|

|

|

|

|||||

|

|

|

Datadog has followed the market’s trajectory closely, rising in tandem with the S&P 500 over the past six months. The stock has climbed by 9.5% to $141.85 per share while the index has gained 13.4%.

Is DDOG a buy right now? Find out in our full research report, it’s free for active Edge members.

Named after a database the founders had to painstakingly look after at their previous company, Datadog (NASDAQ:DDOG) provides a software platform that helps organizations monitor and secure their cloud applications, infrastructure, and services.

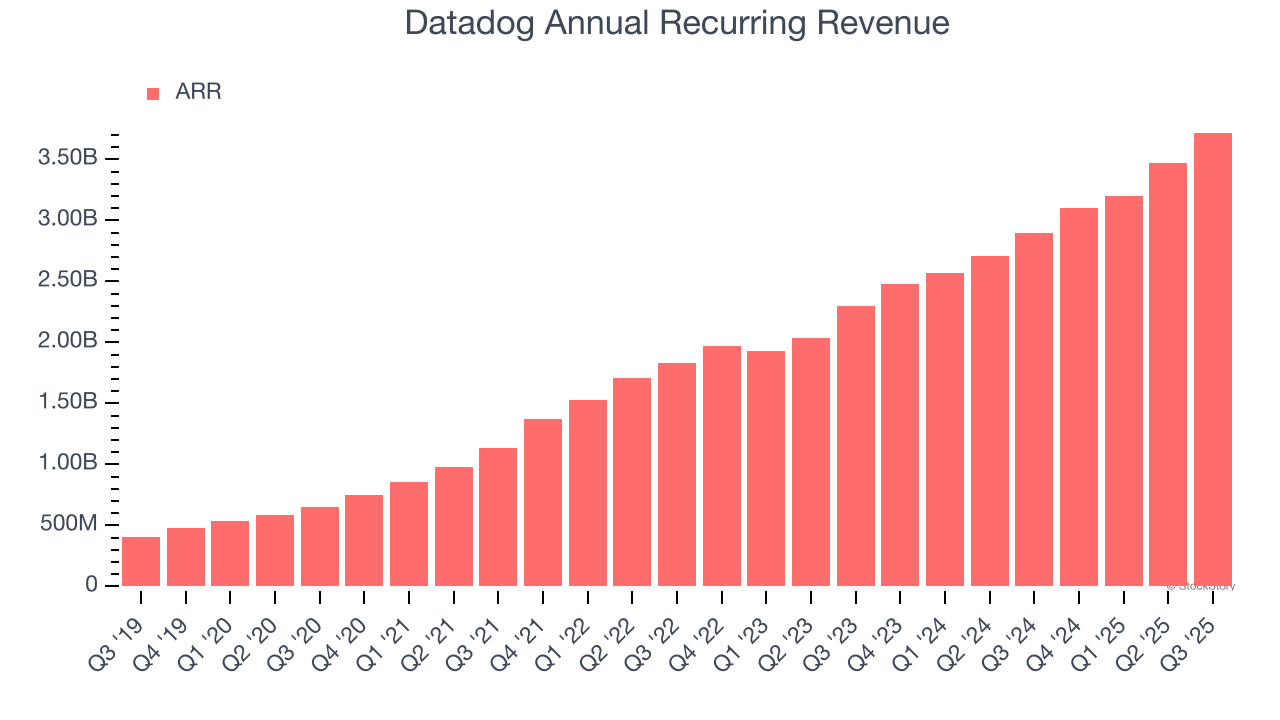

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Datadog’s ARR punched in at $3.72 billion in Q3, and over the last four quarters, its year-on-year growth averaged 26.5%. This performance was fantastic and shows that customers are willing to take multi-year bets on the company’s technology. Its growth also makes Datadog a more predictable business, a tailwind for its valuation as investors typically prefer businesses with recurring revenue.

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite, though some deceleration is natural as businesses become larger.

Over the next 12 months, sell-side analysts expect Datadog’s revenue to rise by 21.7%. While this projection is below its 26.5% annualized growth rate for the past two years, it is admirable and indicates the market is baking in success for its products and services.

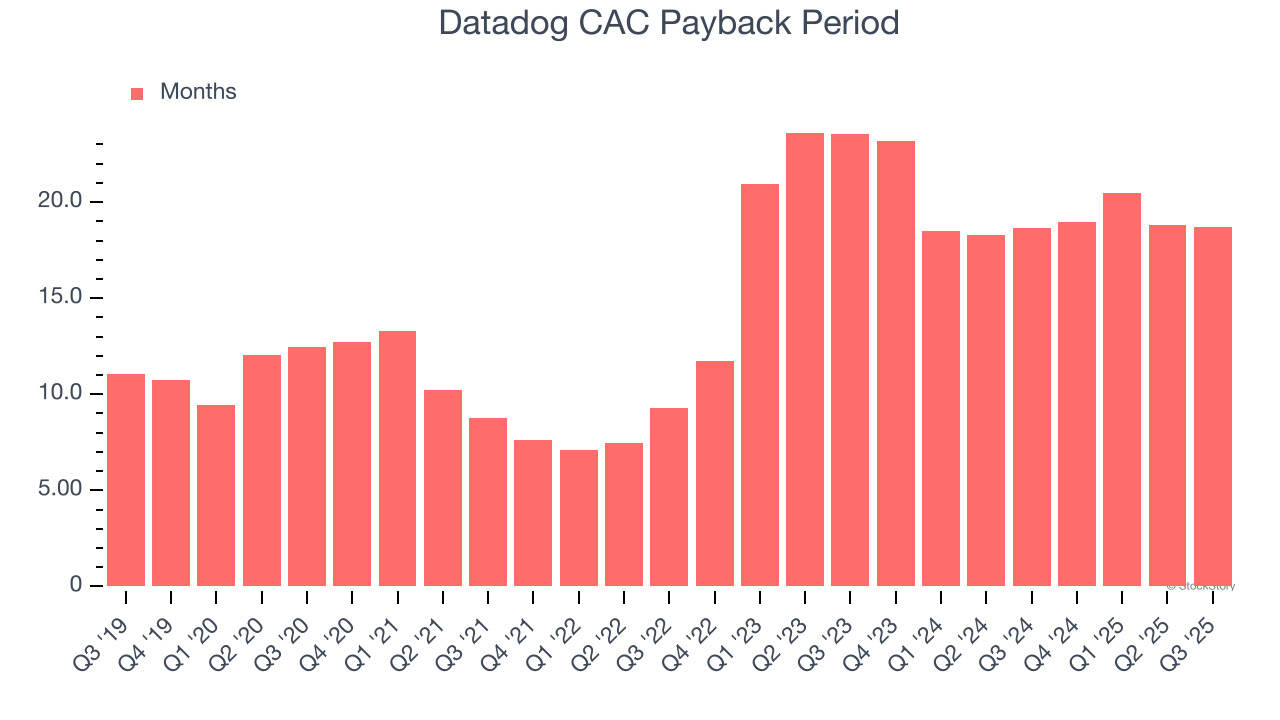

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Datadog is extremely efficient at acquiring new customers, and its CAC payback period checked in at 18.7 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation. These dynamics give Datadog more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

These are just a few reasons why we think Datadog is an elite software company, but at $141.85 per share (or 13× forward price-to-sales), is now the time to initiate a position? See for yourself in our comprehensive research report, it’s free for active Edge members .

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

| Apr-02 | |

| Apr-02 | |

| Apr-01 | |

| Mar-25 | |

| Mar-24 | |

| Mar-24 | |

| Mar-24 | |

| Mar-23 | |

| Mar-17 | |

| Mar-17 | |

| Mar-17 | |

| Mar-17 | |

| Mar-16 | |

| Mar-15 | |

| Mar-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite