Bond ETF (NYSEMKT: AGG). If nothing else, their bond structure should make them effective hedges against unexpected stock market moves.

They're legitimate long-term bond-core holdings. But they're intermediate-duration funds, which means they can fall when rates rise. I'm not talking about "tiny chart wiggle" falls, but real drawdowns. For example, they saw roughly half the price drops of the S&P 500 in 2022, but then they never followed the stock market up in 2023 and 2024. All told, BND and AGG investors haven't even kept up with inflation in the last 3 or 6 years.

Verdict: Like the dividend investments, bonds can play a functional strategic role. They're just not reliably cash-like.

Once I stopped trying to make "income" do the job of "cash," the answer got simpler: very short-term U.S. Treasuries -- the kind of stuff that behaves like cash but yields more when short rates are elevated.

A common way to do that inside an IRA is a T-bill ETF like the iShares 0-3 Month Treasury Bond ETF (NYSEMKT: SGOV). This fund invests in short-term government debt, and is a simpler equivalent to purchasing those Treasuries directly.

In an era of high Fed rates, you can usually count on these payouts to beat the best interest rates in your brokerage's cash sweep accounts. And you've seen how slowly these rates move down, even under extreme political pressure to cut them quicker.

So the short-term Treasury Bond ETF fits dry powder better than the rejected SCHD, BND, or AGG ideas:

And the fund price is rock solid, even in a deep financial crisis. The iShares fund, for instance, really didn't move much in 2019 or 2022, but its payouts have made a helpful difference in recent years:

If you want long-term equity income, a fund like SCHD can be great (it's just not "cash").

Do you prefer a long-term bond allocation? Bond funds like BND/AGG can make sense.

But if you want true dry powder in your investment account that doesn't pay peanuts? Look to T-bills/ultra-short Treasuries. SGOV is not the only name in the game, but it's popular for good reason.

Dry powder shouldn't be exciting. It should be dependable. SGOV fits the bill for me.

Before you buy stock in iShares Trust - iShares 0-3 Month Treasury Bond ETF, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and iShares Trust - iShares 0-3 Month Treasury Bond ETF wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $509,039!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,109,506!*

Now, it’s worth noting Stock Advisor’s total average return is 972% — a market-crushing outperformance compared to 193% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of December 23, 2025.

Anders Bylund has positions in State Street SPDR Portfolio S&P 500 ETF and Vanguard S&P 500 ETF. SGOV is on his shopping list right now. The Motley Fool has positions in and recommends Vanguard S&P 500 ETF, Vanguard Total Bond Market ETF, and iShares Trust-iShares 0-3 Month Treasury Bond ETF. The Motley Fool has a disclosure policy.

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-01 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite