|

|

|

|

|||||

|

|

|

Bath & Body Works, Inc. (BBWI) appears to be facing a structural decline as sales, earnings power, brand relevance, and analyst expectations continue to trend lower. What was once a productive specialty retail model is increasingly under pressure in a more competitive, digitally driven landscape.

Store traffic remains muted, and the company has struggled to resonate with younger consumers, leading to ongoing market share losses to competitors with stronger product innovation and more effective digital engagement. At the same time, margin visibility is deteriorating. Elevated promotional activity, persistent tariff exposure, and rising operating costs are compressing profitability, with few clear offsets in sight.

Management’s revised outlook points to a longer and more challenging recovery. Softer top-line expectations, combined with continued SG&A deleverage, suggest earnings will remain constrained even if demand stabilizes. With promotional intensity likely to remain elevated, execution risk appears skewed to the downside over the next several quarters.

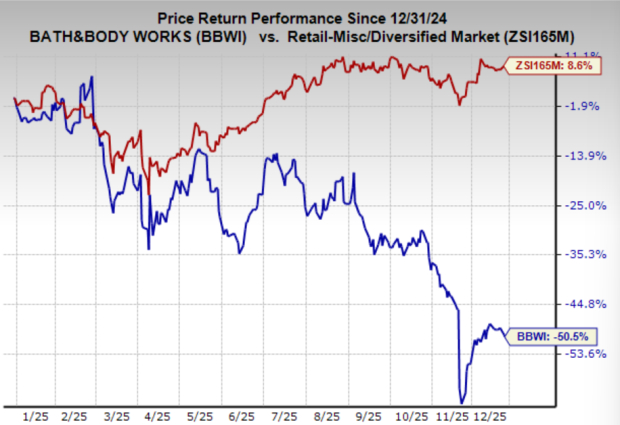

Reflecting these challenges, analysts have continued to downgrade the stock. Shares have been in a persistent downtrend for roughly four years, underscoring the market’s lack of confidence in a near-term turnaround.

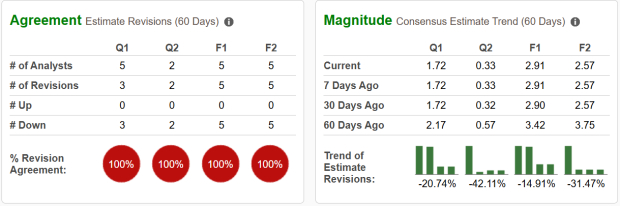

The earnings revision trend for Bath & Body Works has deteriorated meaningfully again over the past 60 days, pushing the stock to a Zacks Rank #5 (Strong Sell). Analyst confidence has weakened sharply, with next quarter earnings estimates cut by 42% and next year estimates reduced by 31.5%, reflecting rising concerns around demand, margins, and execution.

The top line outlook offers little support. Sales are expected to decline 2.3% next year and a further 3% in 2027, signaling ongoing pressure on traffic. On the bottom line, earnings are forecast to fall 11.6% this year and 11.5% next year, suggesting that cost pressures and promotional intensity are overwhelming management’s ability to protect profitability.

This combination, falling revenue, shrinking margins, and accelerating estimate cuts is particularly concerning. Sustained negative revisions tend to weigh heavily on stock performance, and without a clear catalyst to stabilize earnings expectations, BBWI remains fundamentally challenged in the near to intermediate term.

Given the ongoing deterioration in fundamentals, BBWI remains a stock to avoid. Earnings estimates continue to move sharply lower, revenue trends are negative, and margin pressure shows little sign of abating. In retail, sustained negative revisions are rarely a short-term issue, and BBWI’s estimate trajectory suggests deeper structural challenges rather than a temporary slowdown.

Until the company can demonstrate a clear inflection in traffic, brand relevance, and profitability, and until earnings revisions stabilize, the risk-reward profile remains unattractive. With shares entrenched in a multi-year downtrend and analyst sentiment firmly negative, BBWI lacks the catalysts needed to justify new capital at this stage.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-20 | |

| Jul-16 | |

| Jul-15 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-06 | |

| Jul-06 | |

| Jun-26 | |

| Jun-24 | |

| Jun-23 | |

| Jun-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite